Biotech, Panic is in the Air!

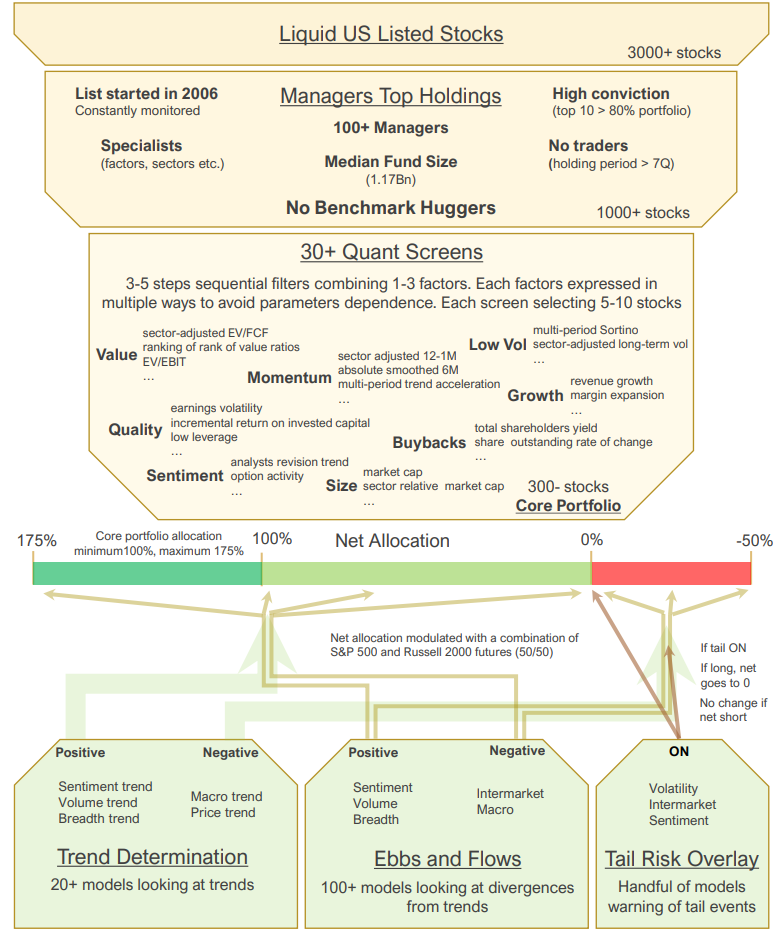

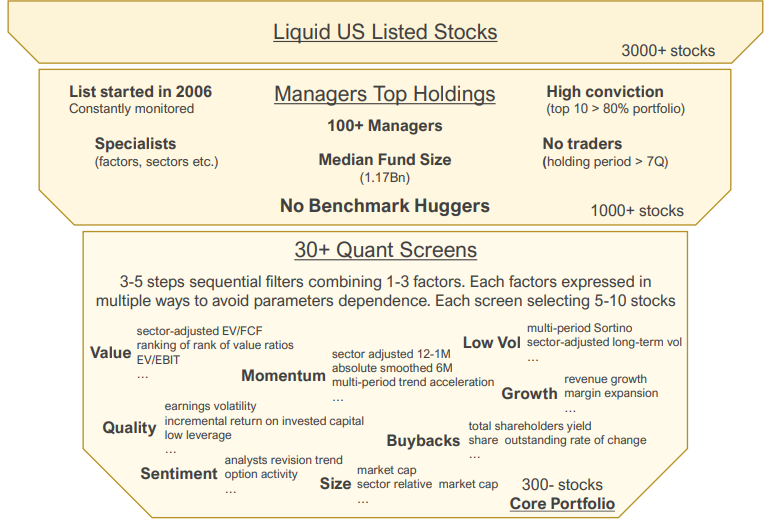

As you probably know by now, one of our strategy, the Sentinel Gurus US, uses the holdings of more than 100 managers to create the universe on which we run our quantitative screens.

The methodology looks like this:

For most of the rest of this article, we will concentrate on the universe of stocks generated at the following step:

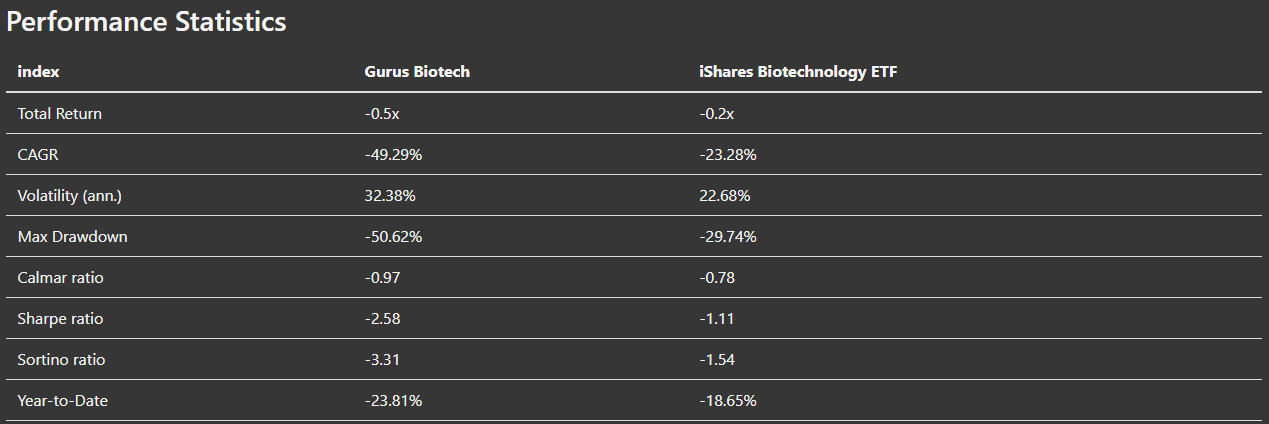

While the biotech sector has been underperforming recently, the biotech holdings of our managers (some of whom are biotech specialists) have experienced their worst return ever.

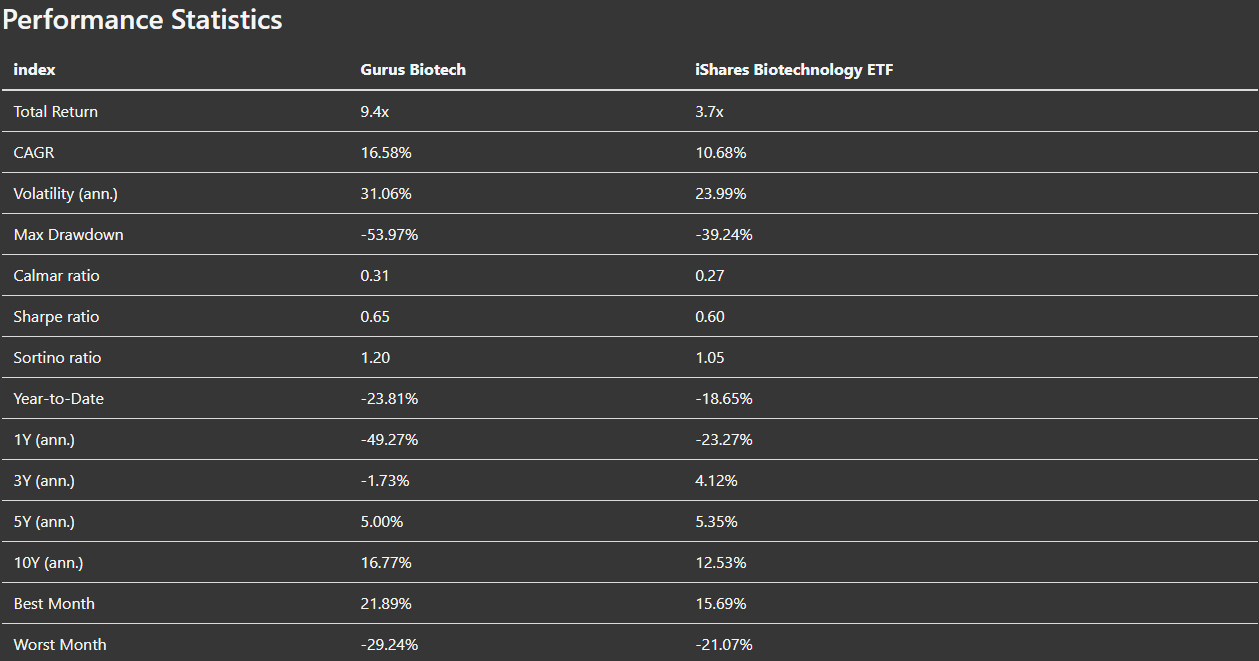

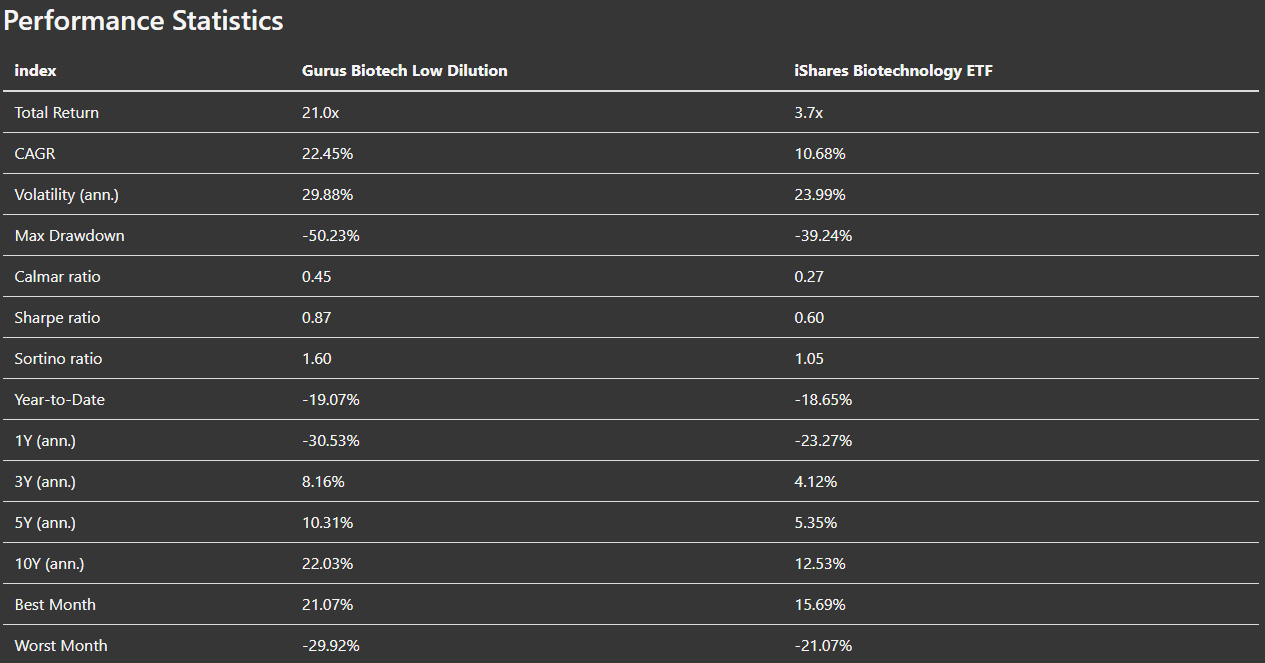

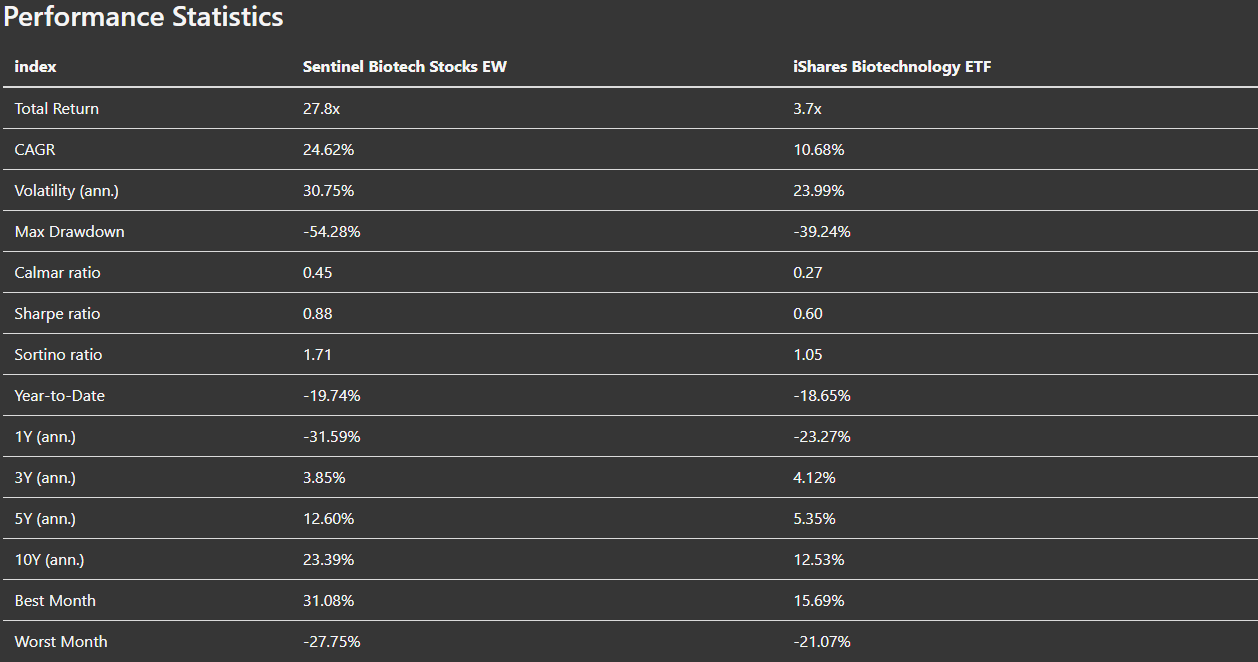

Here is the performance of an equal weight portfolio of the biotech stocks held by our managers (Gurus Biotech) relative to the iShares Biotech ETF. )

Ouch!

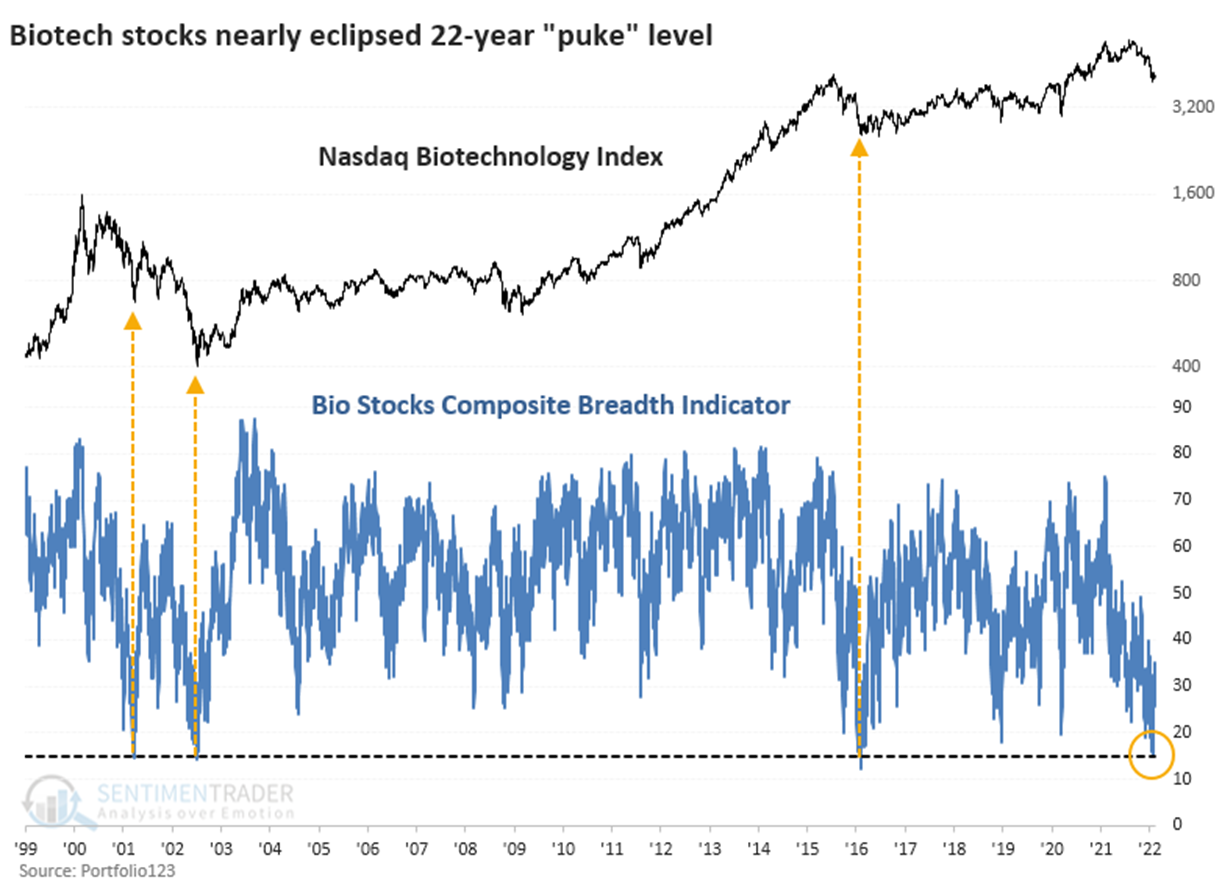

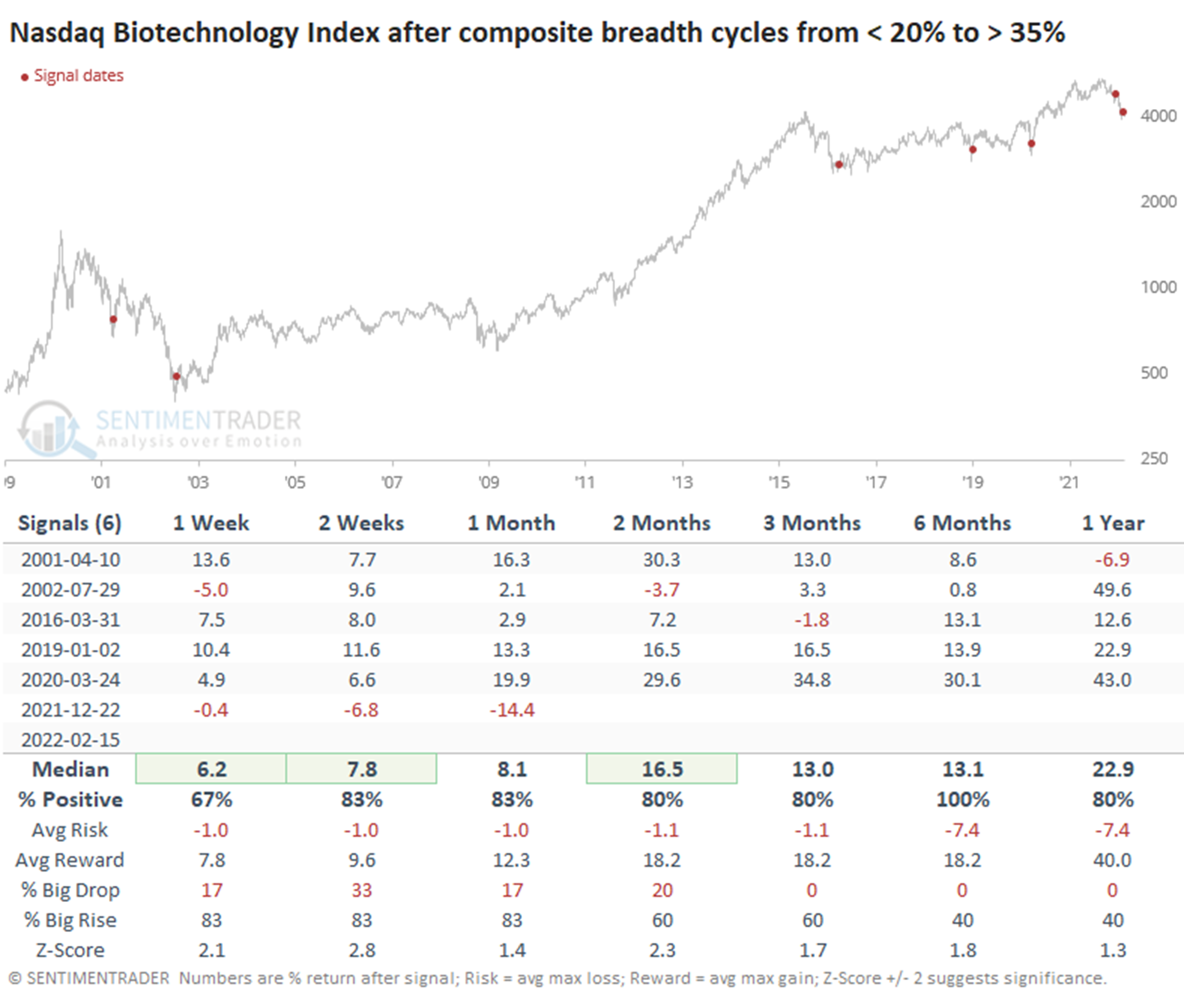

Jason Goepfert, the always insightful founder of Sentimentrader, recently posted a couple of great graphs showing of oversold the sector is.

Using his composite breadth indicator he created an oversold timing model.

As one can see, the model triggered two signals in the past 2 months with the first having the worst 1 months return of all the signal (and not by a little!).

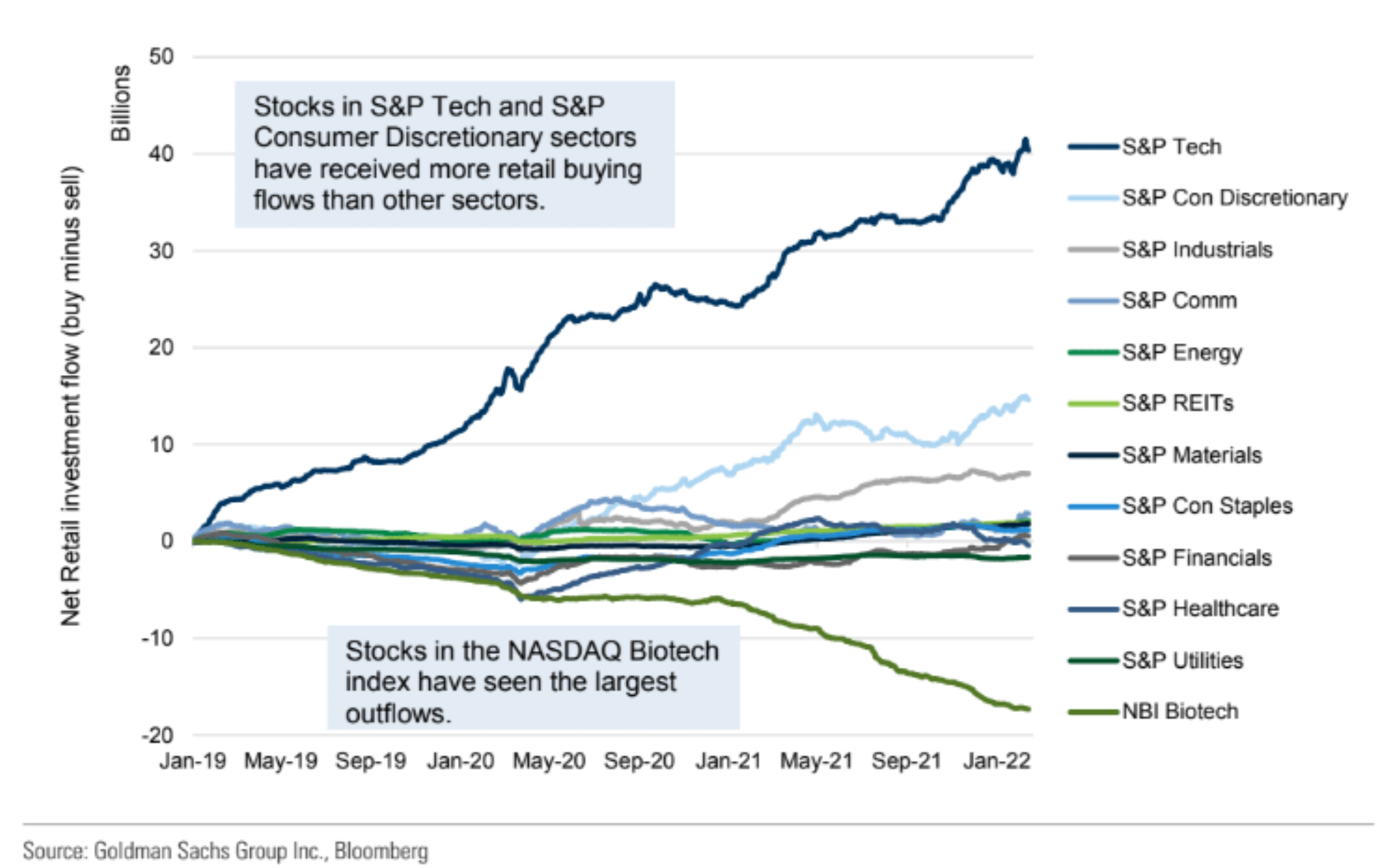

We can also see, courtesy of Goldman Sachs (h/t Thomas Callum), that

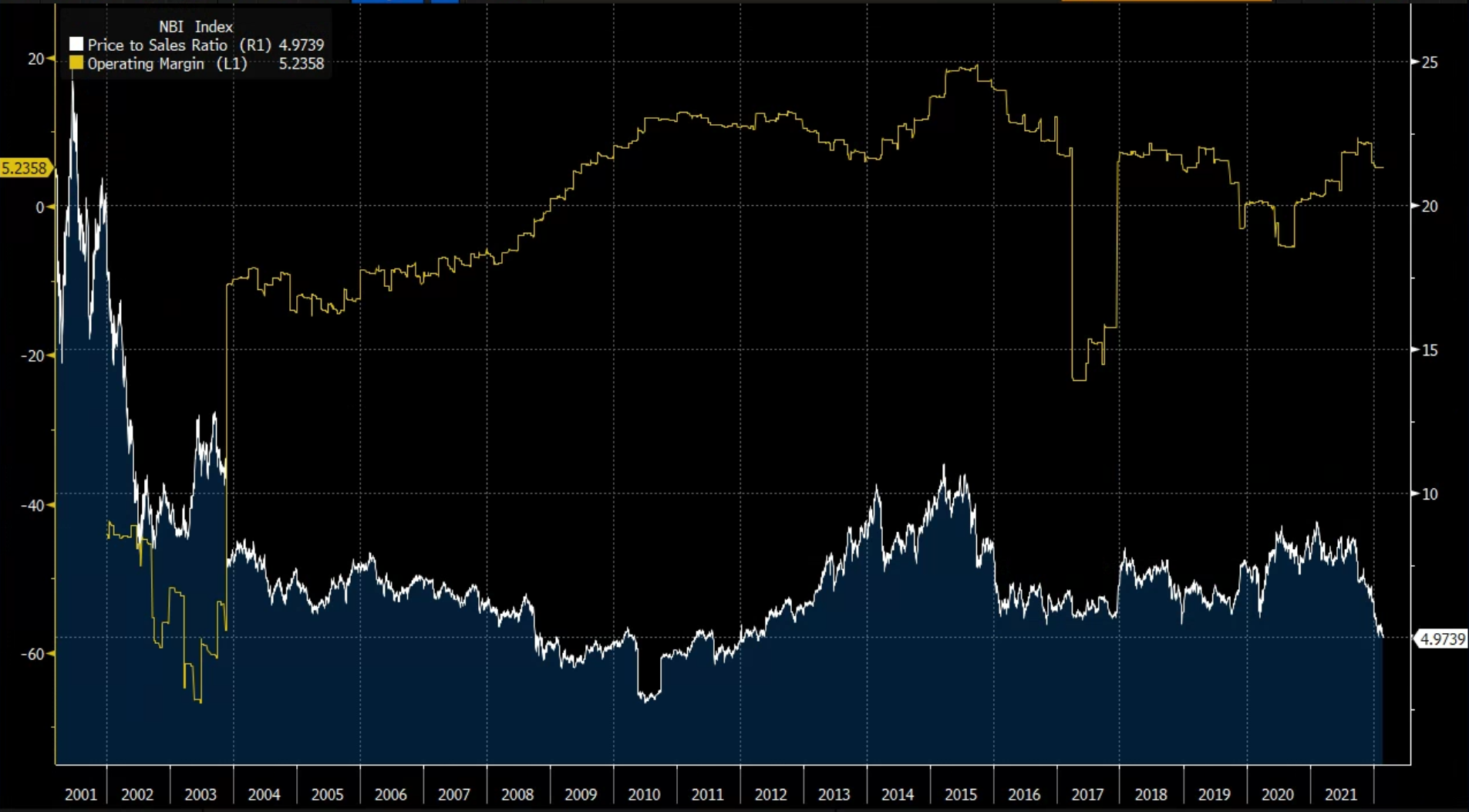

Valuing the Biotech sector is tricky as individual stocks success depends on drugs trial which are uncertain by nature.

Anyhow, looking at the Price to Sales of the Nasdaq Biotech Index, one can see that we are at the bottom of the past 20 years range while operating margin are still slightly above average. Our hunch is that the Price to Sales could still fall significantly if the overall market experience a cyclical bear market.

We believe that some large, historically successful, biotech funds are in a precarious position with some forced selling currently occurring in the market.

What to do?

Well, let's see if we can use our managers biotech holdings to come up with something simple and effective. All models use monthly rebalancing schedule if not indicated otherwise.

If we look at the relative performance of the equal weight portfolio of the biotech stocks held by our managers relative to the iShares Biotech since November 2006 we can see that the portfolio outperformed the ETF by more than 6% a year but with higher volatility and a larger drawdown.

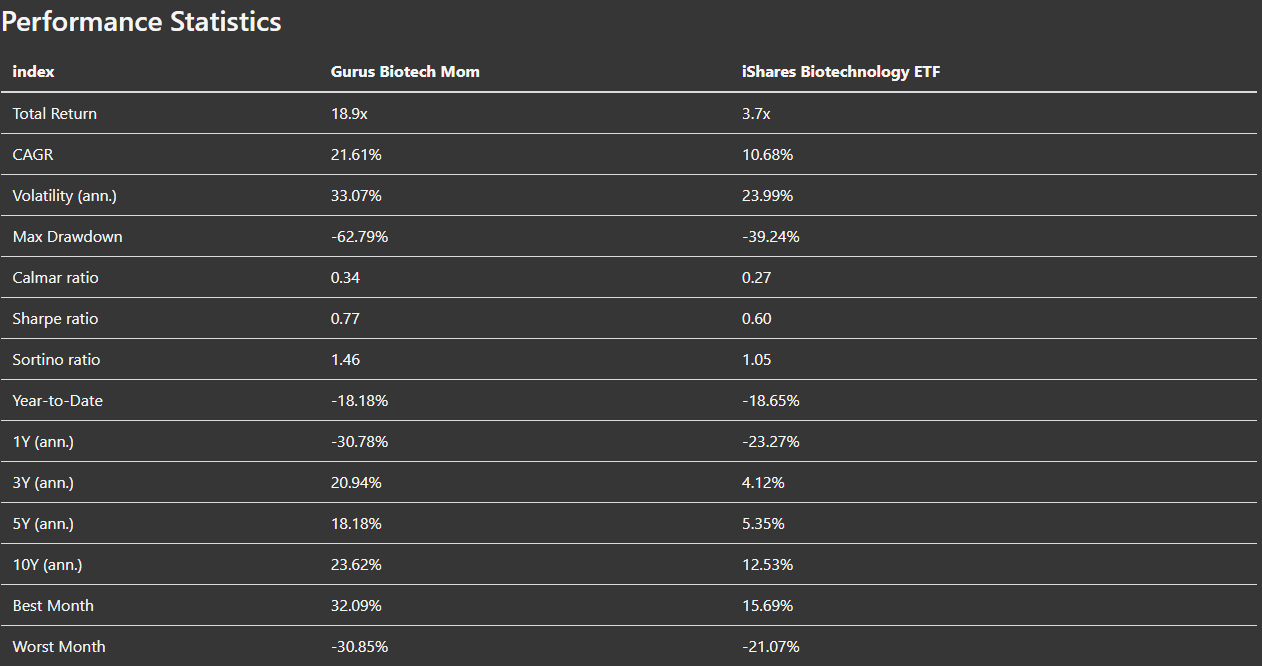

What if we only select the 20 stocks which have the highest smoothed 6 months momentum?

The annual outperformance moves from 6 to 11% but the volatility and max drawdown increase too.

Biotech companies tend to be heavy diluters as many have to print shares to stay alive while trying to successfully launch a product.

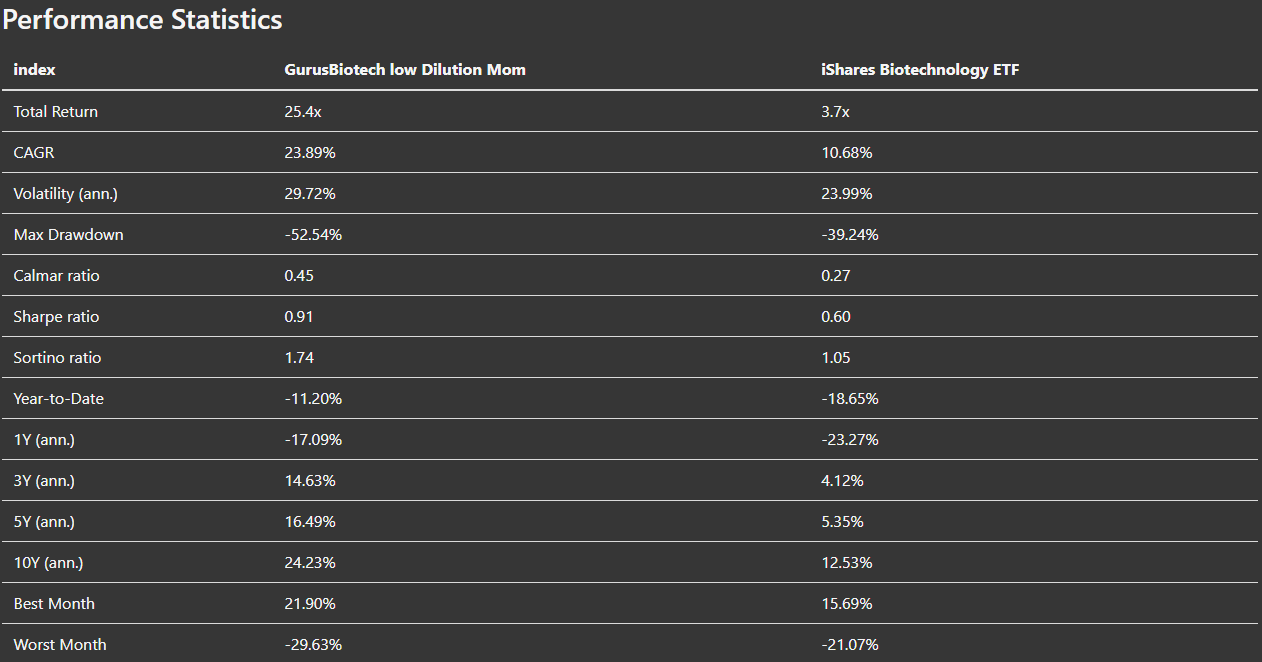

So what if we remove the 50% of the shares having the highest recent dilution from the portfolio?

The annual outperformance increases slightly and the volatility and max drawdown are lower compared to the momentum portfolio.

So both the momentum and the dilution factor seems to be producing significantly higher returns than the basic equal weight portfolio. What if we combine both.

We will remove the 50% of stocks with the highest "dilute" factor and then, from the remaining stocks, buy the 20 with the highest 6 months smoothed momentum.

The annual outperformance is now 13%. Volatility and drawdowns remain higher than the iShares biotech index though.

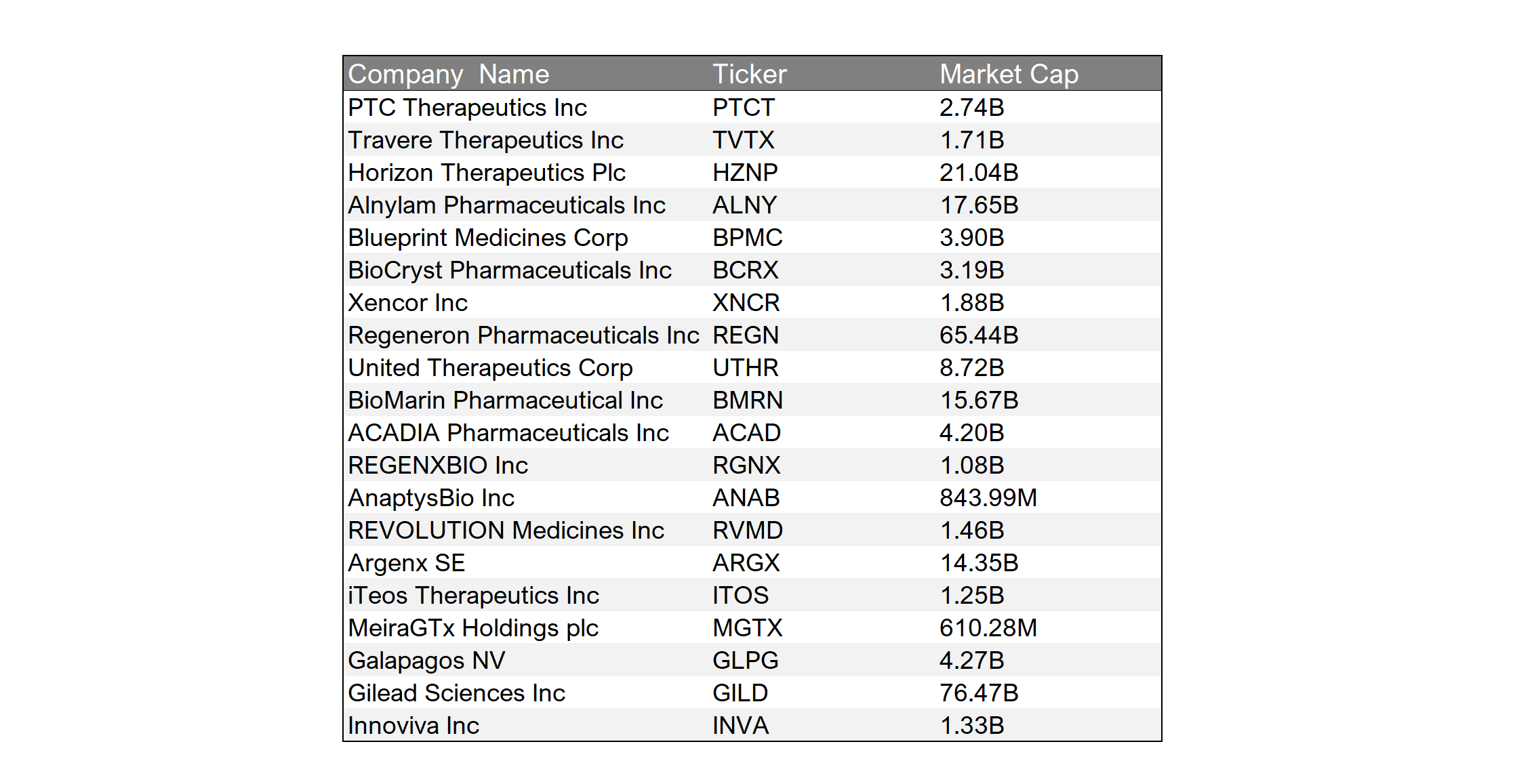

The current portfolio comprises the following stocks:

A last strategy we will look at is the performance of the equal weight portfolio of biotech stocks held in the Sentinel Gurus US strategy. The rebalancing here is quarterly.

We are thus looking at the biotech stocks of the Sentinel Gurus US Core Portfolio. The biotech stocks which have been selected from the 30+ screens run on the Managers Top Holdings universe. They have historically represented between 4-11% of the stocks selected in the Core Portfolio.

14% annual outperformance with higher volatility and drawdown. It is very similar in performance statistics to the low dilution momentum portfolio presented earlier.

A further possibility would be to add our US Beta Management Overlay to the portfolio. It is not biotech specific but adding it (net exposure moving from -50% to 125%) would make the annual outperformance reach almost 20% with slightly higher volatility and similar drawdown than the IShares Biotech ETF.

To conclude, we have no way to know if we are near an absolute bottom for the biotech sector and, as per our previous articles, we are not very optimistic with regard to major US stock indices.

The above strategies are a good substitute for long only investors who want to get exposure to the biotech sector.

Given the recent underperformance of our manager biotech holdings relative to the sector and given that our market beta overlay is currently recommending a market neutral position and likely to recommend a net short position if the markets continue to fall, the low dilution momentum strategy with market timing seems to be a good place to put some money to work already now.

About us:

NAVA Capital SA (‘Nava’) is a Swiss based advisory firm. It is a spin-off of a large Swiss single Family Office and it has developed since 2005 several proprietary quantitative strategies under active use, managing significant amounts of money.

Kroma Capital Partners Ltd. (‘Kroma’) is a Dubai based, DIFC incorporated - DFSA regulated entity holding a Category 3C license. This license allows Kroma to Managing Assets, Holding and Controlling Client Assets, Arranging Credit & Advising on Credit, Advising on Financial Products and Arranging Deals in Investments. As a distributor we have advised clients on funds and bespoken solution since 2017 with assets raised > 1.3 bn $. As an adviser we advise 3 investment vehicles: a fund of private markets funds, a volatility fund of funds and a US long/short equity fund.

Nava and Kroma have entered into an exclusive partnership offering quantitative investment solutions under the Sentinel Family of Strategies. We offer institutional investors solutions with our Sentinel Gurus US Long/Short strategy, our Sentinel Enhanced Long/Short indices strategies (which can be run on any sufficiently large stocks universe), our asset rotation strategies and our volatility strategy. All strategies are highly liquid and offer full transparency and Mark-to-Market pricing.

Bespoke investment solutions are available as:

· AMC’s on the UBS Platform

· European Funds under the OpenFunds SICAV AIF / UCITS

· Cayman Funds (exp. 2022)

If you are a qualified or an accredited investor and want more information on the above, you can contact us at:

contact@nava.capital

If you have any comments on this article, you can contact us at:

blog@nava.capital