October 30, 2023

Summary

- Farmer’s wisdom

- Recession in sight

- Households growing despair

- Corporations, same dynamic

- Private Equity: don’t fall for it, please!

- Housing, expect non-linearity

- Europe’s “chant du cygne”

- China, could it be worse than feared?

- Intermarket canaries

- Is the Treasury looking toward next November when managing the TGA?

- Buybacks rolldown

- Unfriendly valuation

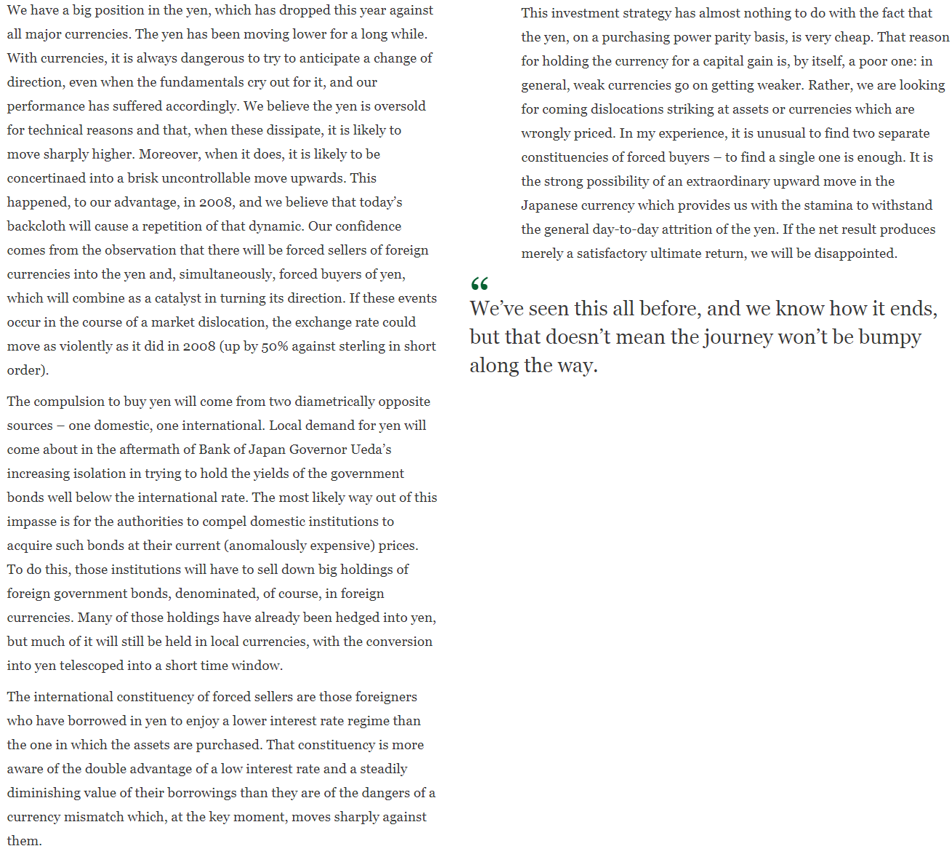

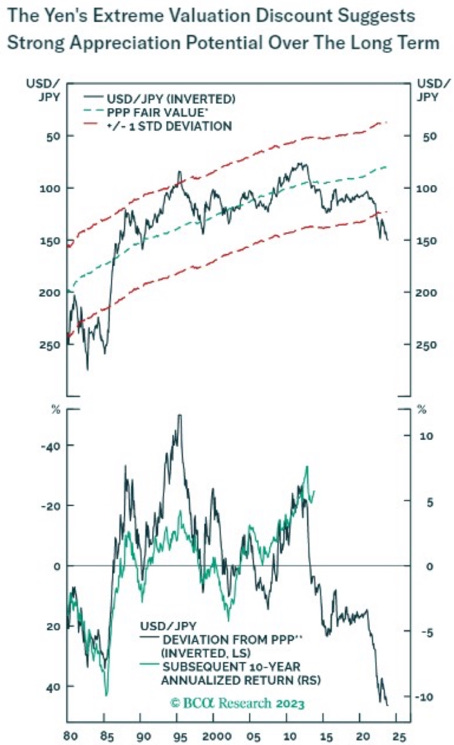

- Cheap Yen

Macro – Why?

Sometimes analysts over complicate…

We like what we call «le bon sens paysan» (farmer’s wisdom) in French.

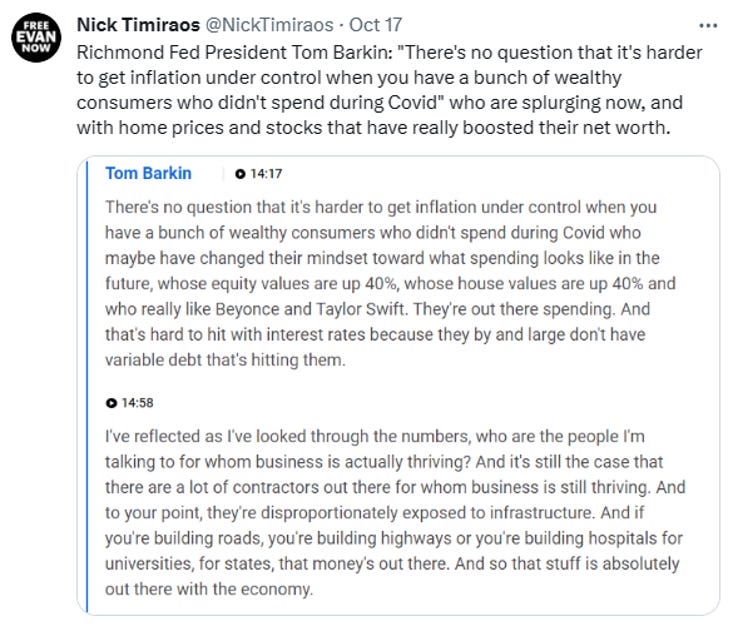

Tom Barkin of Richmond Fed seems to agree…

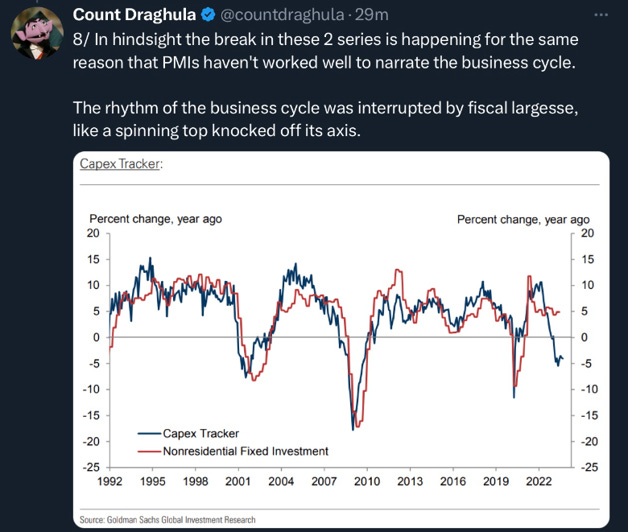

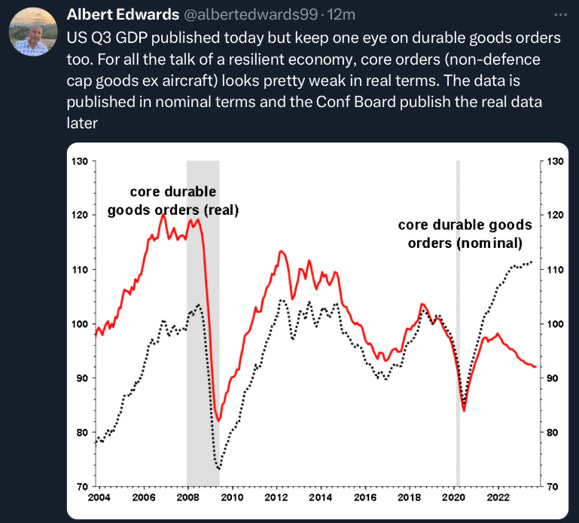

And those fiscal largesses also explain why PMI's and capex trackers have not work up to now…

Macro – Recession

Money illusion in all its splendor…

…but the days of reckoning are approaching very fast!

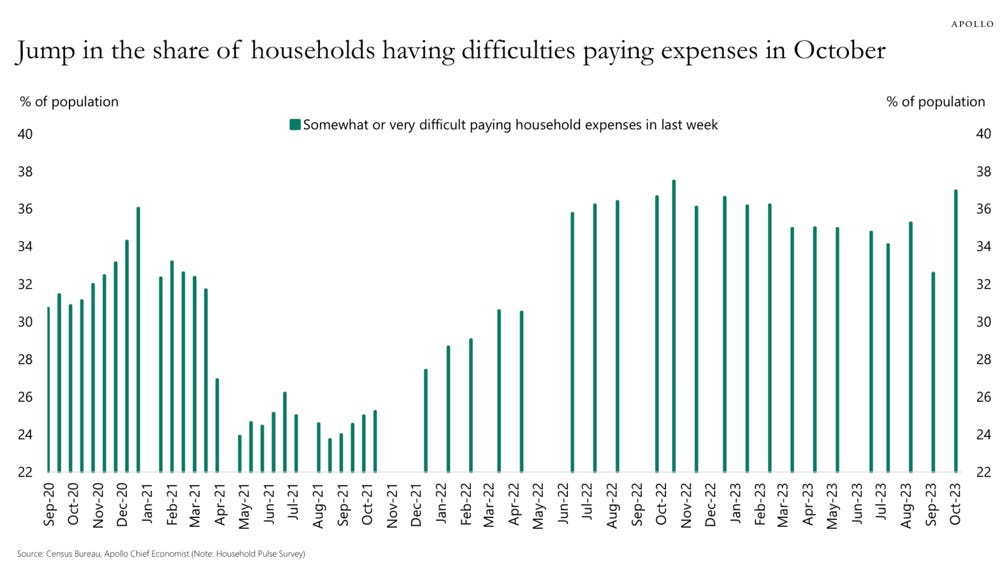

Macro – Households

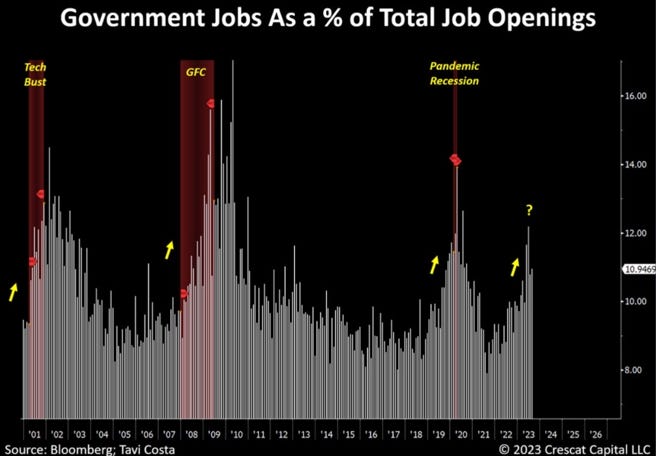

Another indication that the employment picture might not be as rosy as it seems..…

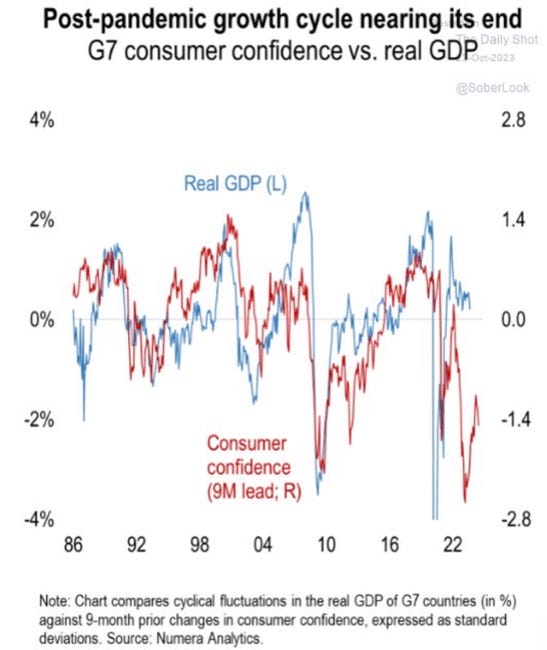

…and consumer confidence has been showing it for some time too

Our “rising the income ladder stress” is playing out as expected.

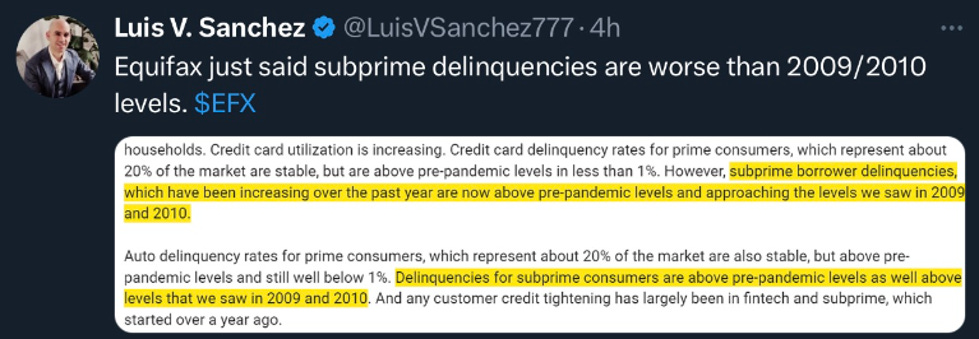

As subprime borrowers stress is slowly getting of the charts…

Macro – Corporates

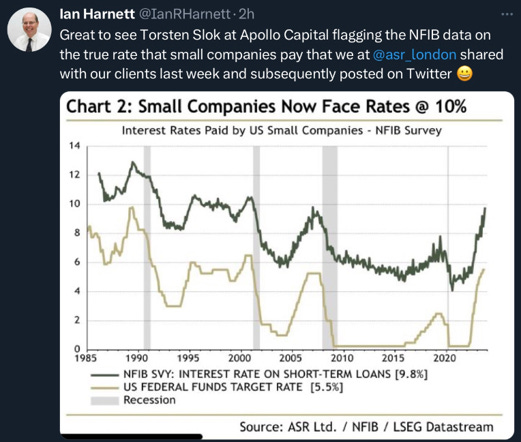

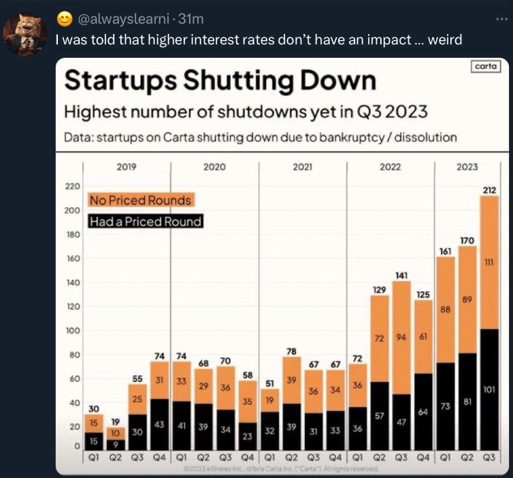

Same is true for corporations…

…as postponing refinancing or rising new debt becomes harder and harder the longer rates remain high.

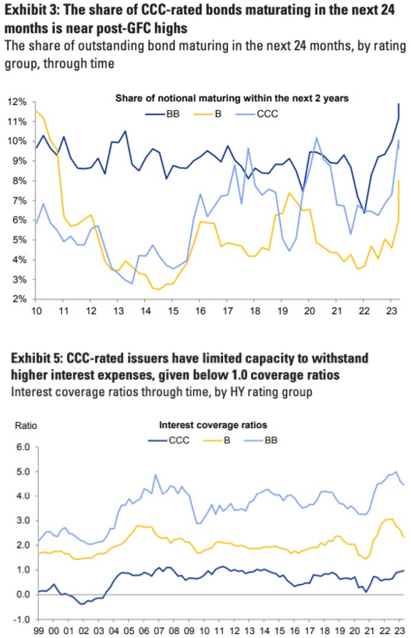

Macro – Mark to Market

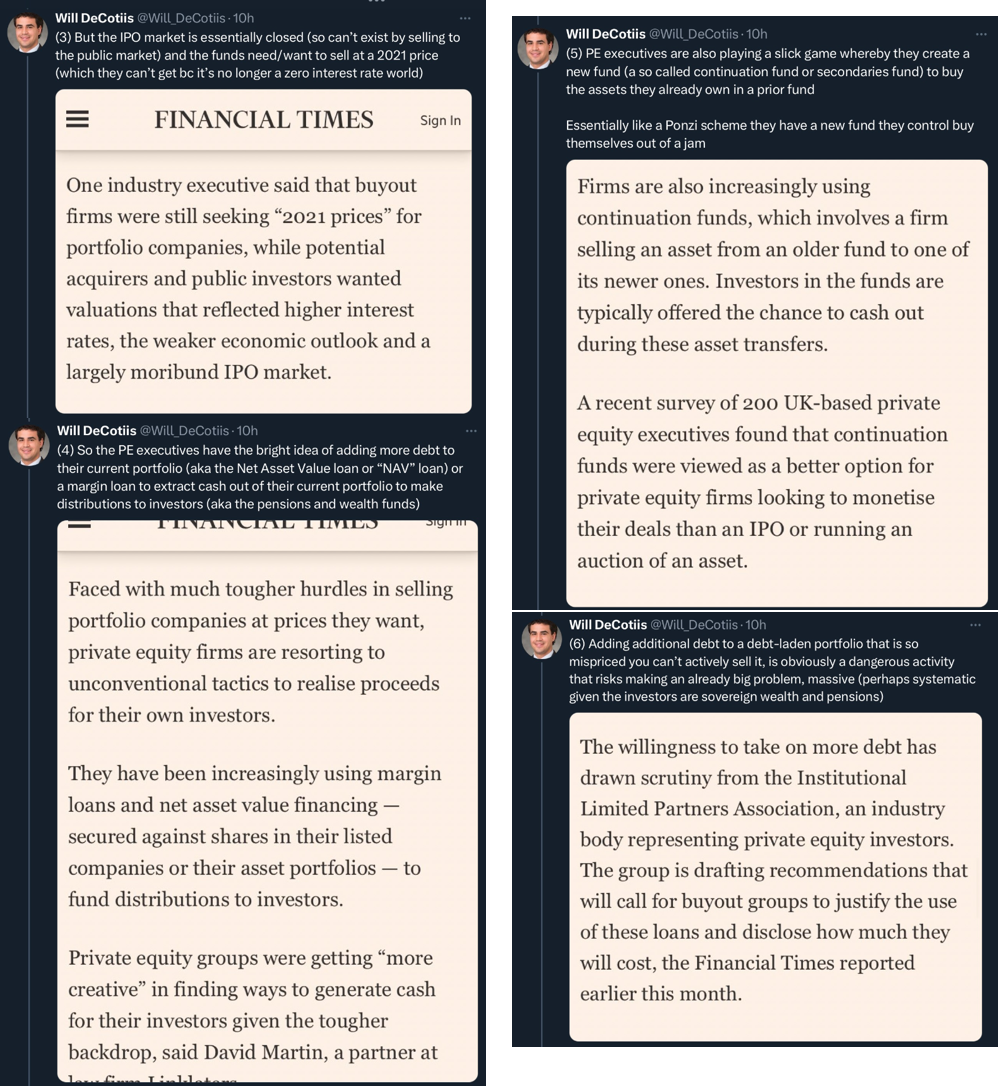

We have long argued that the Private Equity industry was where the asset liability mismatch was the most glaring in this cycle (as the banks were in 2007-2008). They are “ingenuous” but…

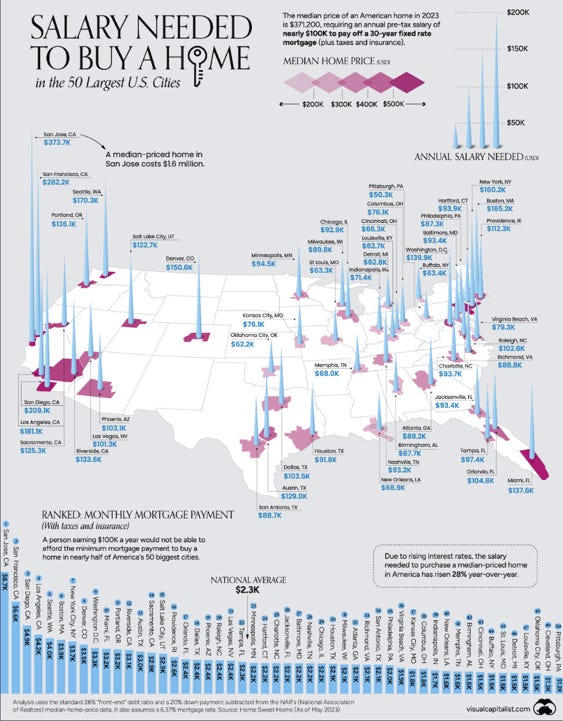

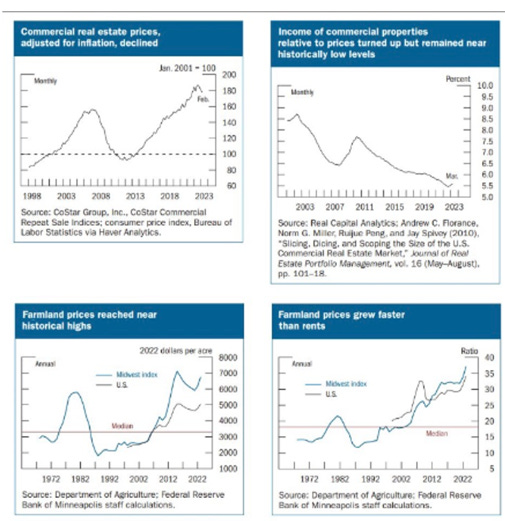

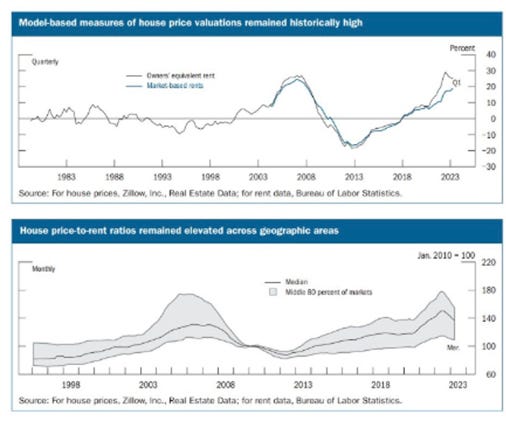

Macro – Housing

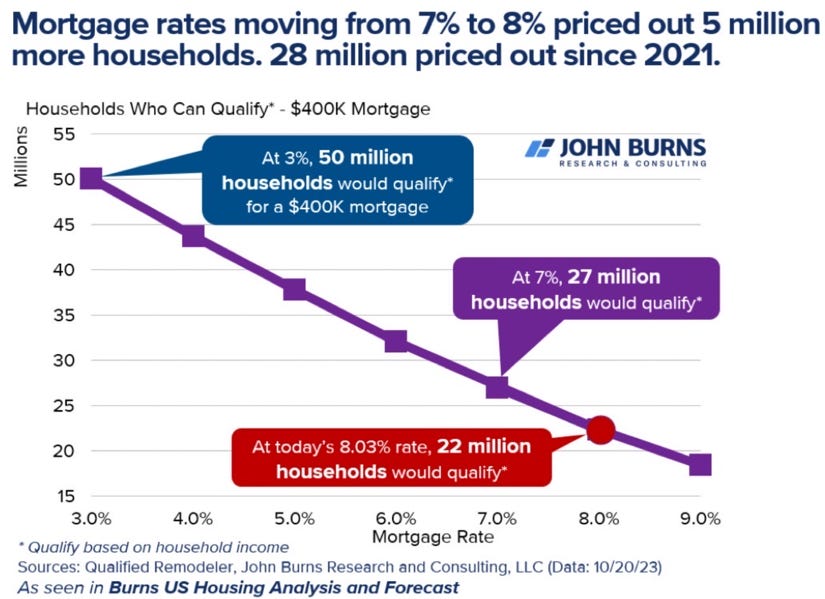

New buyers are slowly being priced out the markets… wait for employment to break down decisively and…

Visual Capitalist, as always, has a beautiful way to show it!

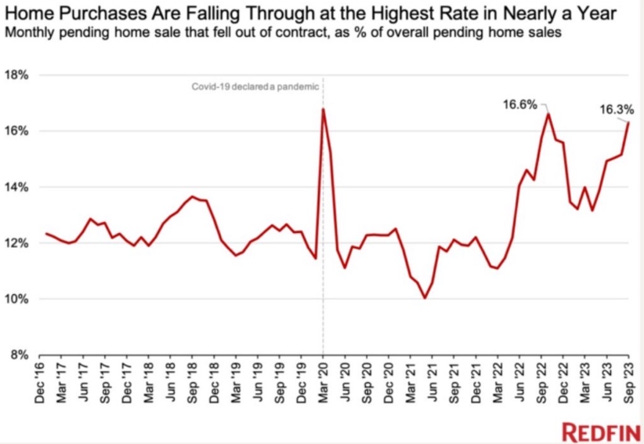

… explaining the rapid increase of pending home sales falling out of contract….

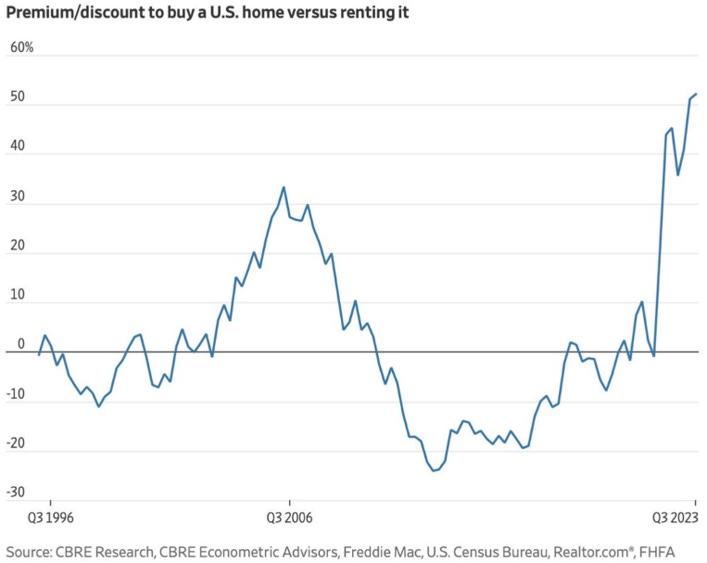

Given the coming surplus of rental properties to hit the market in the coming months, buying instead or renting will become increasingly irrational.

What if…

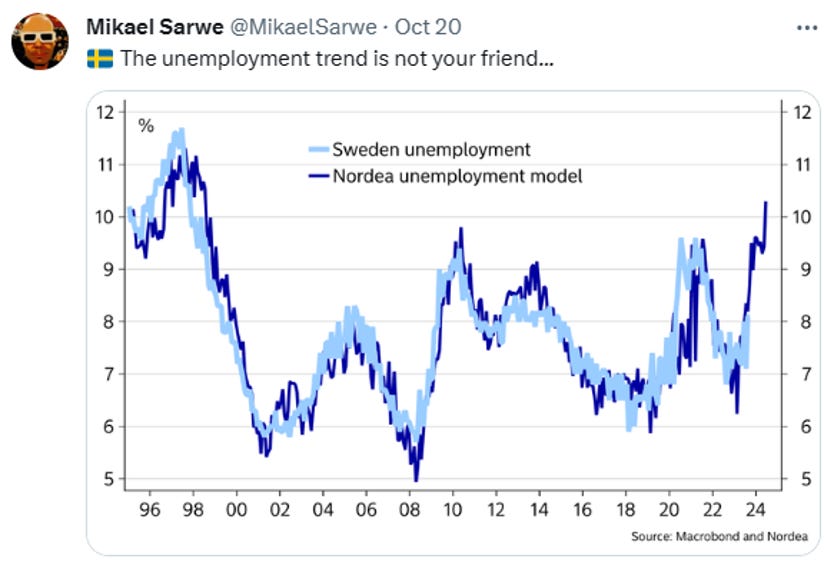

Macro – Outside of the US - Europe

Having lived 13 years in Sweden and experienced the relentless rise in the housing markets and leverage in all of its forms, I would not be surprised if it becomes one of the biggest victim of the current cycle.

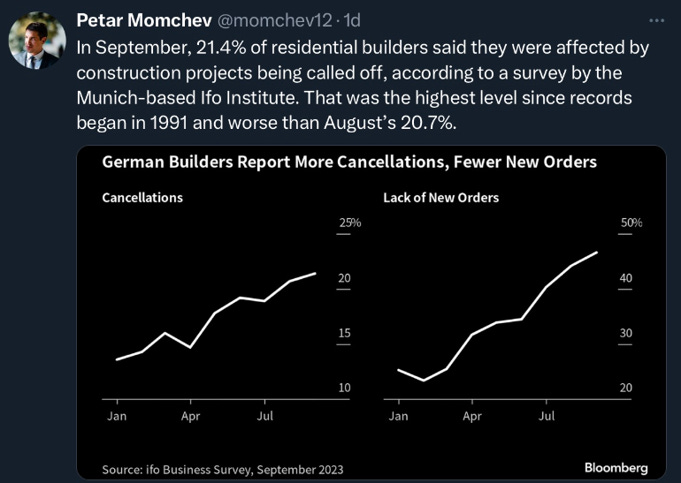

The German real estate market (the whole economy to be honest) is not looking good either…

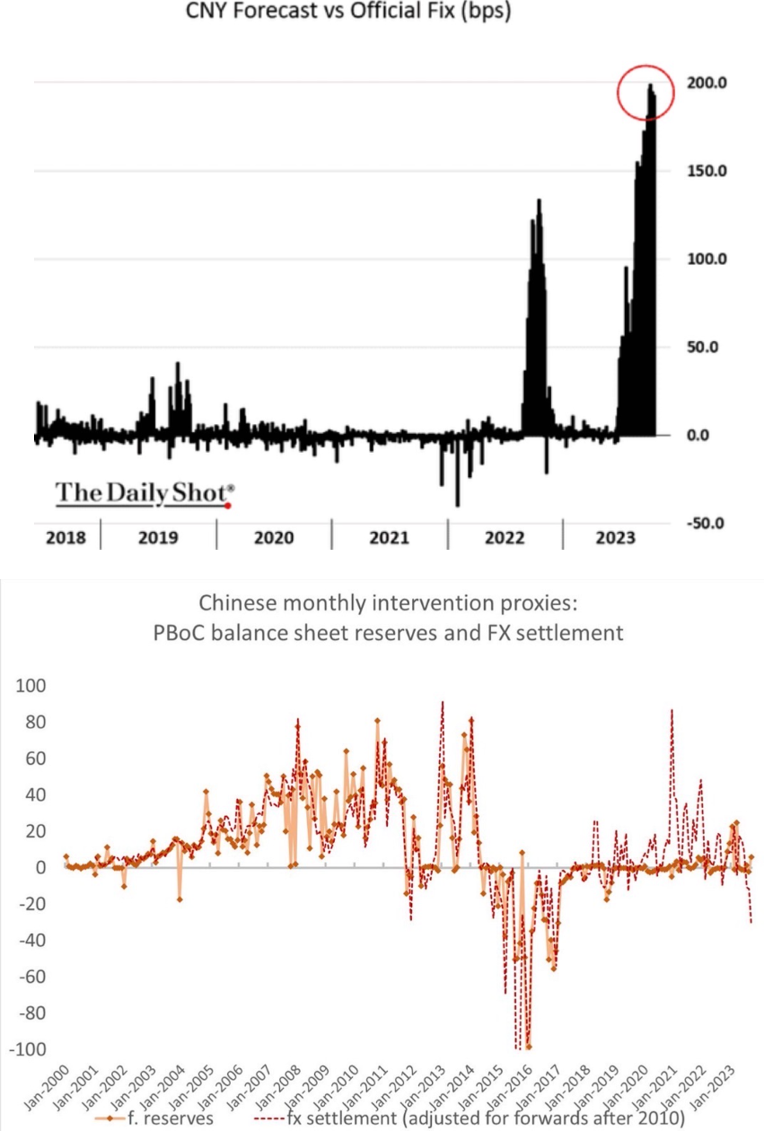

Macro – Outside of the US - China

We have shown similar graphs some weeks ago… the Chinese government is trying to avoid a further decline in the CNY as much as it can.

Bob Elliott sees the current developments closely resembling a BoP style crisis…

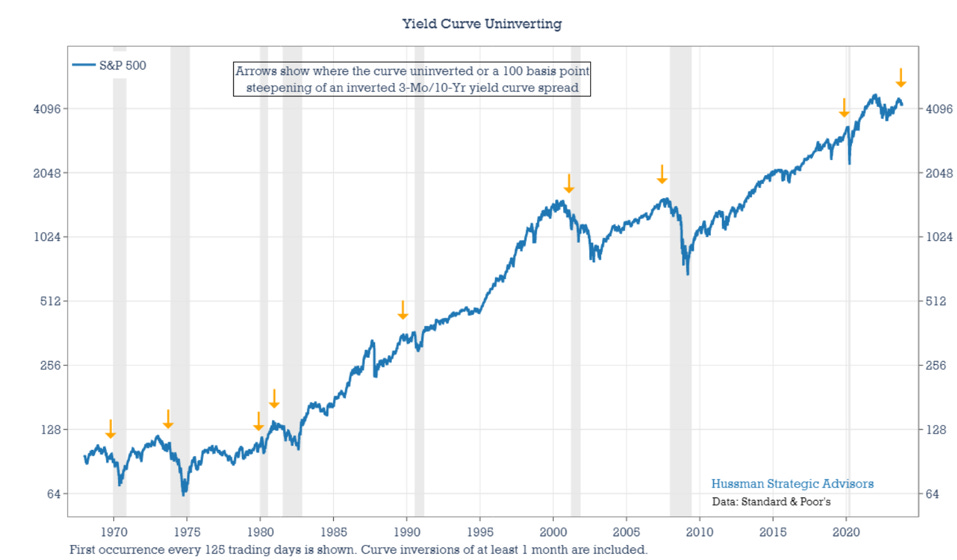

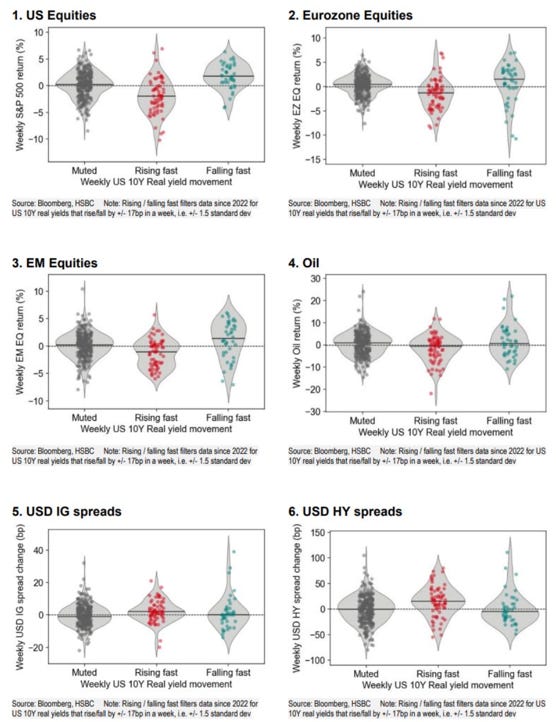

Market – Intermarket

Real yields are starting to be interesting. The corollary is that real rates are high given the macro growth which is not a positive for risky assets…

As the distribution of returns shifts downward with a fatter downside tail when rates move quickly up.

Other canaries in the coalmine…

Market – Liquidity

Could the Treasury increase TGA now to be able to spend without having to borrow during the few months preceding next years presidential election?

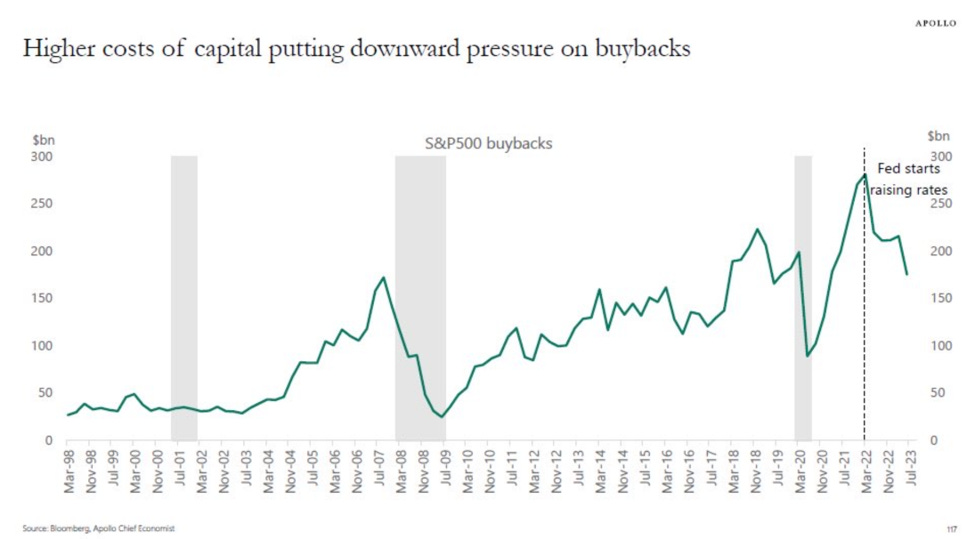

It has been our contention in previous MashUps that buybacks would decline. This seems to be happening now…

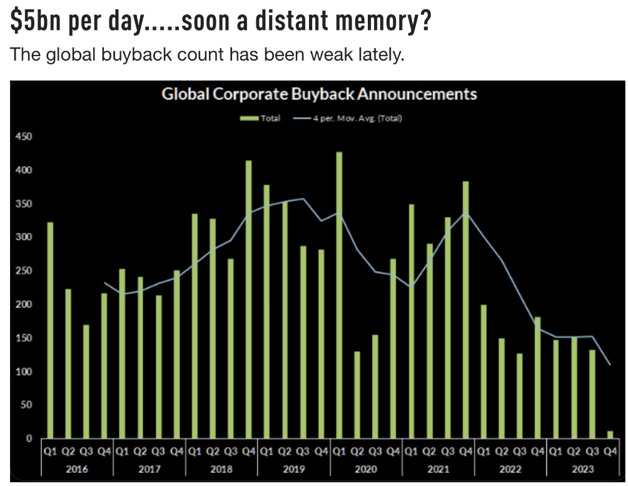

…and not only in the US.

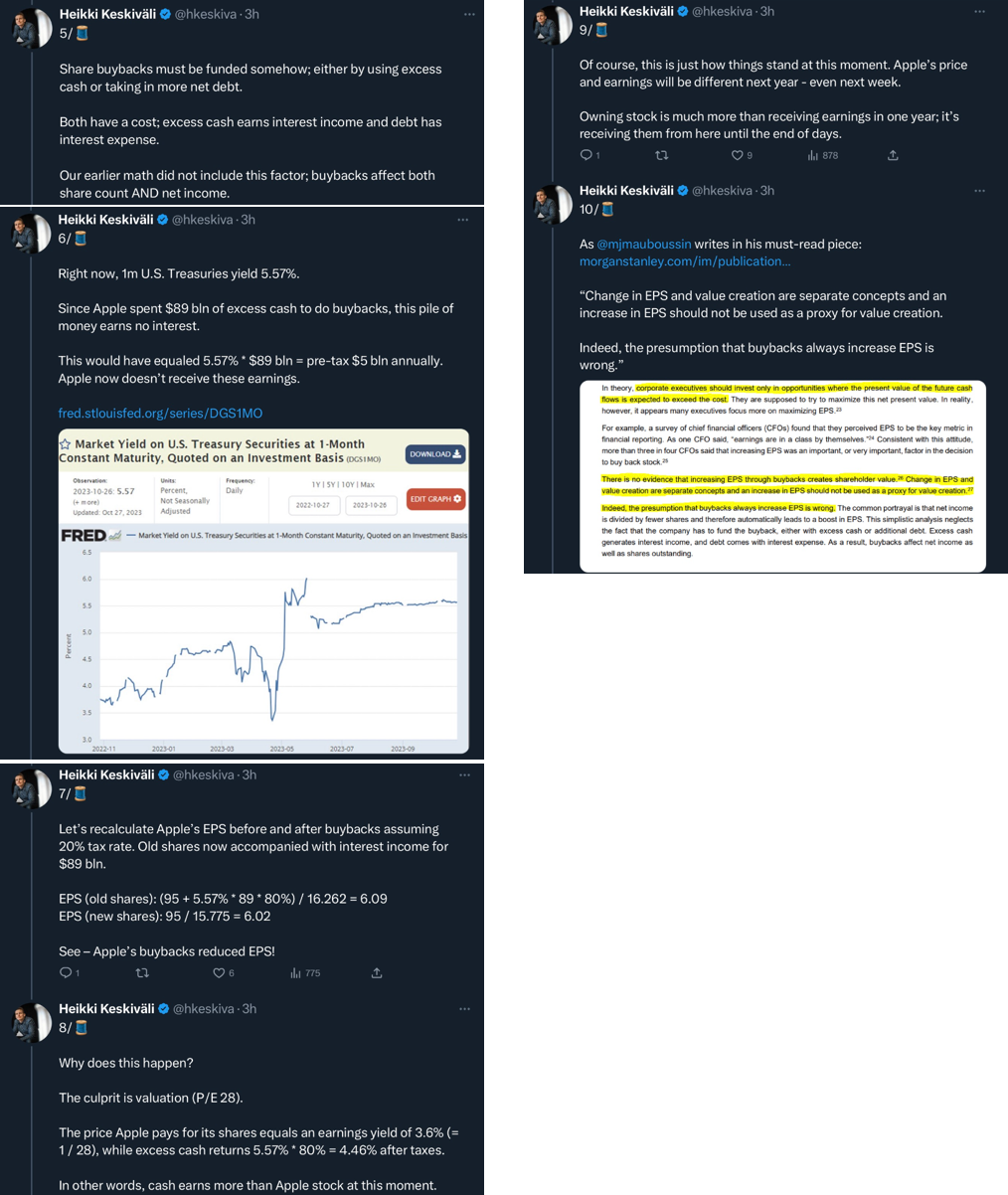

Now an excellent thread on why it would even be rational for some of the strong balance sheet buyback gluttons, to lower the number of stocks they buy back (taking the example of Apple).

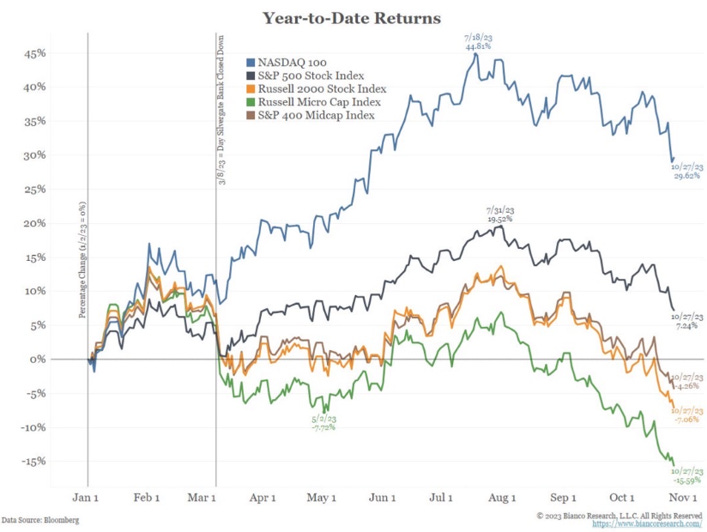

Market – Breadth

Uniformity in risk taking is absent…

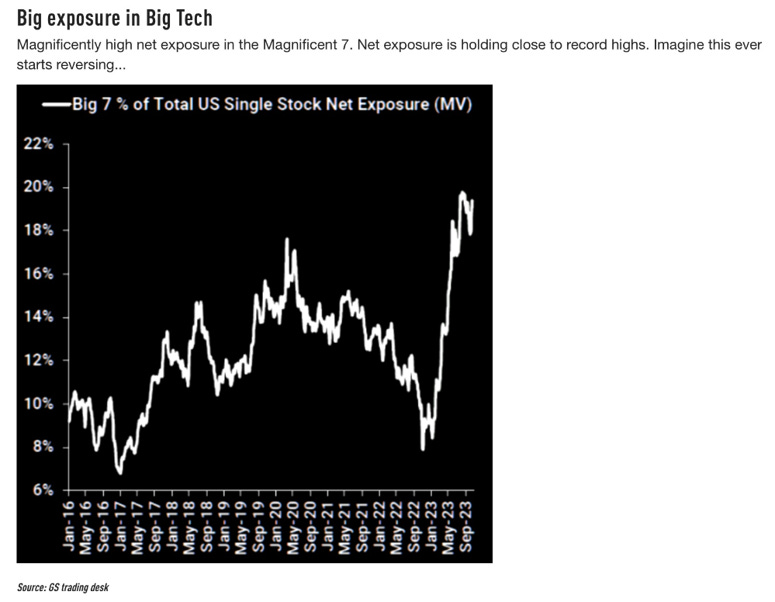

…while everyone is on the Magnificient 7 bandwagon… AAPL better not disappoint this week…

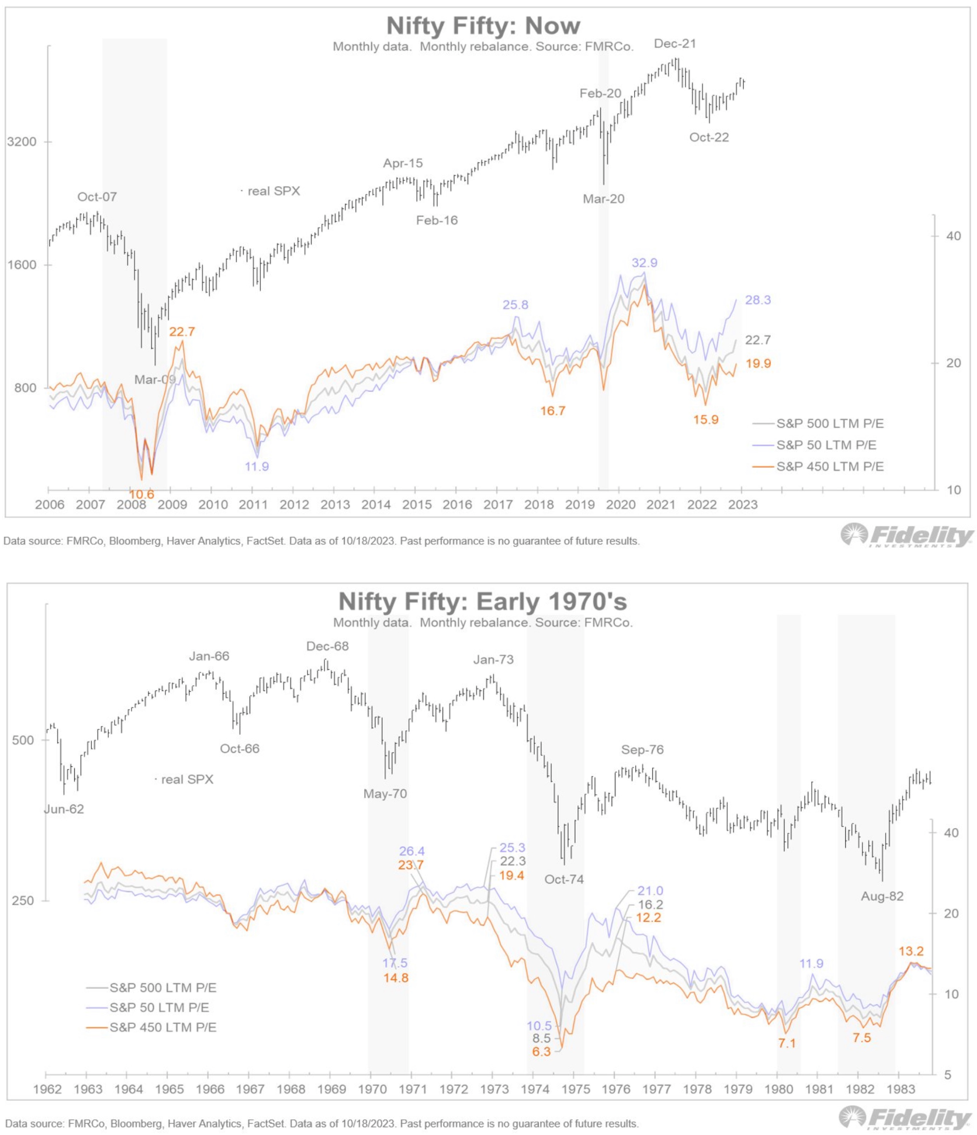

Market – Valuation

The lack of uniformity can also be seen in the large valuation discrepancy (some of which is probably warranted given the quality of the balance sheet of some of the largest index weights) between a handful of large stocks and the rest of the market.

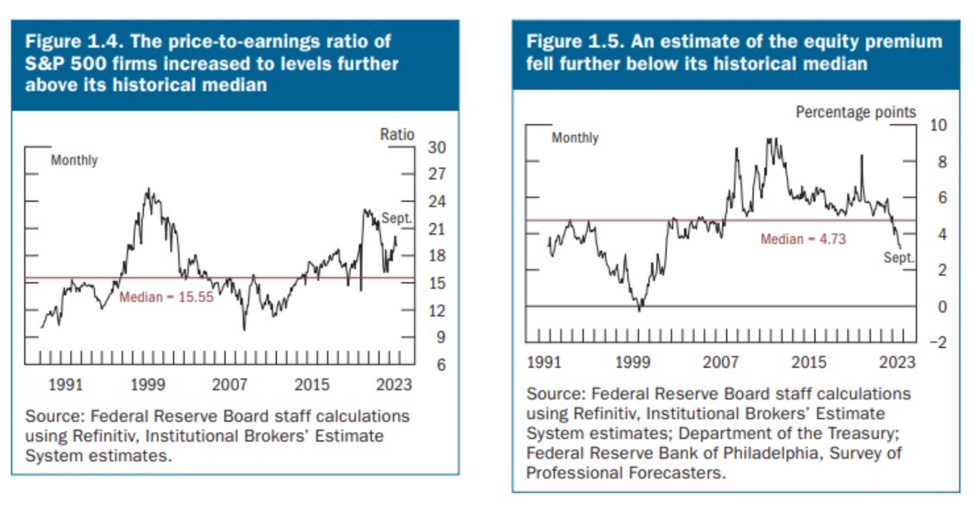

Note that even the Fed does not think equity markets are cheap…

… same is true for other assets… Will it take responsibility one day?

The combination of overvaluation and rate pressure is unprecedented.

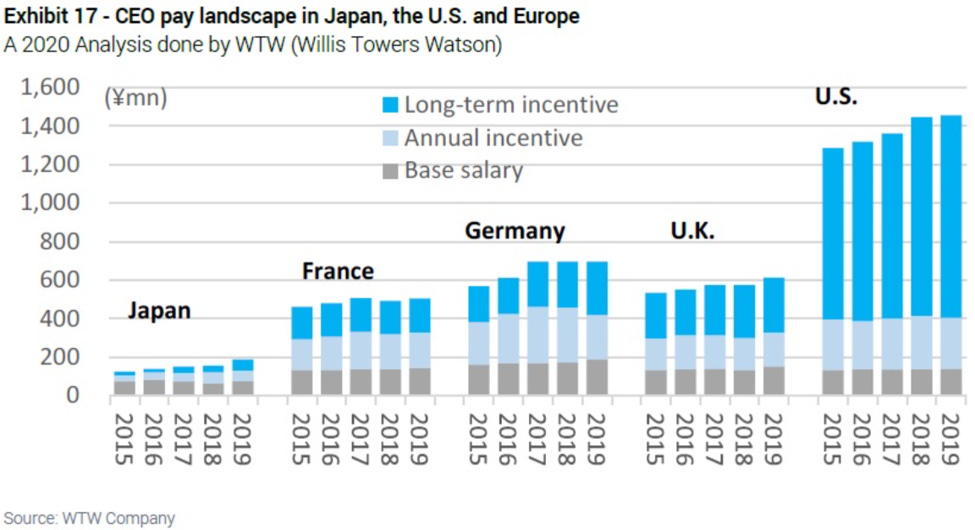

Market – Japan

Beside valuation and a more shareholder friendly environment, another reason why we think investing in Japan is a no brainer is the Yen...

While we have rarely complained about the wealth accumulated by companies' founders with significant skin in the game, we have often looked with contempt to the CEOs making millions with little skin in the game and absolutely no consideration for the long-term prospect of the company they “manage”.

Japan is a refreshing exception in this context!

Others