January 21, 2024

Summary

•2023, a year to remember. Was this time different?

•Recession still on the table and what if it already started?

•Markets are pricing the best of all world.

•Political shenanigans are, again, to be expected in 2024. Be reactive!

•Inflation, a last cyclical hiccup?

•Don’t exclude a deflation scare during the coming downturn. Longer-term this is another story.

•Investors positioning is now max long.

•Invest outside of the US stock market, favor cash generating small caps!

•One should be short vol/long carry in the belly and long vol/short carry in the wing. Investors are doing the reverse now. Nasty accidents waiting to happen.

Macro – 2023

2023 was a challenging year in many respects.

Not only did the market rose with very little participation (at least until early November) but, while the jury is still out, the recession we expected for Q3 or Q4 2023 failed to materialize (the jury is still out but…)

Our models could not anticipate the level of fiscal shenanigans and largess the current administration would come up with. We need more imagination!

Macro – Looking ahead

What the markets are anticipating?

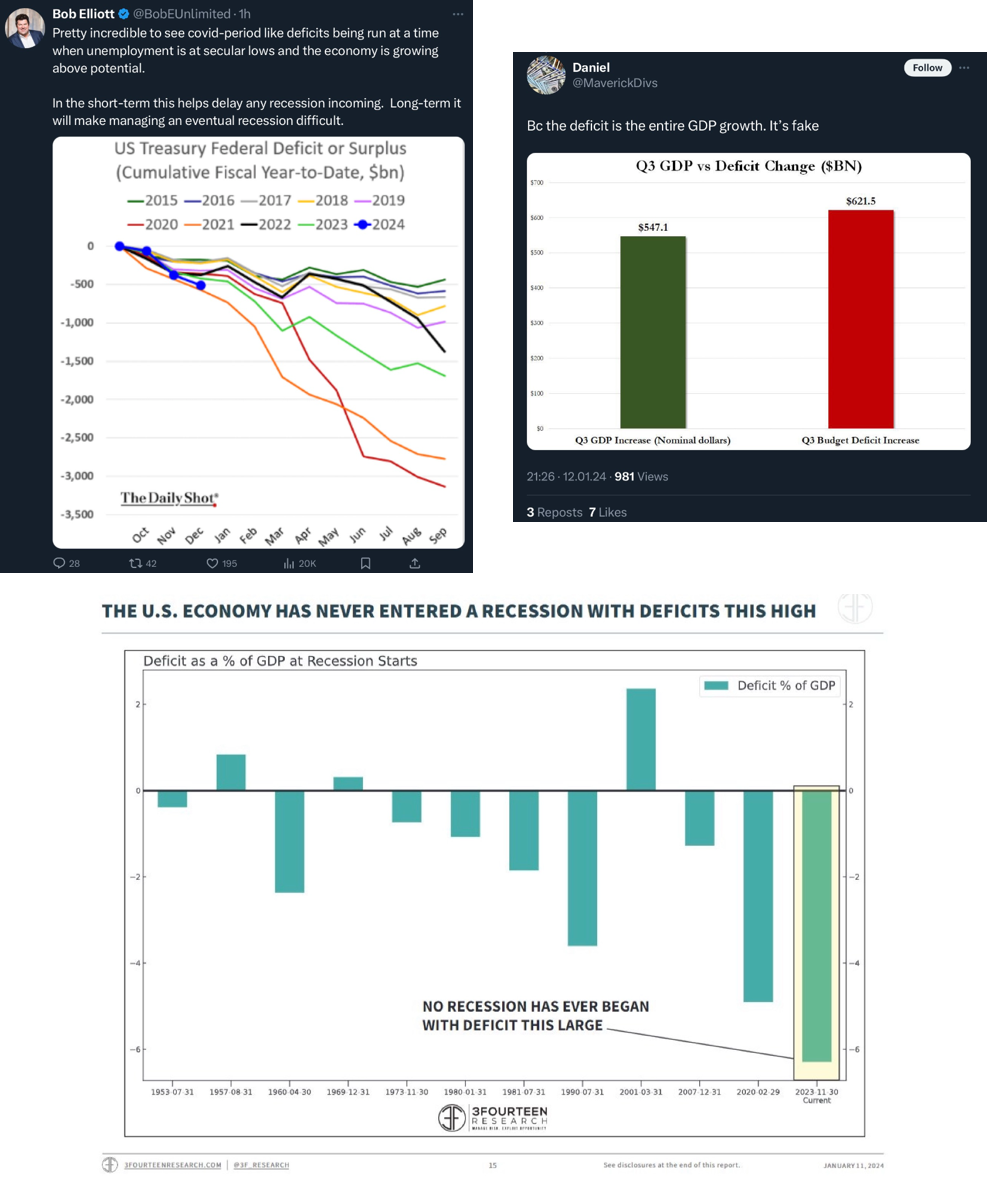

Both politics and central bank policies will determine if we achieve the soft/no landing by kicking the can down the road or, as we still expect, the US enters (or continue the current) recession.

Macro – Looking ahead – Fiscal Policy

MMT on steroid… what counts here is the second derivative, not the absolute level but the momentum.

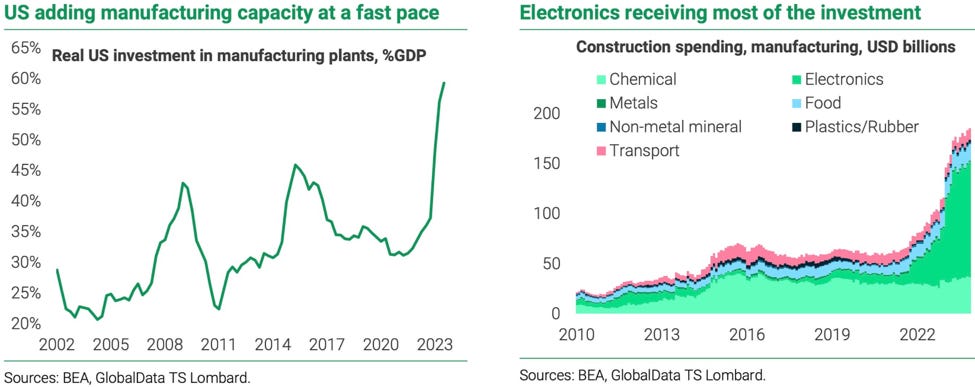

The various infrastructure/reshoring investment programs are likely to continue unabated or even accelerate slightly.

Students loan borrowers won’t face any penalties for missed payment until later this year. Election quand tu nous tiens!

Others might need some “help” too.

Macro – Looking ahead – the Fed

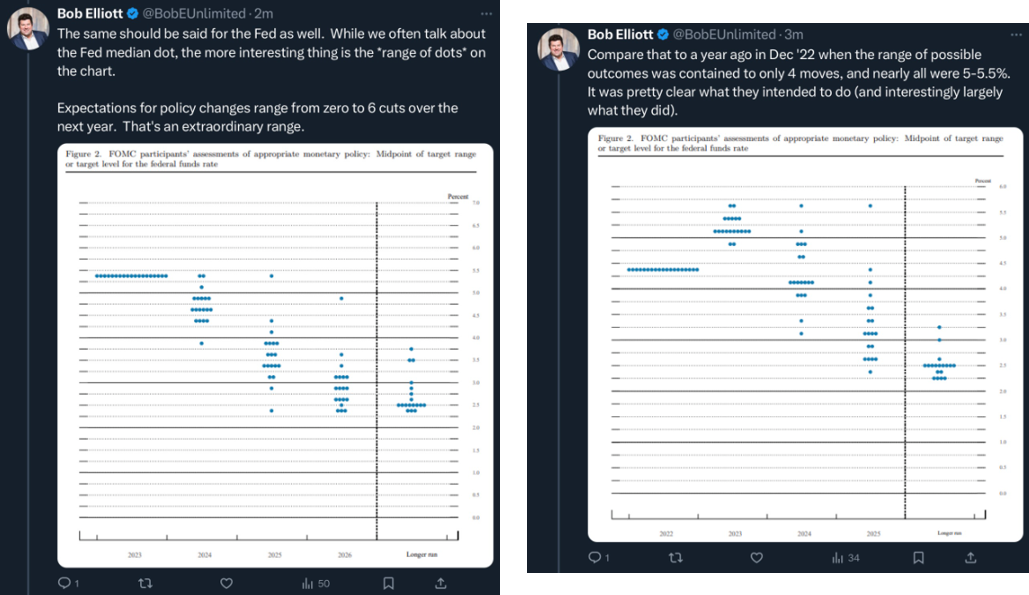

As much as it wants to pretend it is immune to political bias, the Fed is not. Ask J. Yellen and L. Brainard. The huge range of SEP forecast for 2024 is just a reflection of this.

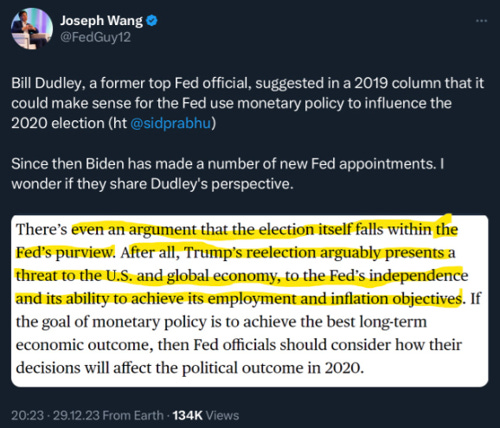

Some are saying that J. Powell surprising dovish (or market wanting to perceive him as dovish) in December was triggered by a sudden realization that J. Biden could loose to D. Trump this fall. We do not doubt that some members would do whatever they can to support the incumbent President, we do not think this is the case of J. Powell or C. Waller.

Indeed…

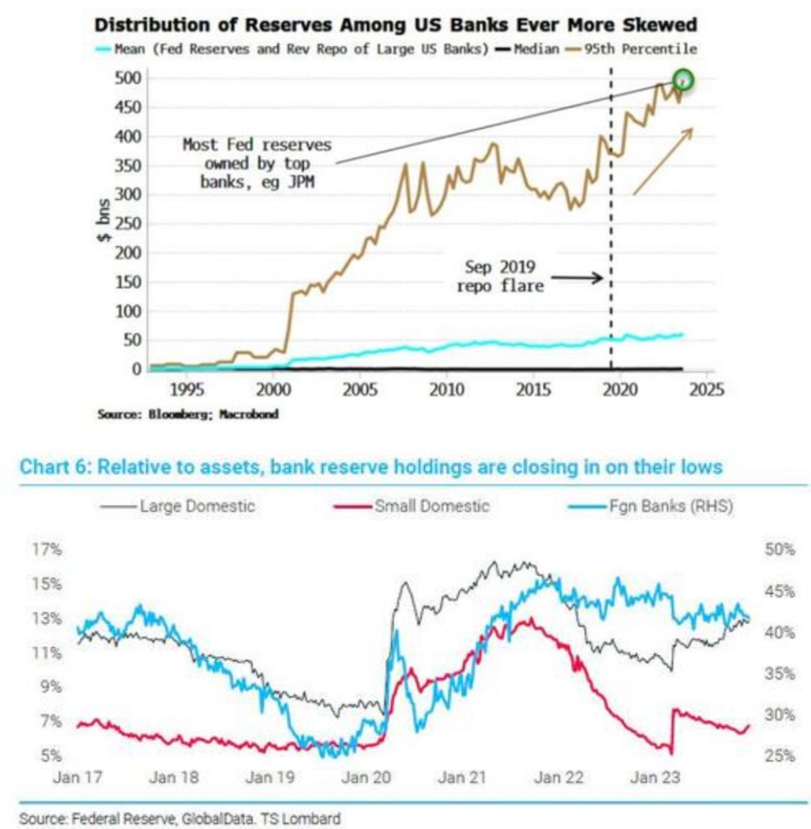

What about the balance sheet? L. Logan talked about it and we now know, thanks to the minutes, that it was a subject during the last Fed meeting. While reserves seem plentiful on aggregate, the devil is in the details. Many small domestic banks are probably under-reserved now…

And we are not talking about this…

Or unintended consequences…

Macro – Looking ahead – the Fed and others

CB liquidity and M2 diverging with risky assets. First graph is Fed liquidity: Fed held securities –(TGA+RRP) + BTFP. The second graph is global CBs balance sheets + M2. The third graph is global CBs balance sheets.

The recession call is important because…

And the curve un-inversion might not be as different as before previous recessions

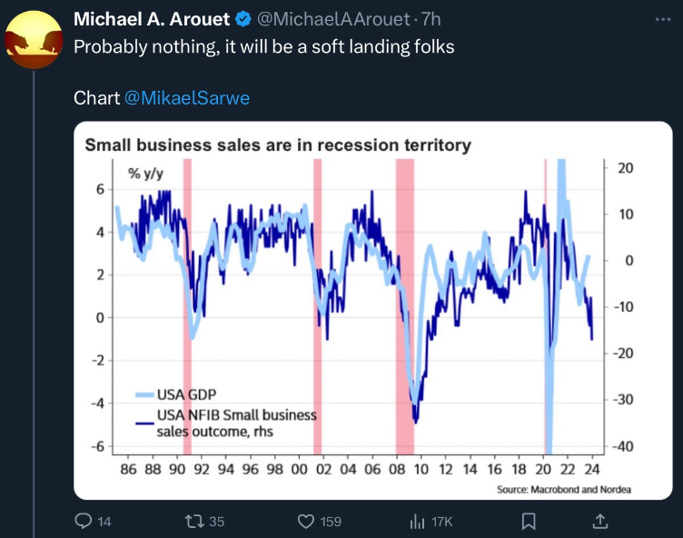

Macro – Macro – Leading Indicators

Small businesses are worried about higher prices and expecting lower sales. Our rolling recession framework (metastasizing slowly from the weaker, households and corporate, to the stronger) in all its splendor.

And the curve un-inversion might not be as different as before previous recessions.

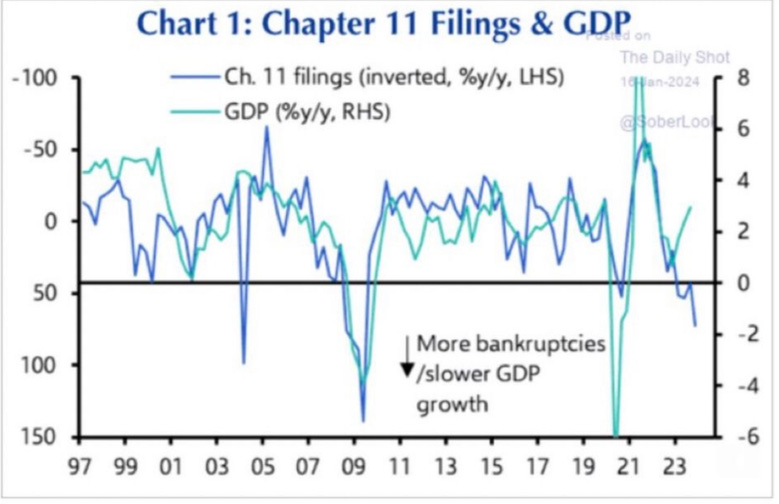

Soft surveys seem to have lost some of their luster (reflexivity in a world where adjustments can almost be made in real-time?) but we would not dismiss them completely yet and …

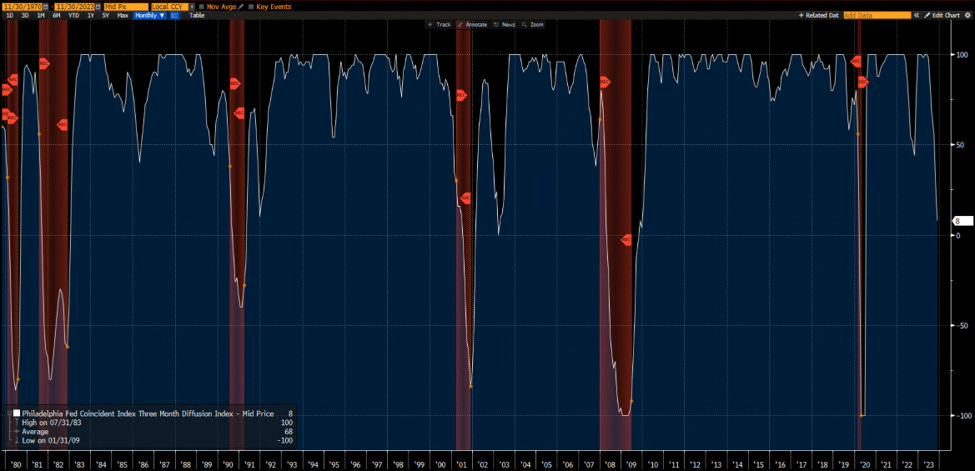

…Philadelphia Fed States Coincident diffusion index not looking great either…

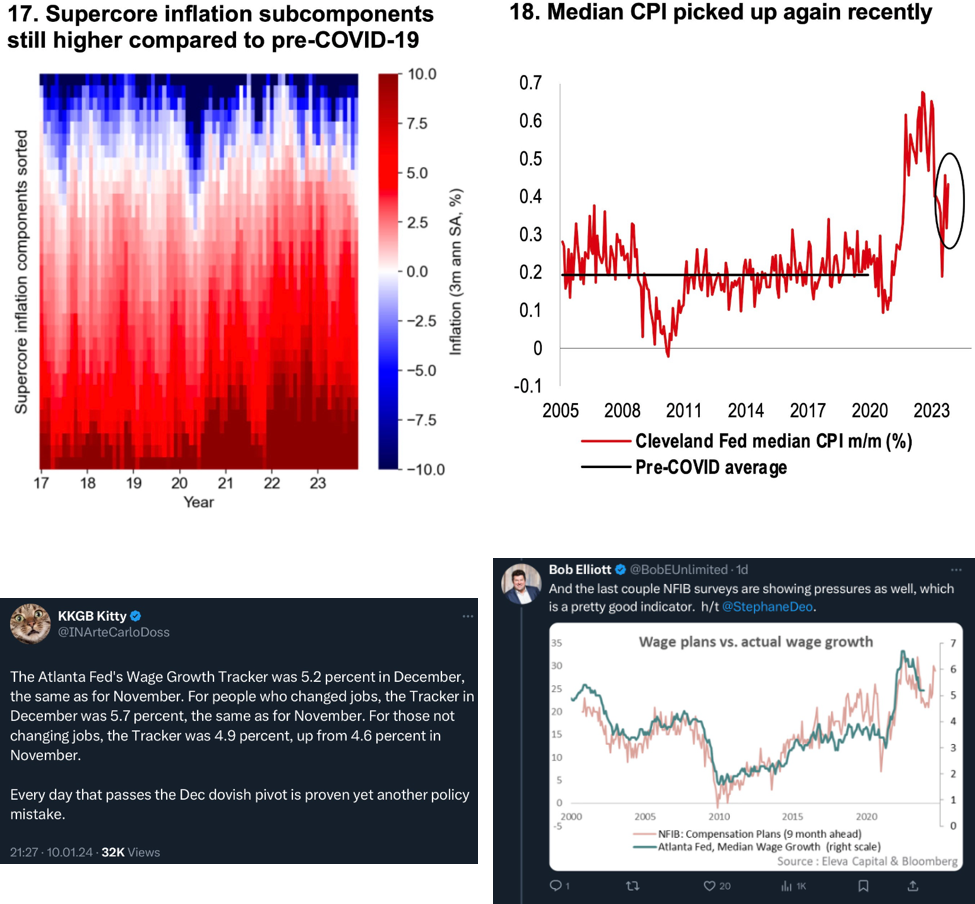

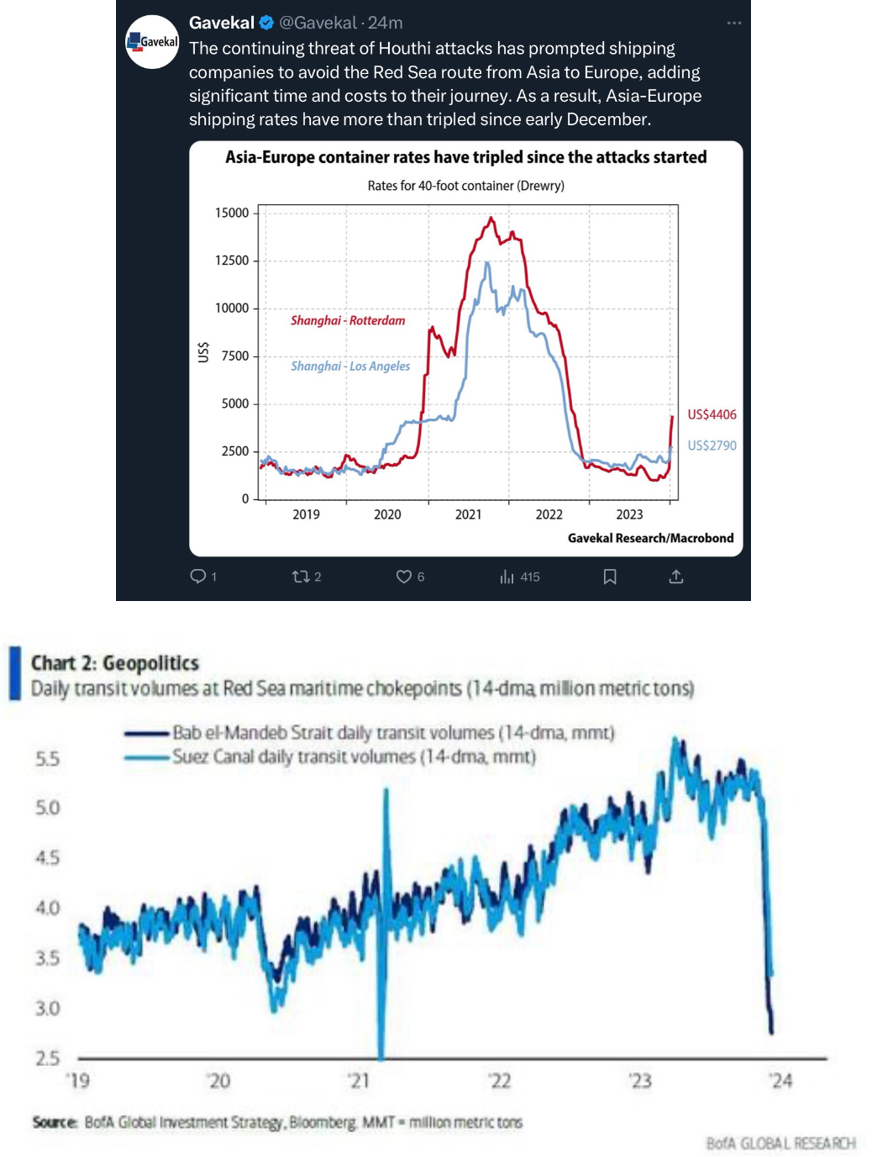

Macro – Macro – Inflation

Our long-term inflation expectation has been clear for some time. It will be much higher than expected as it is the only way out for both the government and those who will hold the key to their election. Asset-rich boomers won’t be able to decide election anymore.

On a shorter-term basis, our scenario was that inflation would be stickier than expected with a potential misleading rebound but that the Fed would remain too restrictive for too long leading to fears of deflation reemerging.

For now, market-based inflation expectations (Inflation Swap Forward 5Y) have risen to more than 2.61% from less than 2.5 at the start of the year.

This could lead the Fed to remain tighter for longer.

This could also lead the Fed to remain tighter for longer...

… but on the other side…

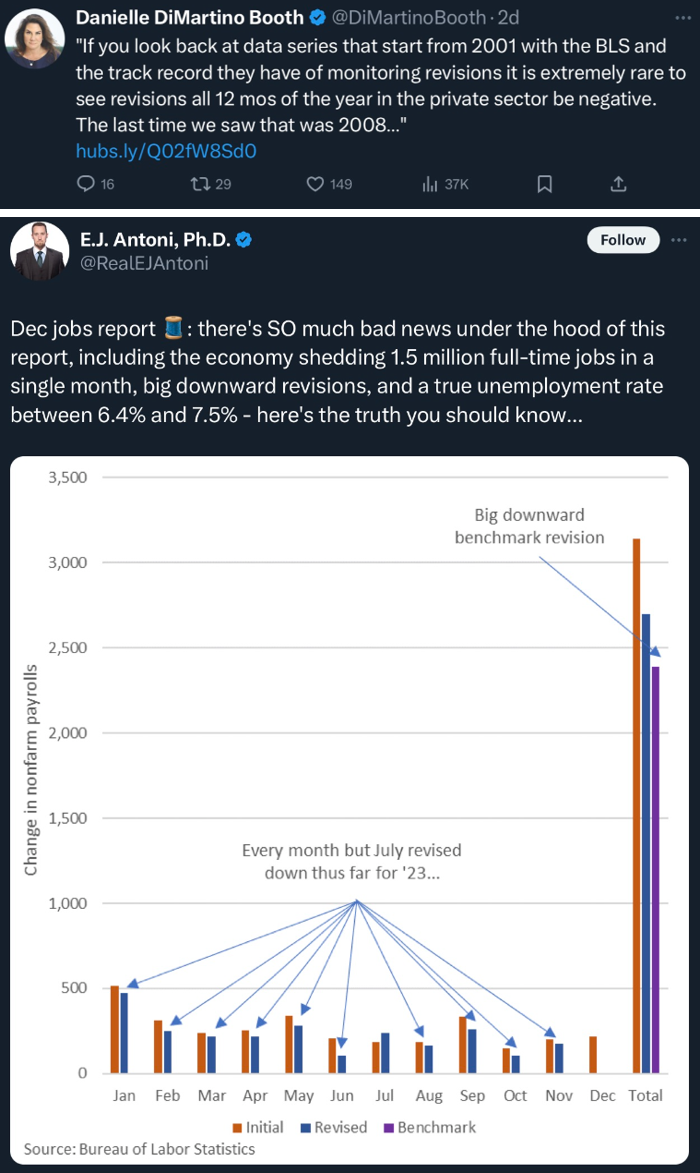

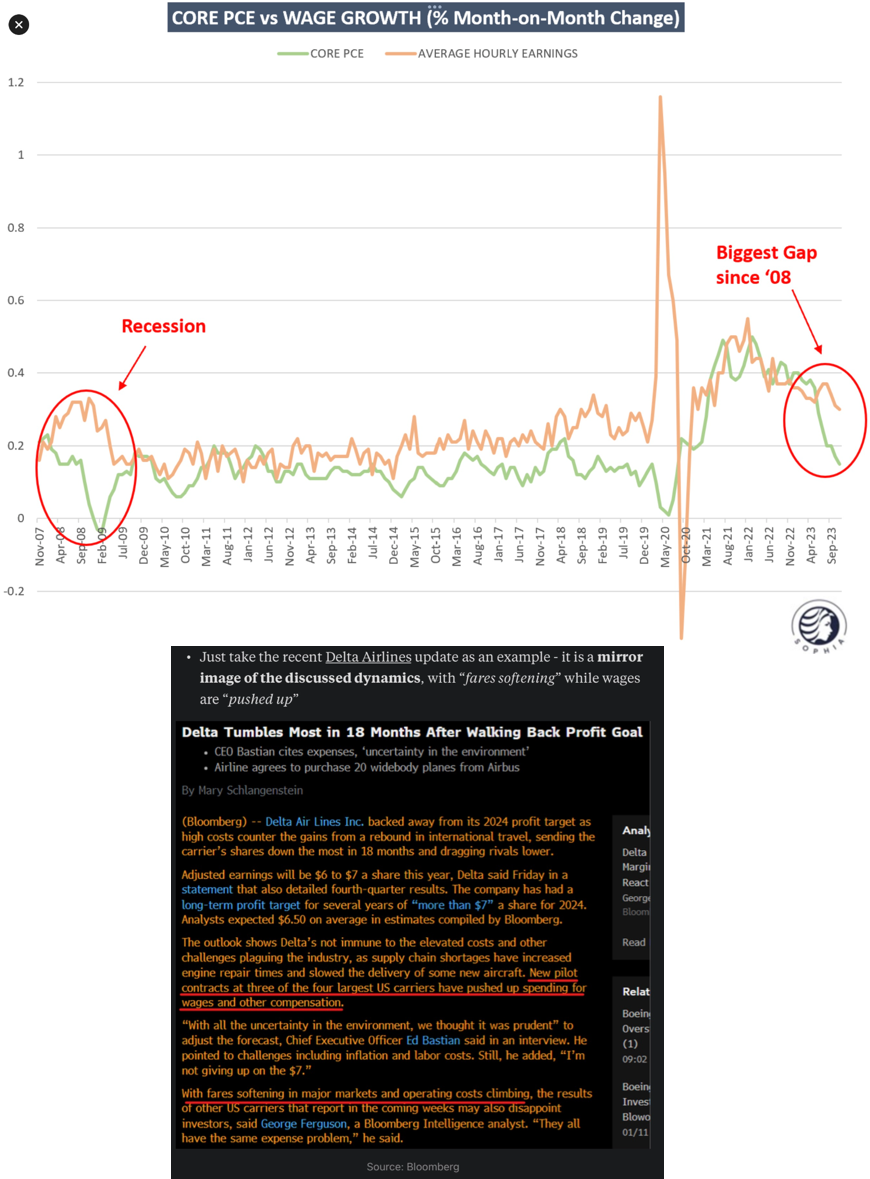

Macro – Macro – Employment

The continued apparent strength of the employment market has been puzzling lately. Even if we take it at face value, one can see that all is not good under the hood...

… and revisions are following the pattern of previous pre/early recession episodes.

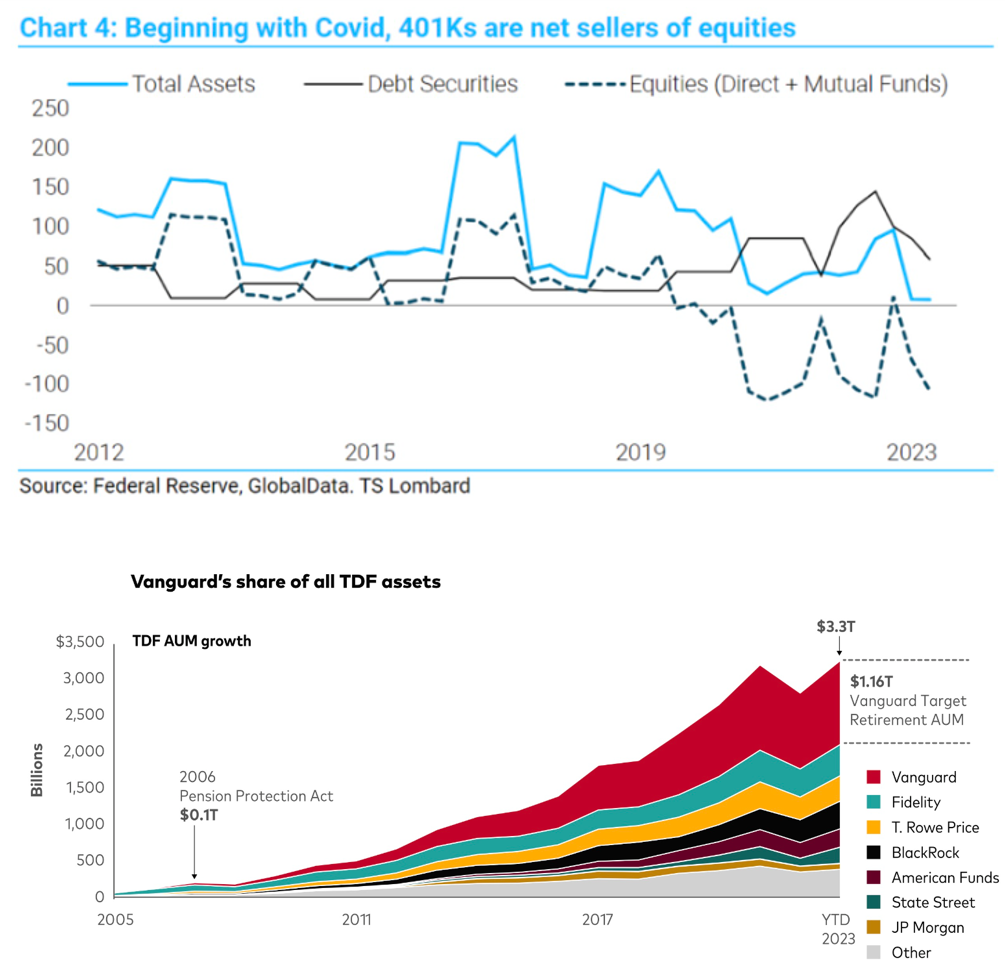

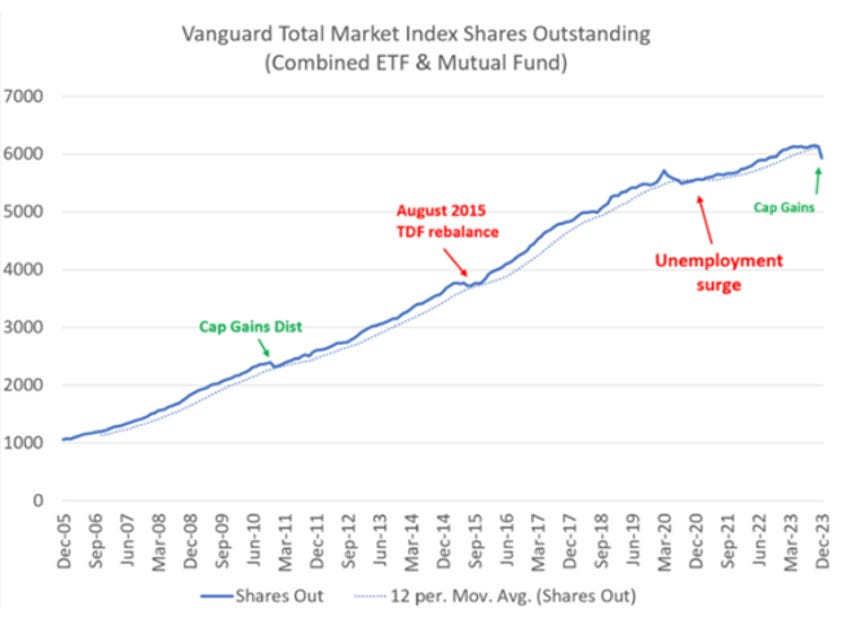

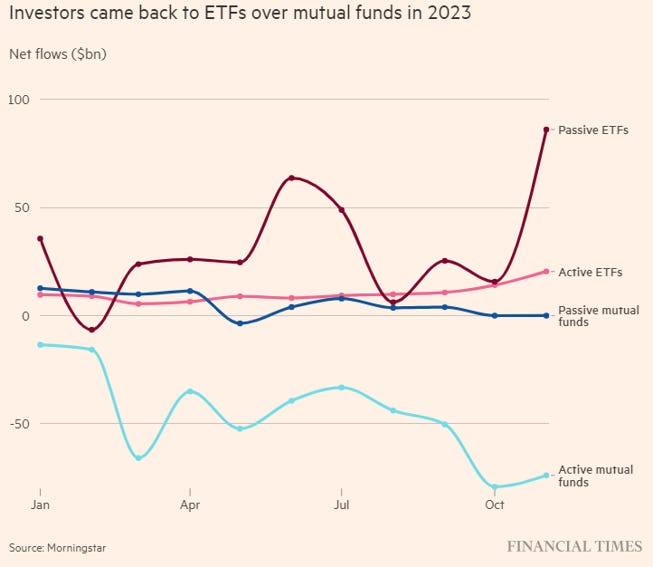

Market – Liquidity

Passive, value agnostic flows to the market have been talked about ad nauseam on those pages. Employment is crucial for the pension passive related flows especially now that boomers are slowly but surely cashing out…

Will those flows be less supportive going forward? We think so (note we said less supportive, not unsupportive!)

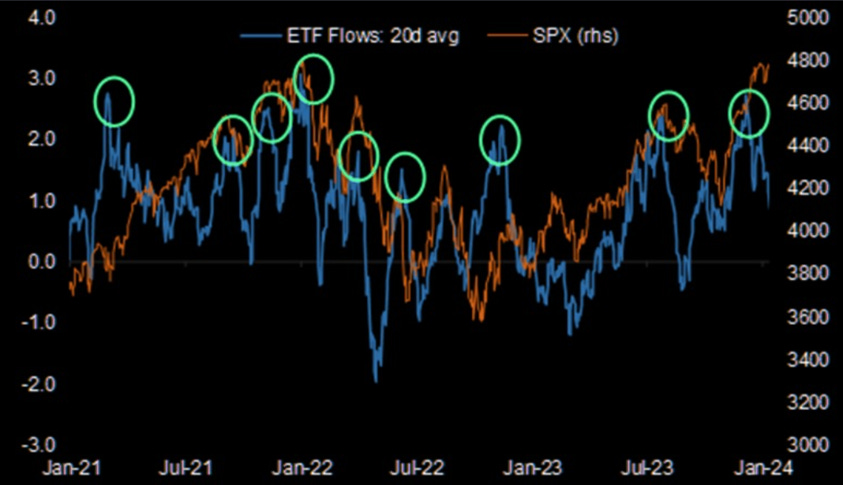

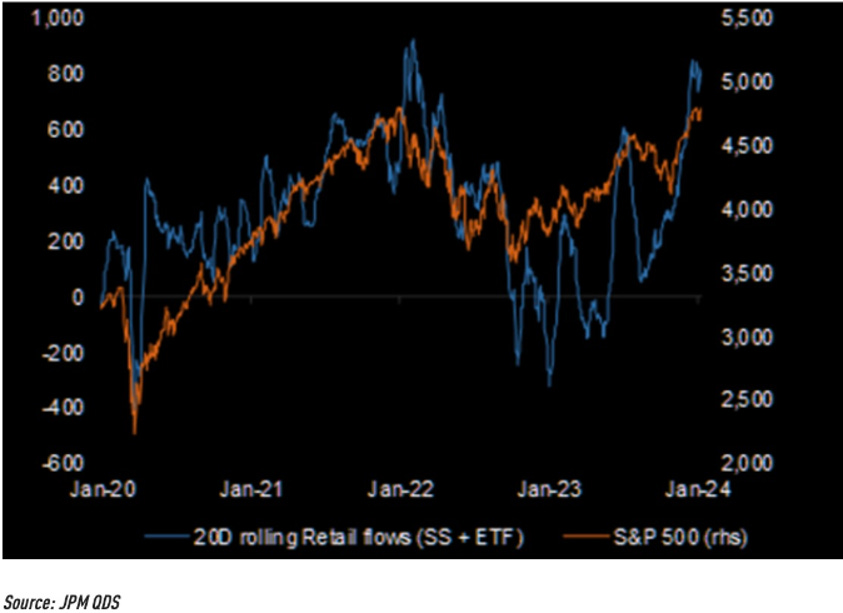

On a short-term basis we see sign of reversing exuberance in nonsystematic passive flows and retail which have been historically followed by corrections

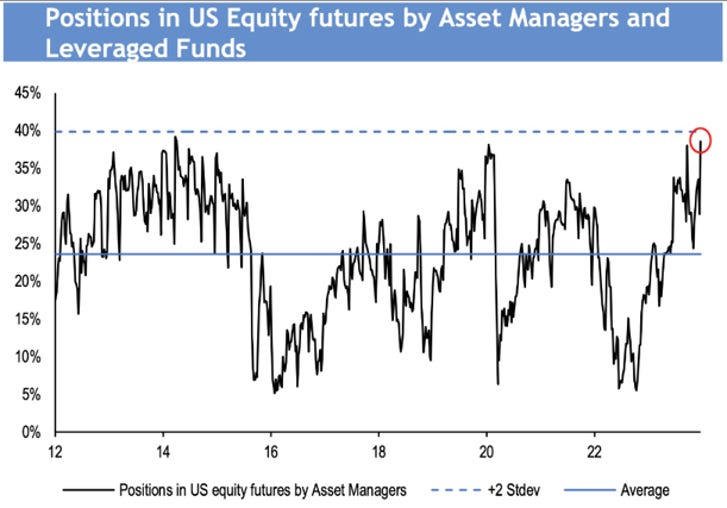

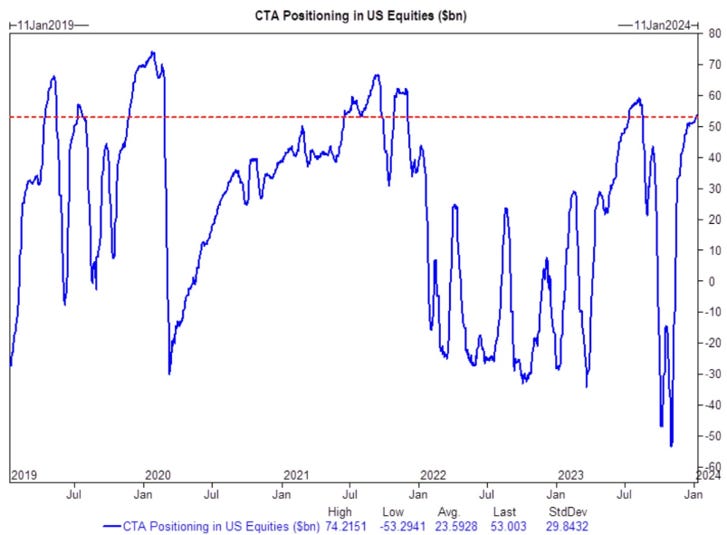

Asset Managers, leveraged funds and other value agnostic systematic funds are also extremely long and are going to be heavy sellers should a correction start and are not going to be heavy buyers before one start to materialize.

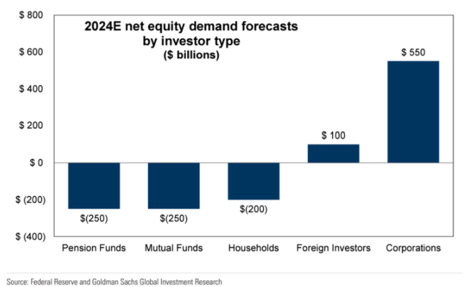

GS expects that corporations (buybacks) will represent, as it has in the past 15 years, most of the net demand for equities. We have explained why we think buybacks might not be as plentiful in the near-future in previous MashUps.

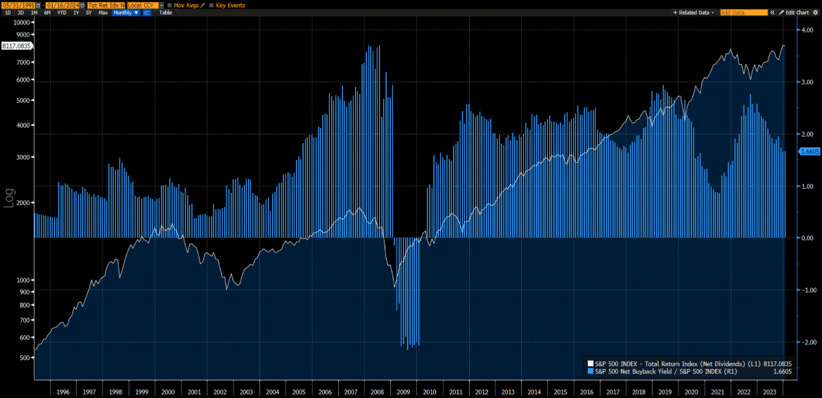

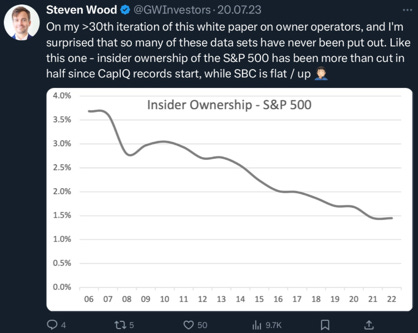

Here is a picture of the S&P 500 net buyback yield and…

… remember the best combination is buybacks and insiders buying and not money transfer from shareholders to managers with little or no skin in the game.

Market – Breadth

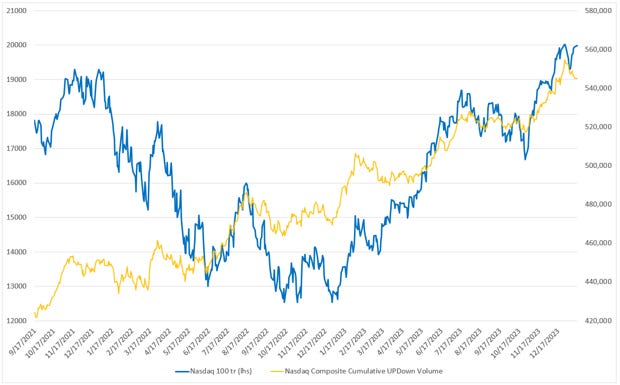

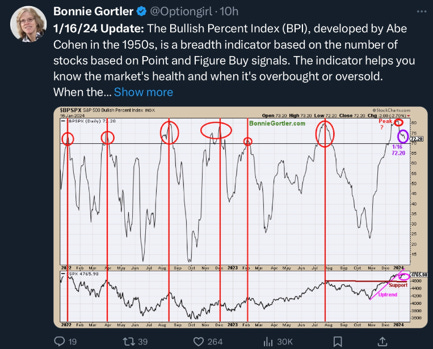

Divergences between the Nasdaq 100 and the Nasdaq Composite up volume-down volume cumulative line is not a positive. Neither is the Bullish % Index moving down from a high level.

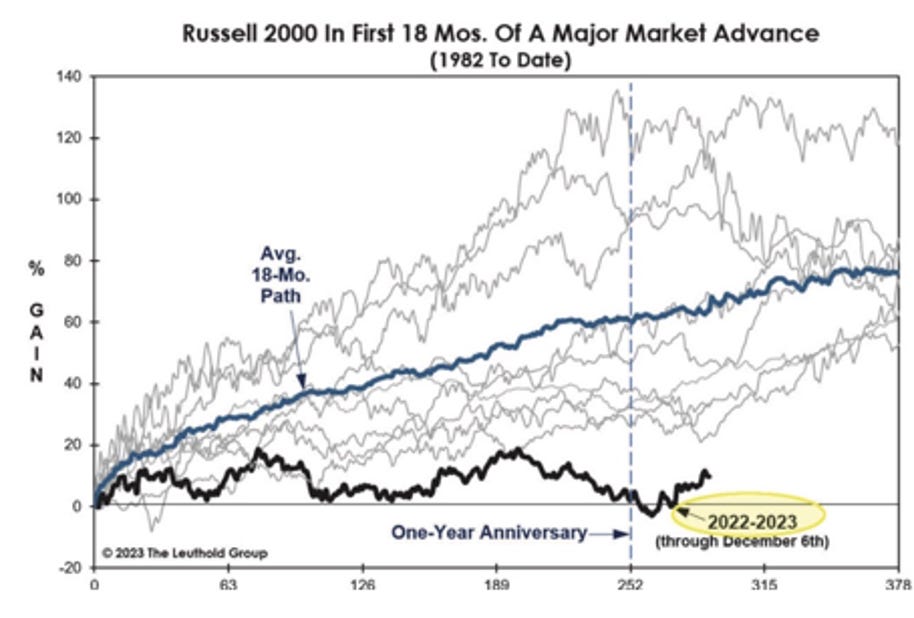

The lack of participation of Small Caps in the rebound is a hallmark of a bear market rally, not a new cyclical bull market

Market – Sentiment

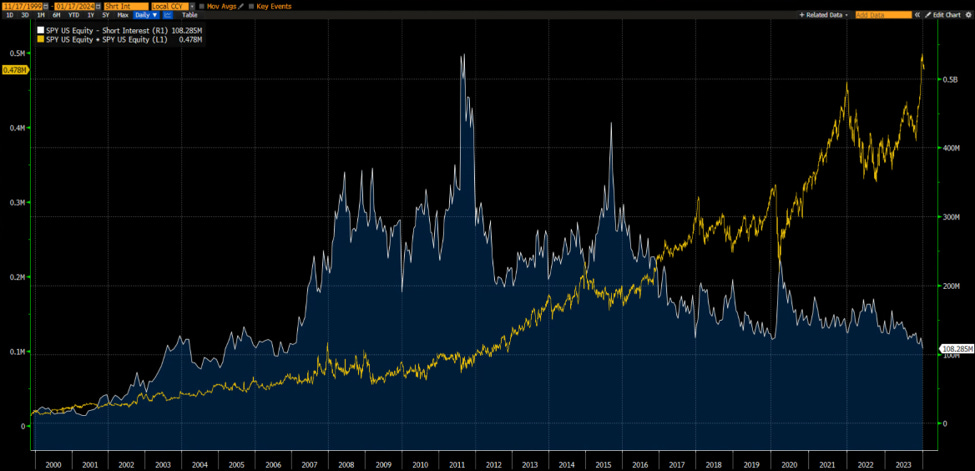

The SPY short interest is continuing to fall while we saw a large surge in AUM. This type of panic buying/short covering is not a good sign.

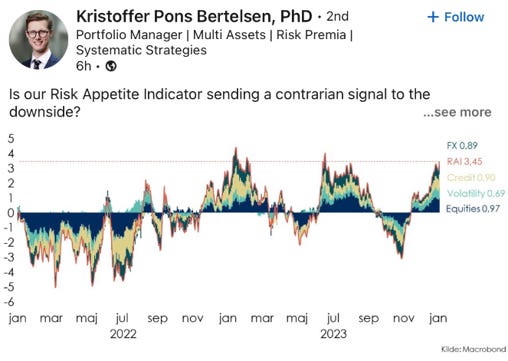

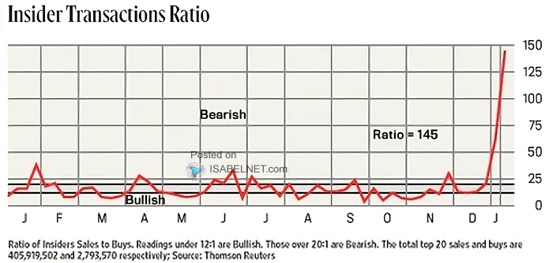

At the same time most risk appetite indicators are reaching their upper bound and insiders are heavily sellers (take it with a pinch of salt as it could be partially explained by tax considerations).

Market – Graph

We like when technical indicators give similar signals using different data granularity (and it aligns with what the rest of our work suggests).

We have a nice setup using T. deMark’s work…

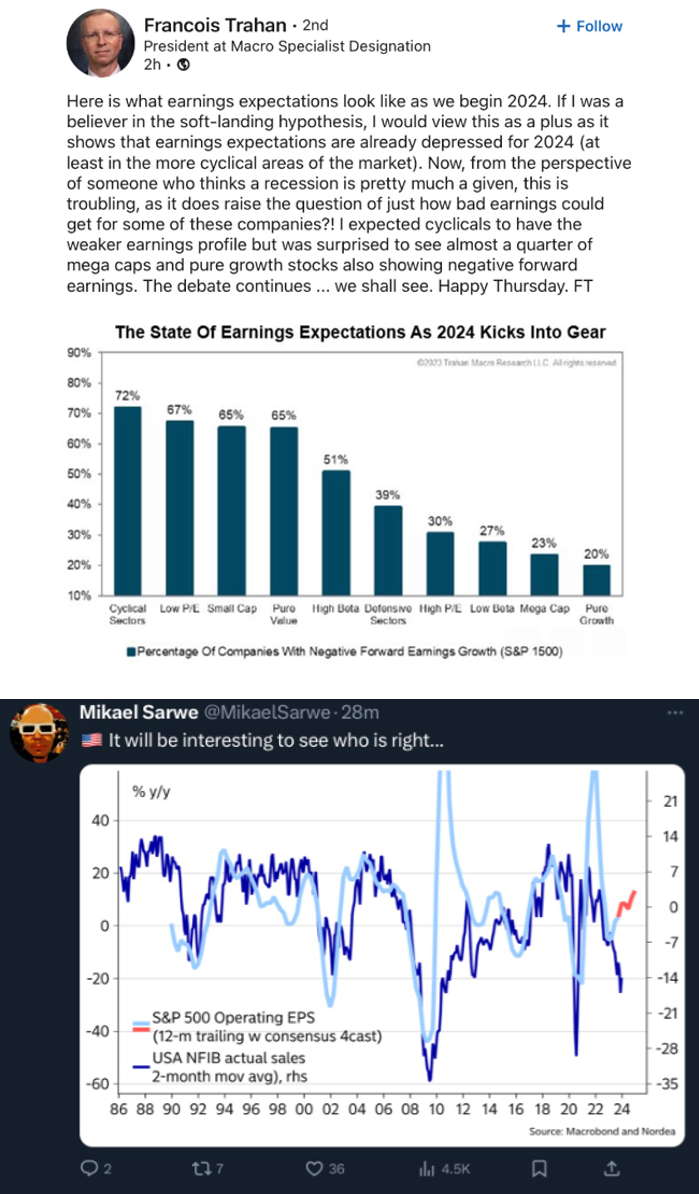

Market – Valuation

Before we move to valuation as such, let’s have a look at the current risks to earnings… We will start with 2 graphs of F. Kronawitter.

Two more observations…

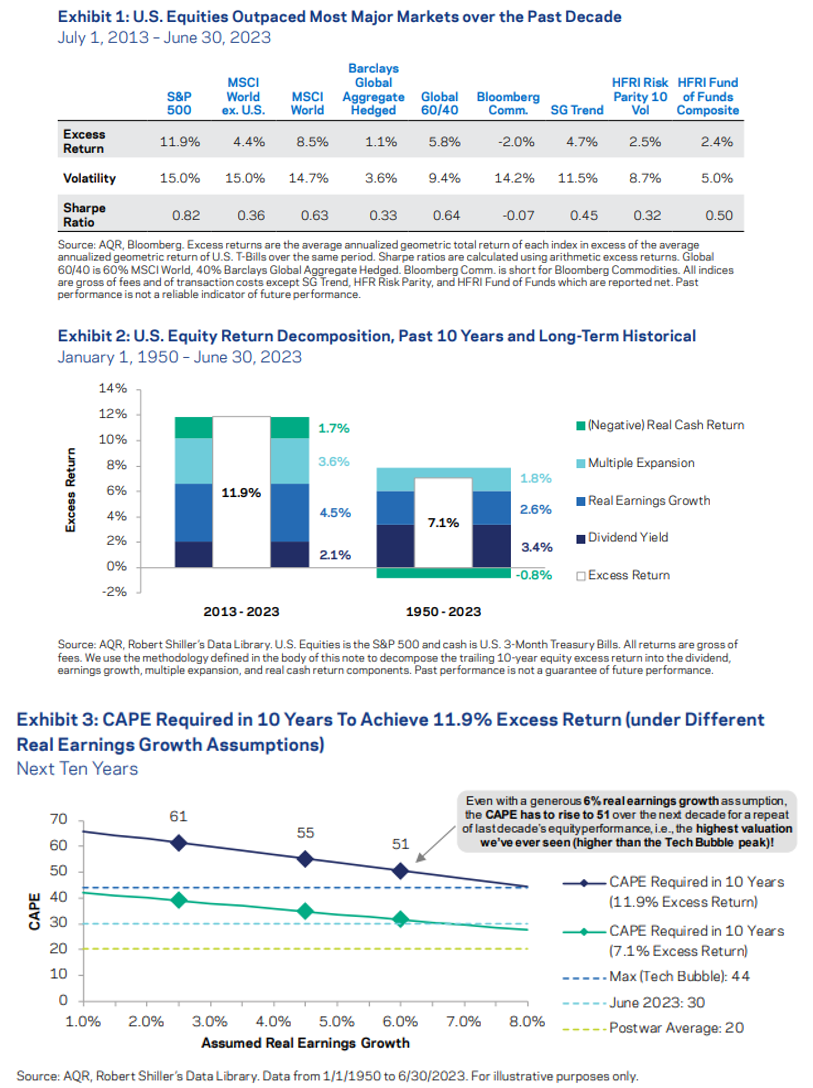

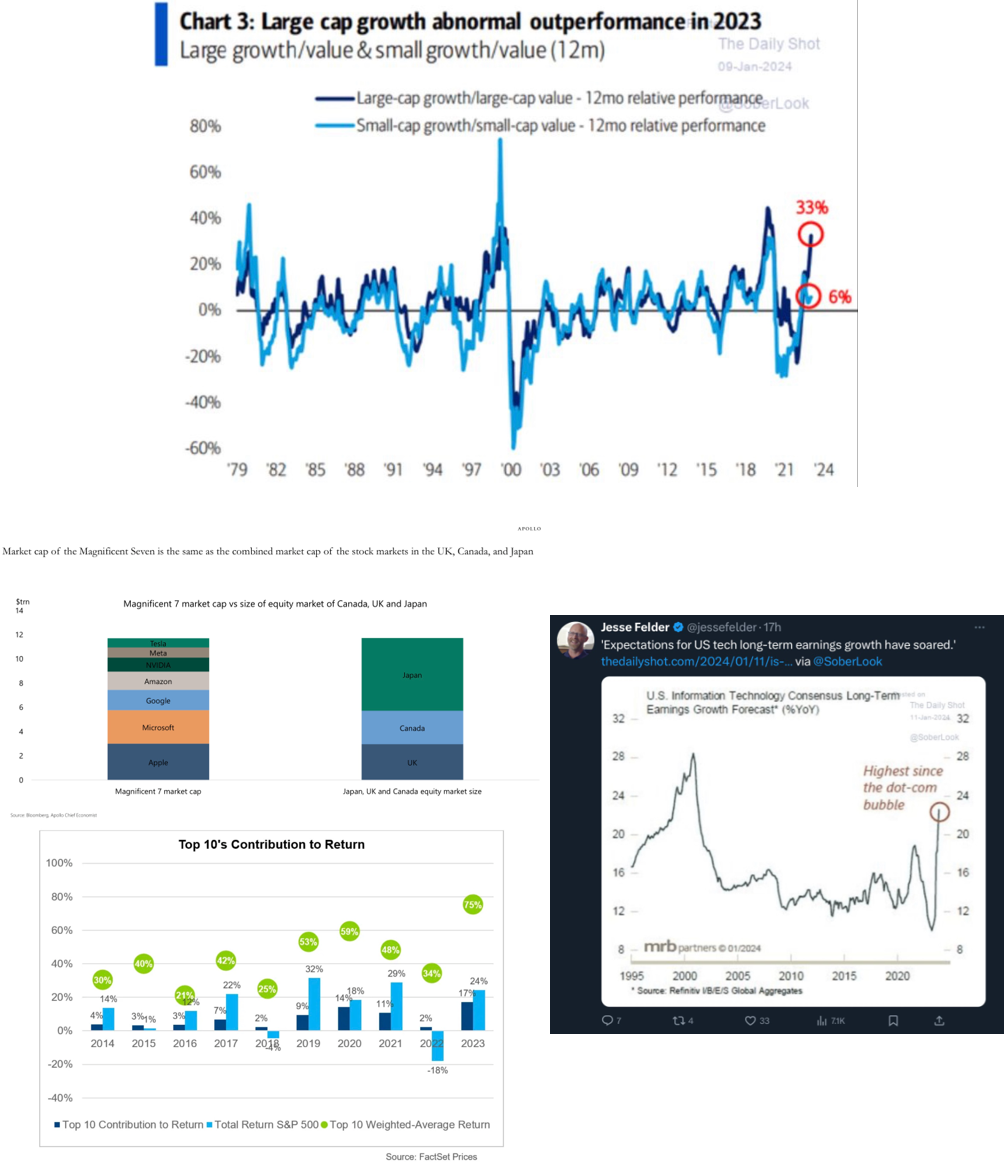

For those hoping for a repeat of the past decade US equity real absolute and relative performance, we have some bad news (a continuation of what was said in previous MashUps but it is so important that we will continue to write about it again and again).

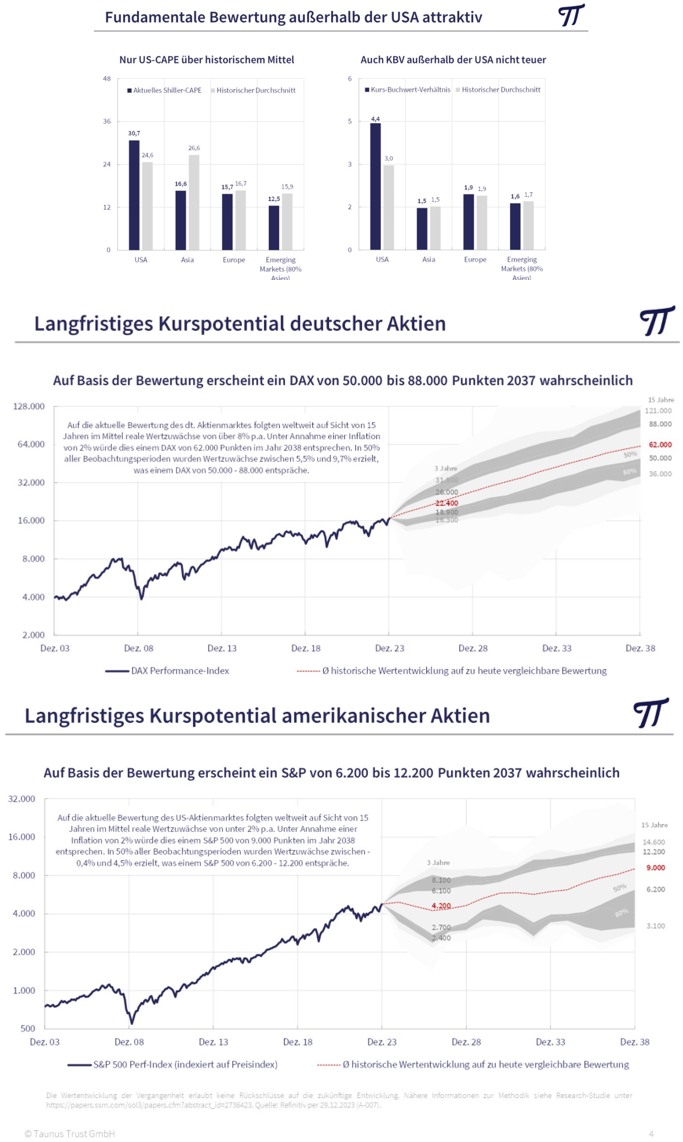

There are more opportunities elsewhere… We have written a lot about Japan (favor Japan domestic oriented companies now to avoid the backlash exporters should experience when the Yen reverses to fair value).

What about Germany?

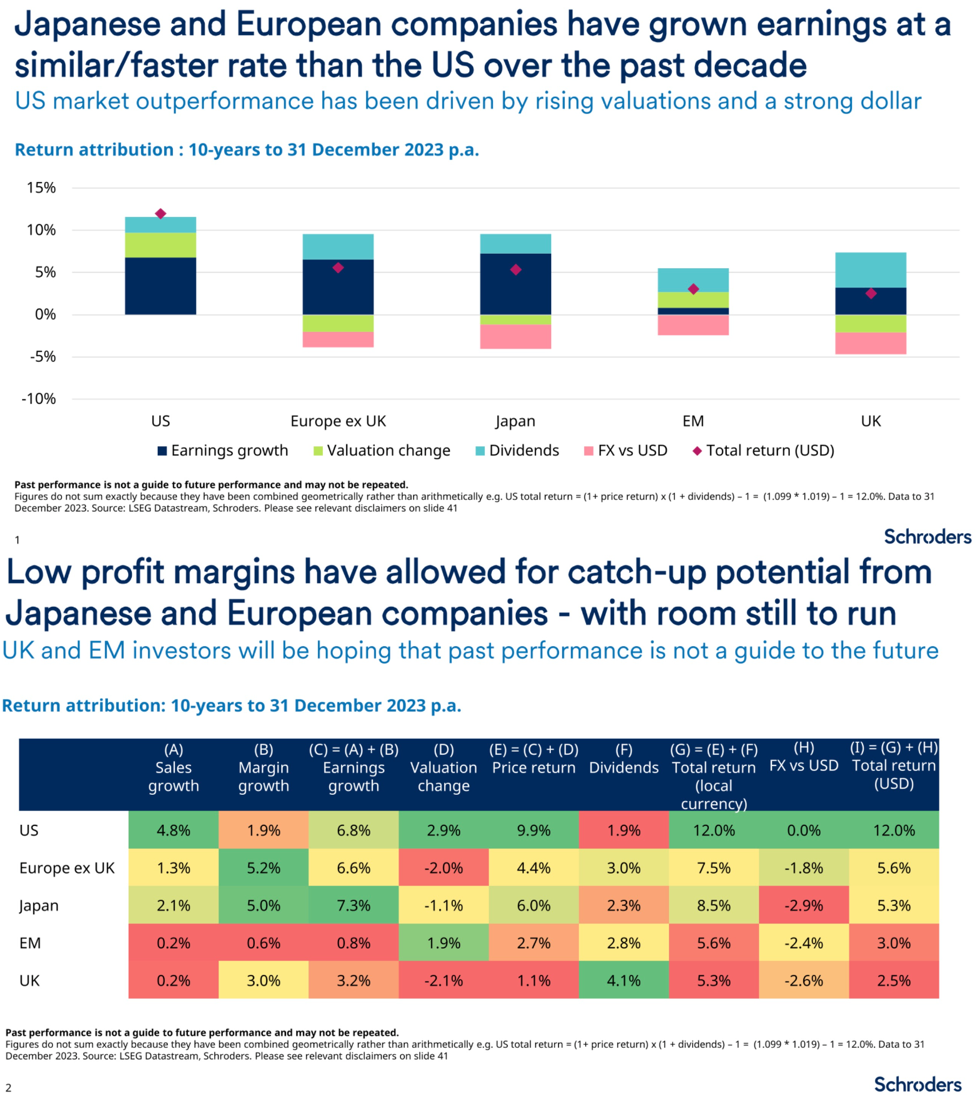

And while sales growth has been slower outside of the US, margin growth has been much higher (and there is still a lot of catch up, catch down or meat in the middle do do). The valuation mean reversion will support markets outside the US on a relative basis.

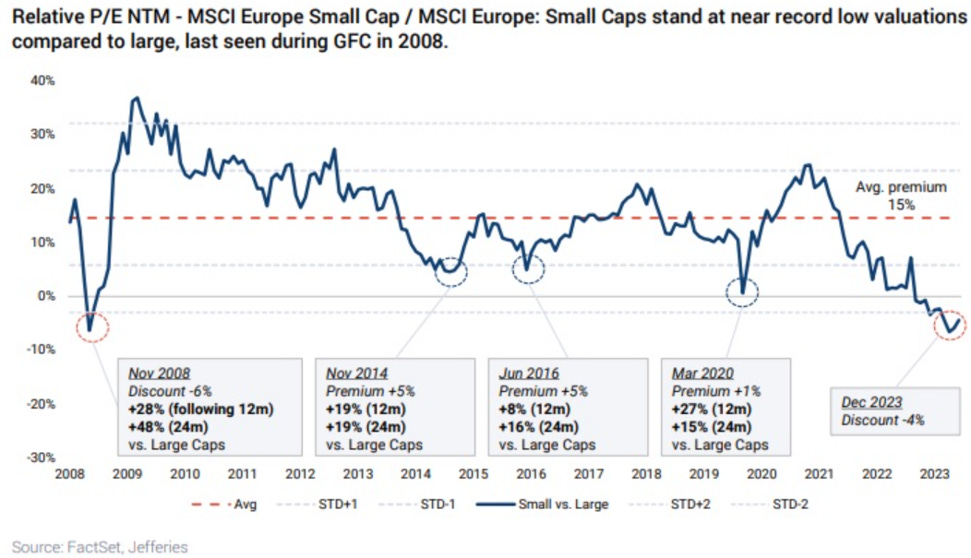

We would favor small cap companies everywhere on a relative basis and outside of the US small caps are likely to generate decent returns in the next 7-10 years but…

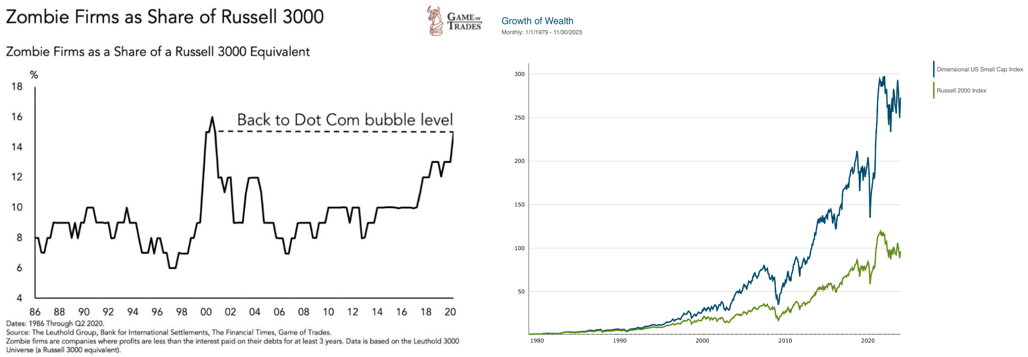

…in small cap land we would avoid loss making companies. There are a lot of Zombies wandering around there. Even when there were not that many, investing in profitable small caps has greatly outperformed the overall small cap indices (that’s why if you should invest in a tracker we much prefer the S&P 600 than the Russell 2000 in the US for example). Dimensional Funds understood it more than 40 years ago…

Once again, do not confuse great companies with great investments…

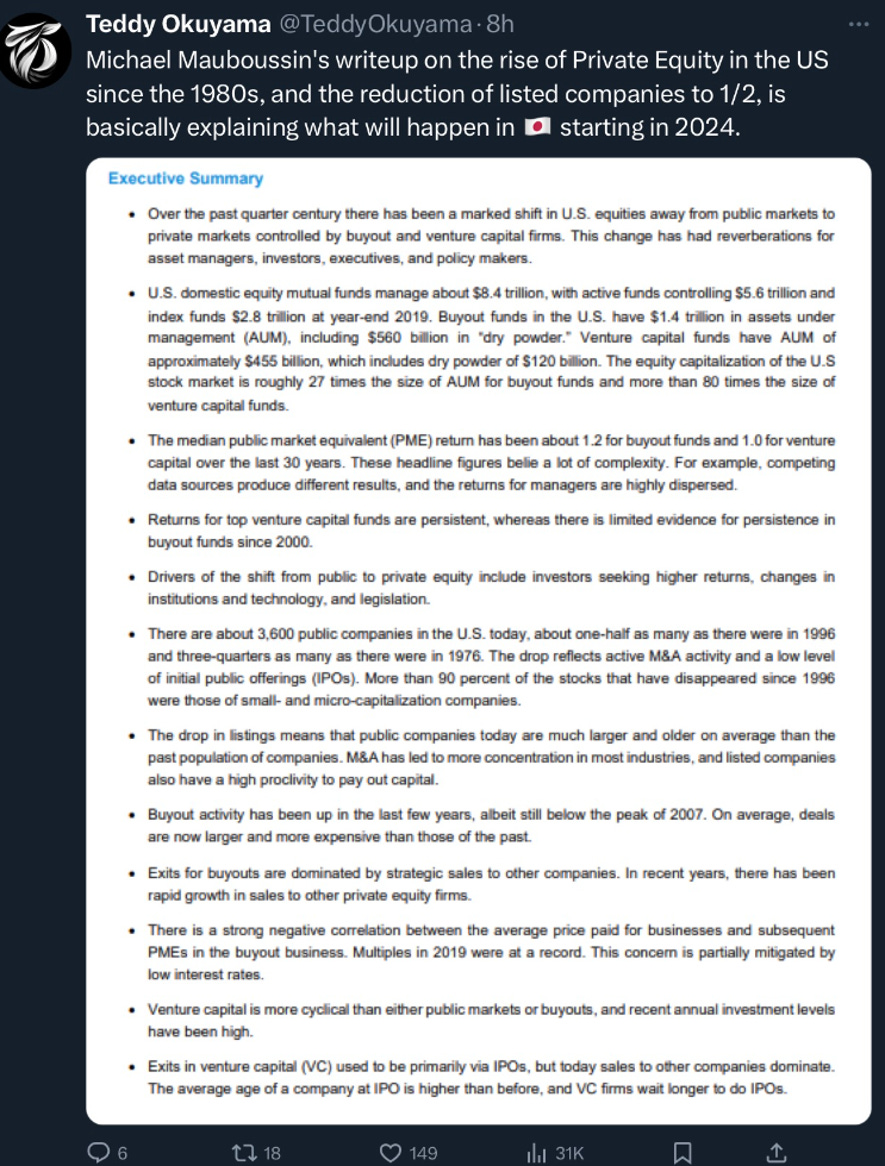

Japan’s future…

Market – Tail Risk

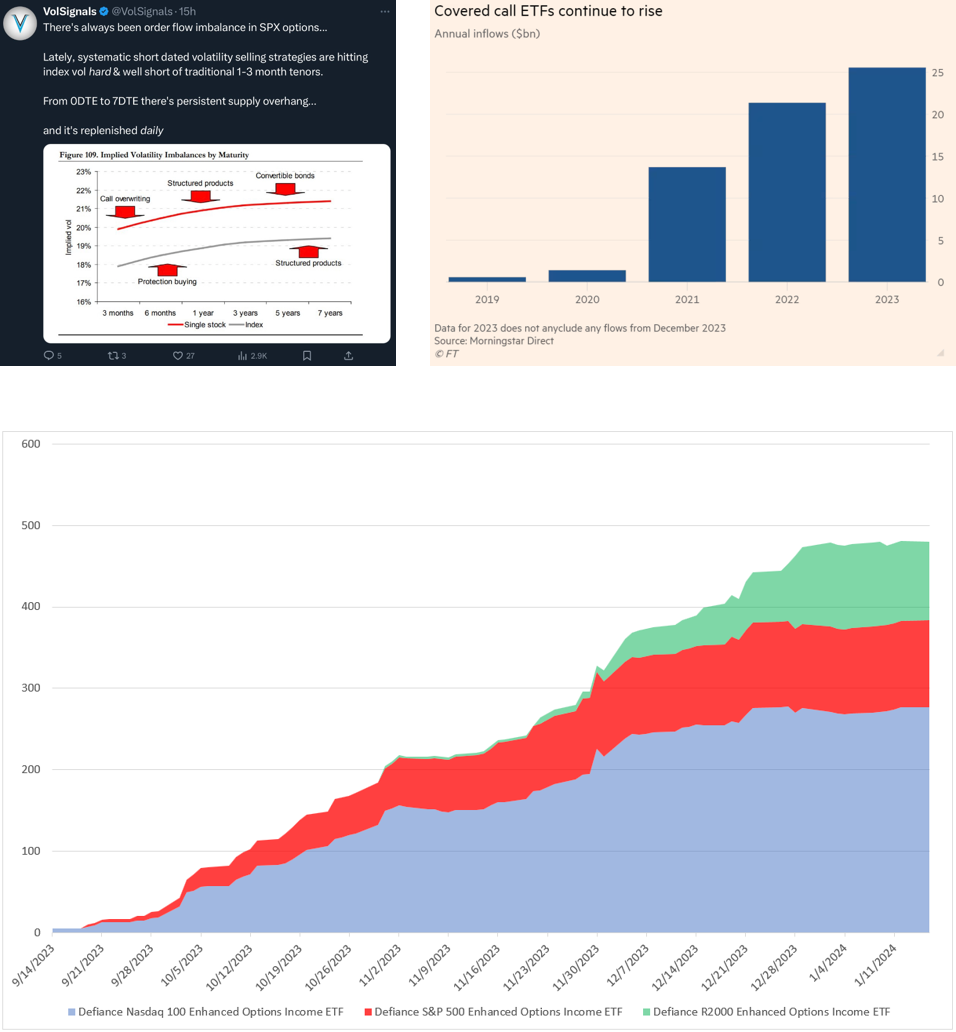

We expect an accident in the volatility space soon.

Now there are huge inflows into strategy selling both upside and downside volatility.

We also see rapidly rising in option volume at the expense of stock volume. Interactive Brokers just published some numbers confirming it. Investors (can we call them like this) are searching for lottery tickets!

As implied volatility is decreasing rapidly, investors need to increase their leverage when selling options to get the same income. If this is not an accident waiting to happen, we do not know what it is…

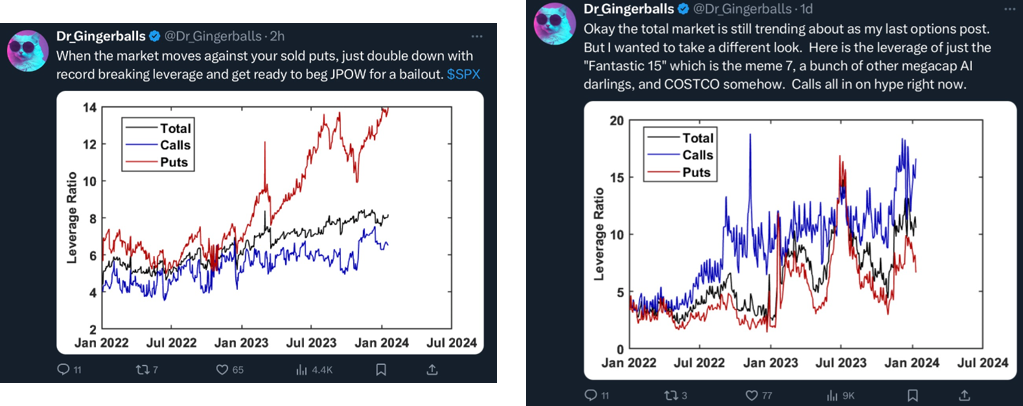

One can also see that investors are using lots of leverage on calls on the “Fantastic 15” while, when looking at all stocks and ETFs, they are using much more leverage in puts. Our guess is that the markets is financing upside volatility in the “Fantastic 15” by selling downside volatility everywhere…

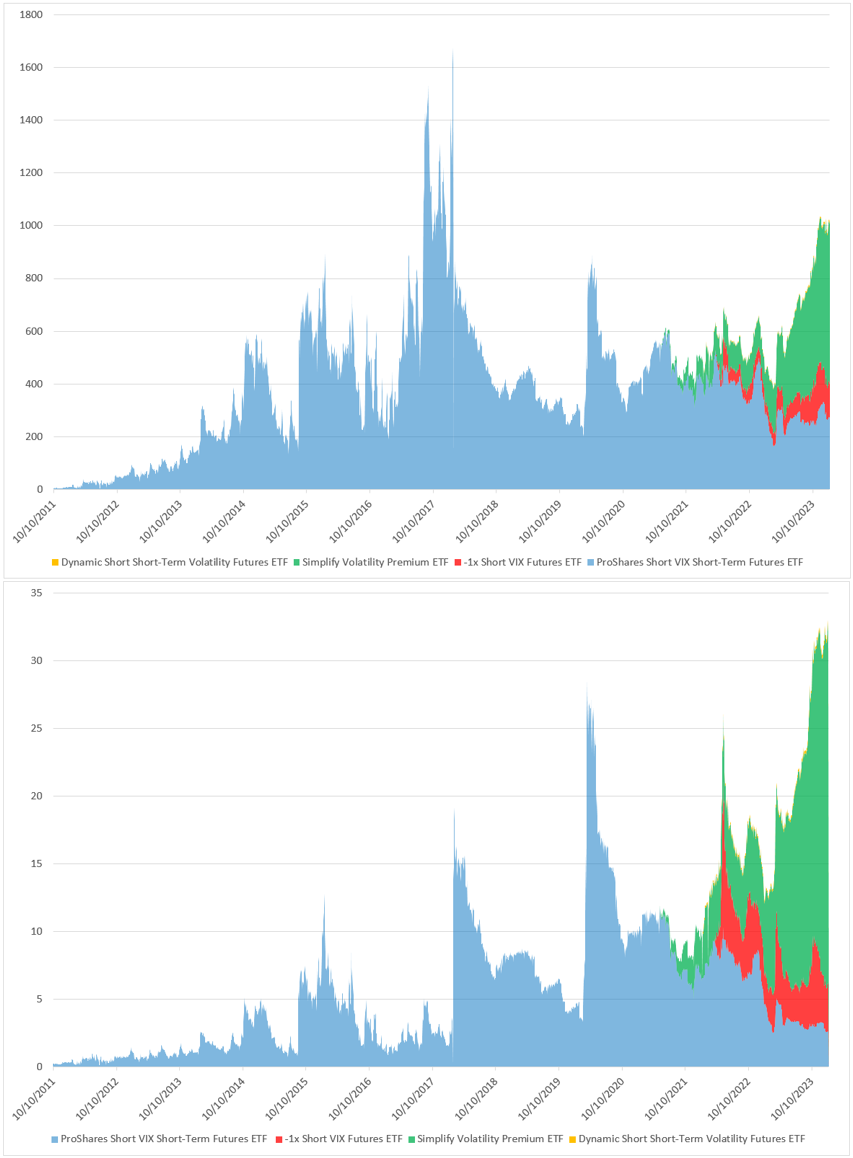

The AUM in short volatility ETFs has increased rapidly recently and it is not just a function or rising price. The second graph is a crude way to look at non-price related flows and one can clearly see the recent gain in popularity (previous spikes occurred after vol shocks).

Market – Fixed Income

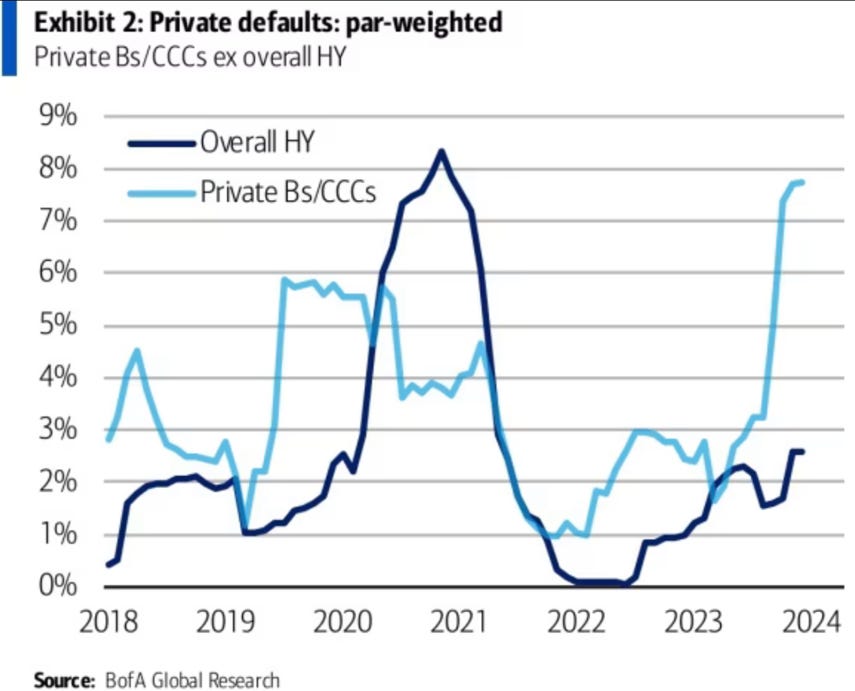

The boom in private credit probably dampened the number of public bonds defaults but the longer the Fed maintains its restrictive policy, the less defaults will occur beyond public scrutiny with all the psychological effect it might have.

Let’s also see how private credit fare during their first real default cycle…

Others

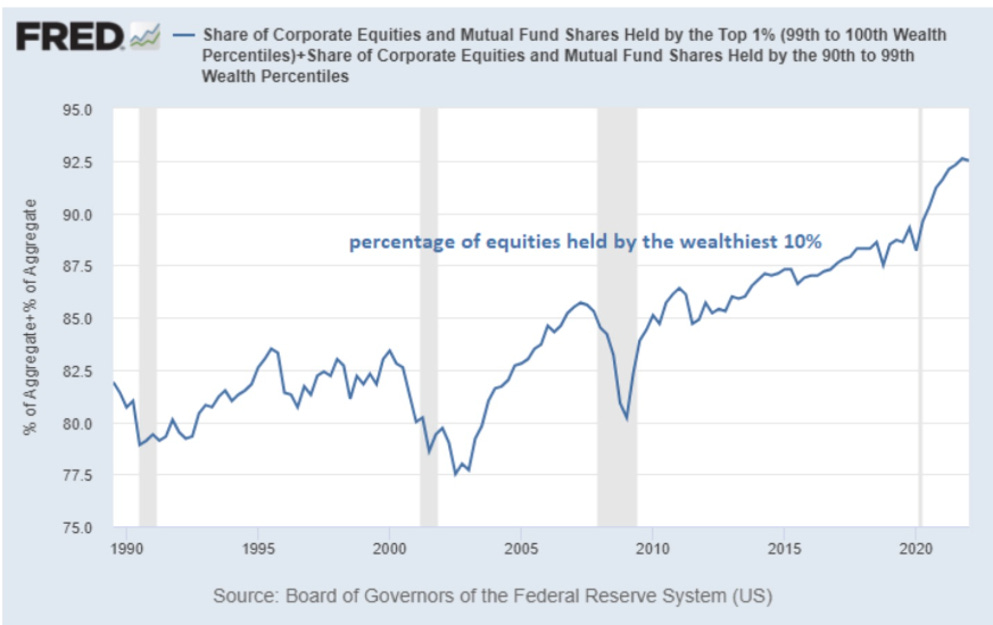

One should stop wondering why western societies in general and the US in particular are getting more polarized. If you add declining real purchasing power, borrowing costs rising much more for those who need the most (not to make money but to survive) and crumbling social fabrics, the opportunity cost to revolt against the system has not been this low in modern history.

Think again about the buyback and insiders' shareholding graphs showed earlier…