August 28, 2023

Summary

- Lags

- Households not impacted homogeneously

- Inflation, battle won?

- Central Banks and lack of humility

- China, again

- Markets –Liquidity, breadth, sentiment and valuations

Macro –Lags

Sometimes a picture is worth a thousand words. Why overcomplicate with fancy explanations…

Thanks @MichaelAArouet for the following 2 gems - second one from Herb Greenberg but twitted by @MichaelAArouet

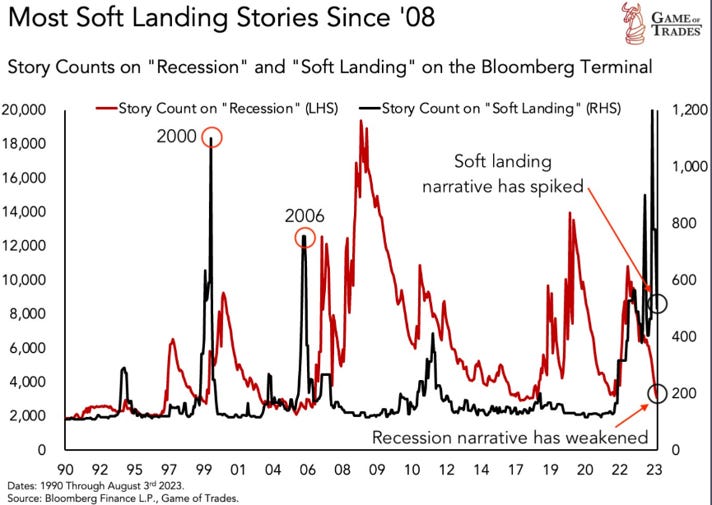

Game of Trades expanded the ‘Recession’ vs ‘Soft Landing’ story counts back to 1990. As the press clips we have shown in the past, one can see that the ‘Soft Landing’ narrative becomes dominant just before the ‘Recession’ starts…

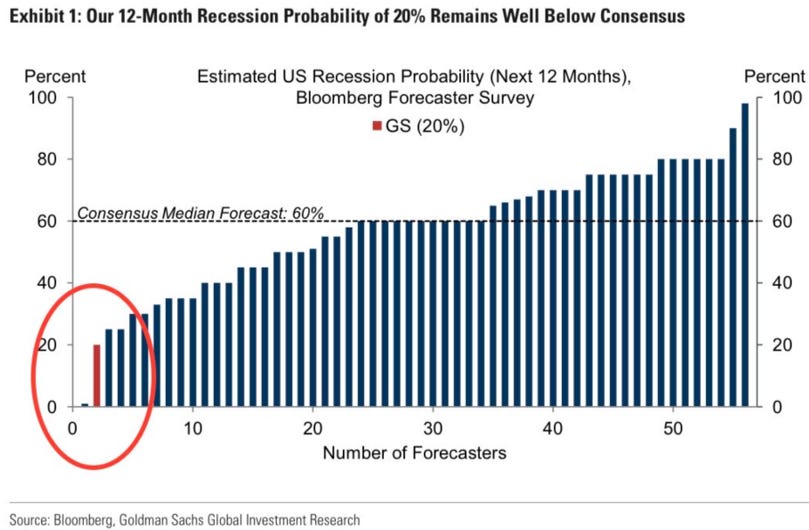

Goldman is giving up on the recession while…

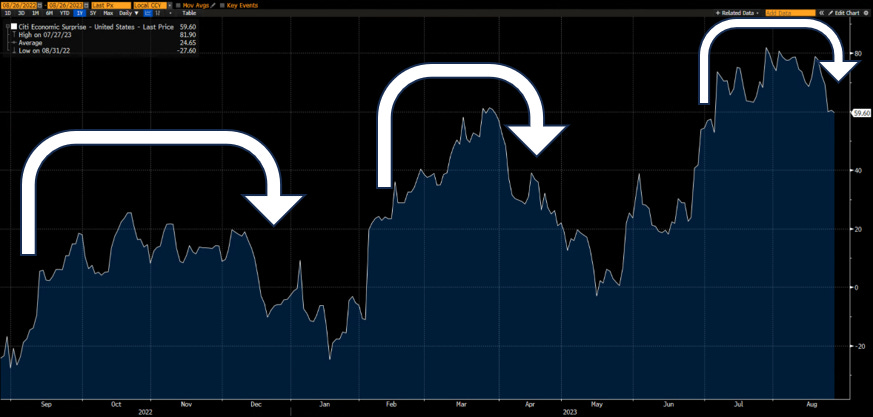

…the Citigroup US Economic Surprise Index is turning downwards. It did 2 times in the past 12 months but the main difference now is that revisions to past macro numbers are negative.

Macro –Households

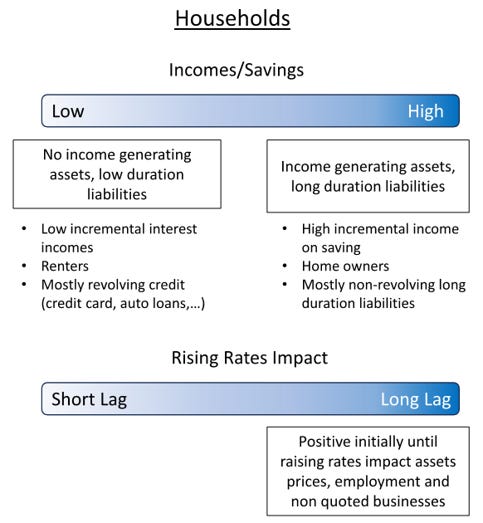

We have spent numerous pages in past MashUps on varying lags of increasing rates on households and corporations. Here is an attempt at a schematic illustration (suggestion for improvement welcomed!).

Now that the Covid excess savings are mostly gone (completely gone for the below median income earners) and that the social security inflation adjustment bonuses are spent the cycle will start to unfold as it has historically.

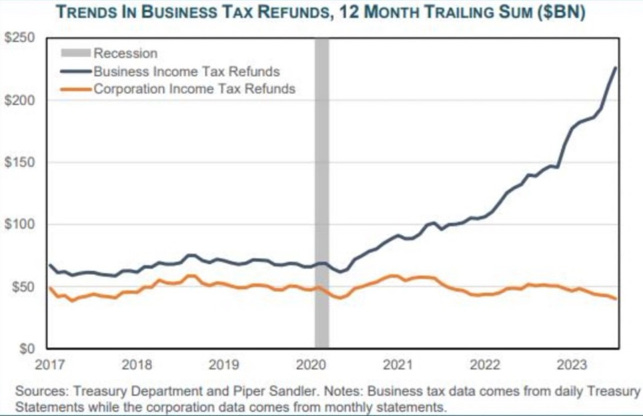

Business owners, courtesy of the Employment Retention Credit, are still getting money to spend but it seems that the IRS and Congress are (finally) looking into that…

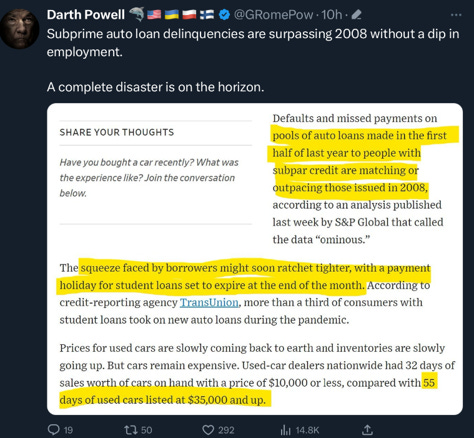

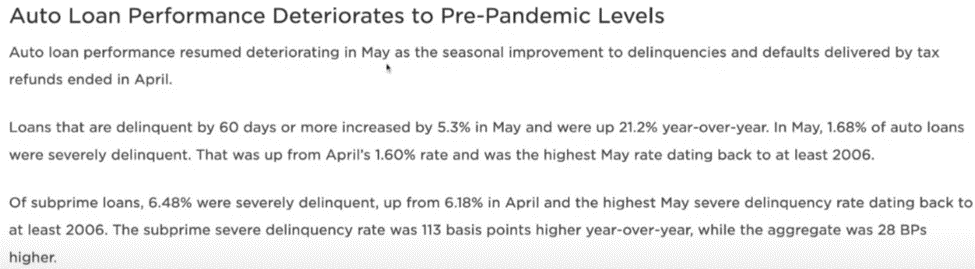

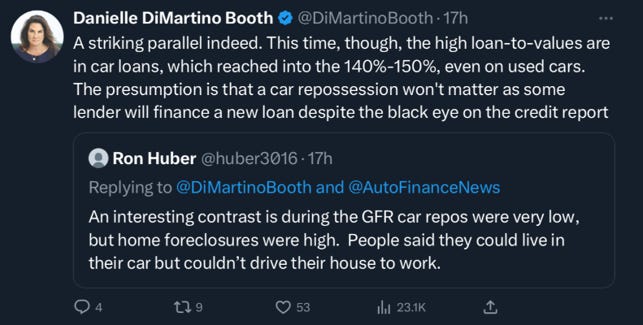

Auto Loans… not good…

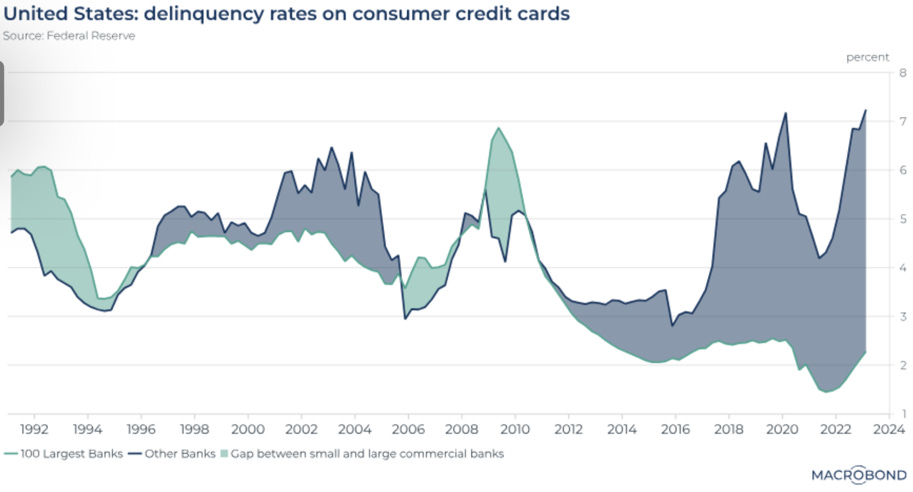

Credit Cards, not so good either…

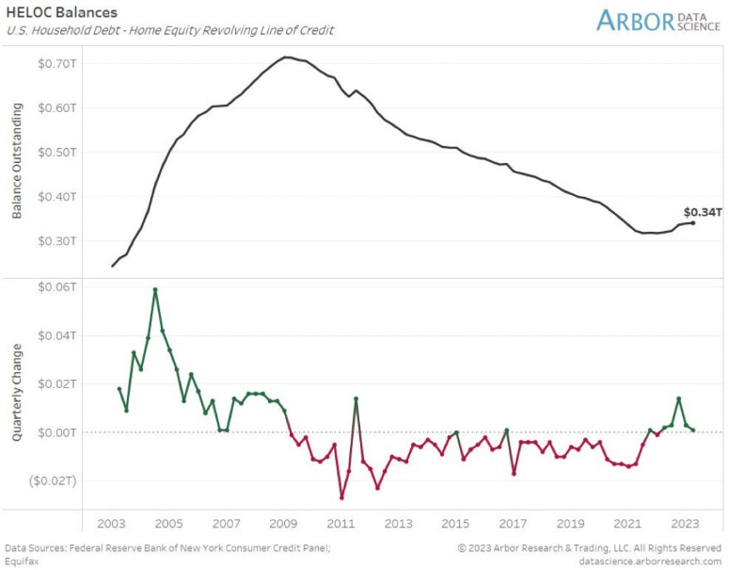

Home equity was tapped early but now it is too expensive…

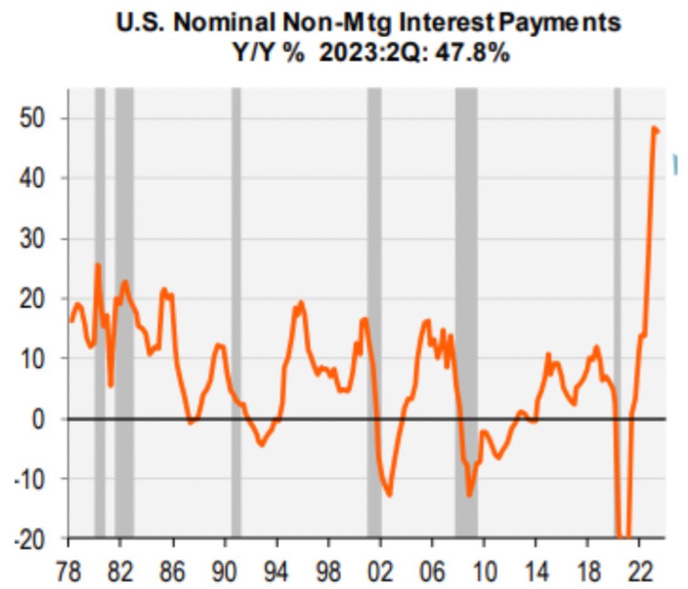

Non-mortgage interest payments are going through the roof…

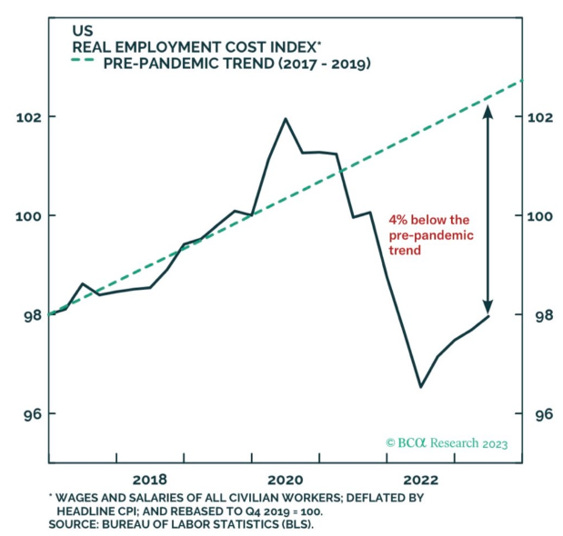

… fortunately real wages are compensating… or not?

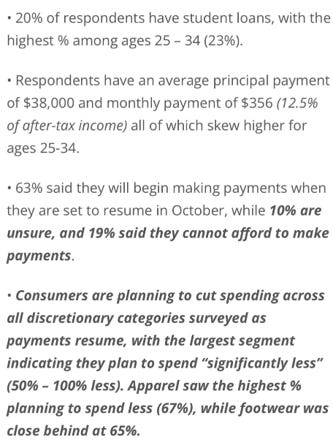

Let’s not forget the end of the student loan payment suspension.

Macro – Inflation

Some really smart analysts are expecting a resurgence of inflation. There could definitely be some surprises into November-December but our main scenario remains that before a longer-term resurgence of inflation, we might have a deflation scare sometimes next year.

One should still keep an eye on what is happening with wage negotiation now that the US are striking as it is usual in some European countries…

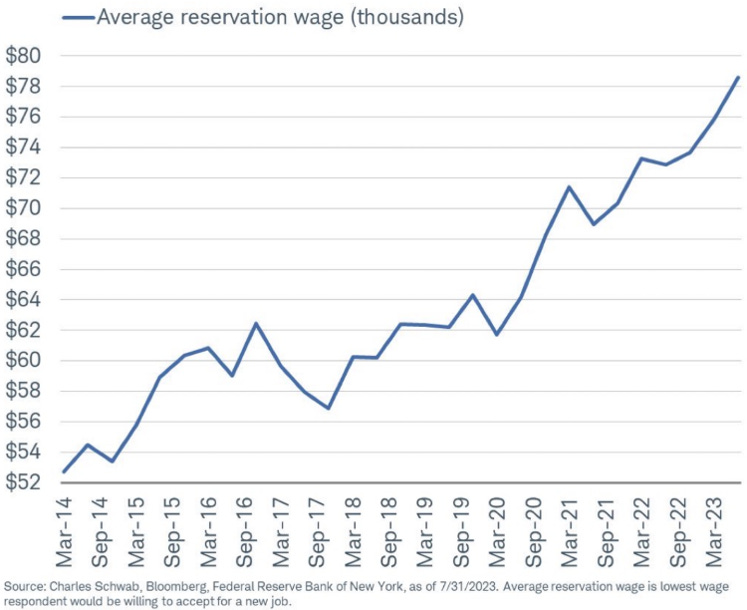

And that the average reservation wage is going to the moon!

Macro – Central Banks

Some commentators were expecting discussions about the level of inflation the Fed should target in Jackson Hole. There won’t be. They will have to change it one day given the endemic level of leverage but doing it now, would be an error. They will use the next recession as an excuse.

On this subject and going along with our longer-term inflation forecast we recommend to read C. Calomiris paper (well it is more than a recommendation, read it!).

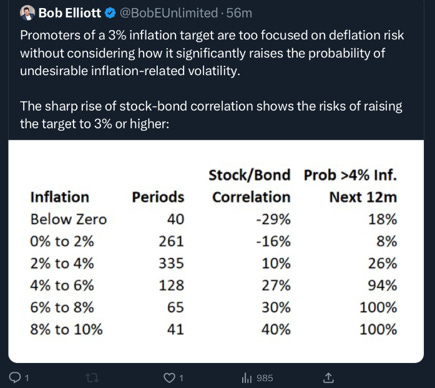

When the inflation path is finally chosen, remember this from @BobEUnlimited. Look at the Stock/Bond correlation column too… 60/40 portfolios won’t work as they used too.

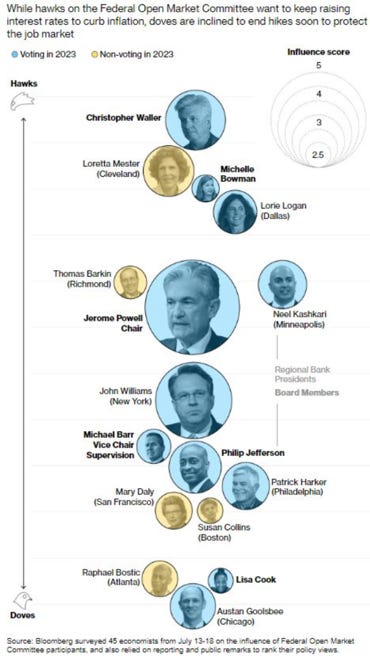

So what will the Fed do in the meantime? In the graph below you have this and next year voters on a «dove-hawk»-ometer

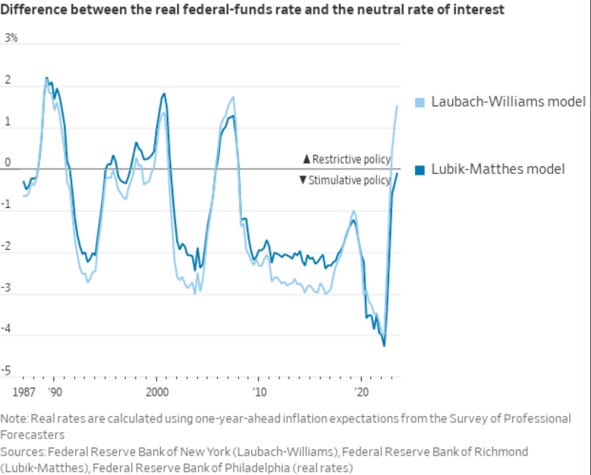

One thing for sure most members of the Fed will continue to base their policies on unobservable measures for which they will build new models (or adapt old ones) to fit the narrative.

Two examples from a recent article of @NickTimiraos.

What is the longer-run fed funds rate? It seems to be moving as much as the short-term one.

What is the difference of the real federal-funds rate and the neutral rate of interest?

It is time for economists to realize that economy is a social science and that it is ALWAYS better to be appoximately right than precisely wrong. We use to joke that forecasting most macro variable 3 months in the future and using a number with a decimal point, one either has a very good sense of humor or is grossly overconfident.

Being a non-economist by education, J. Powell is refreshing on this point.

Macro – Budget Deficit

Before we move on to China, let’s see if you can guess why this happened (hint: November 5, 2024)

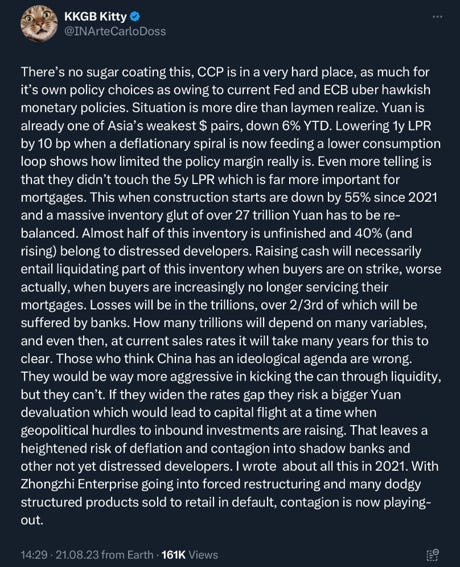

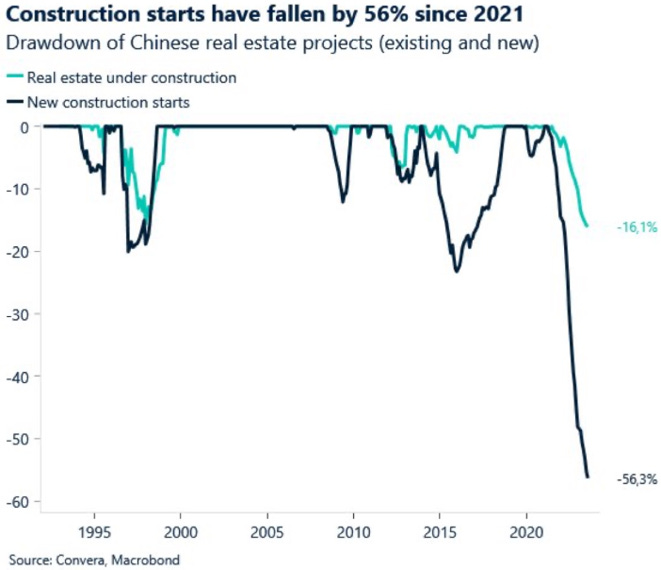

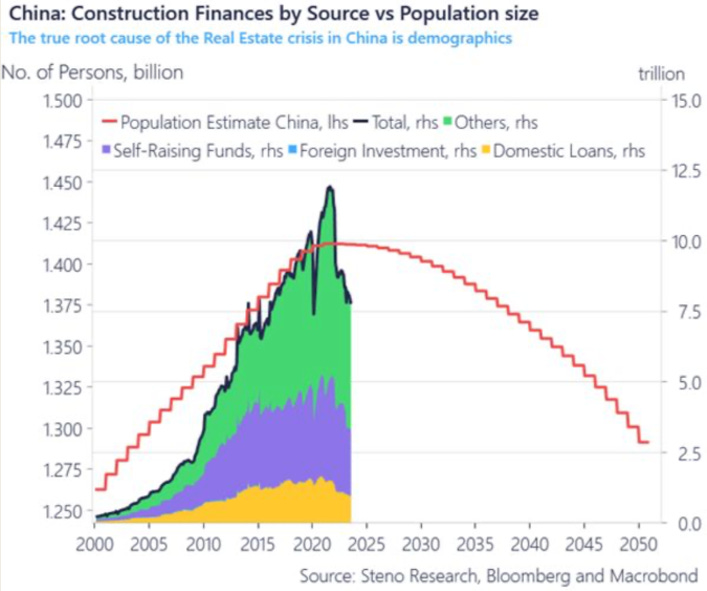

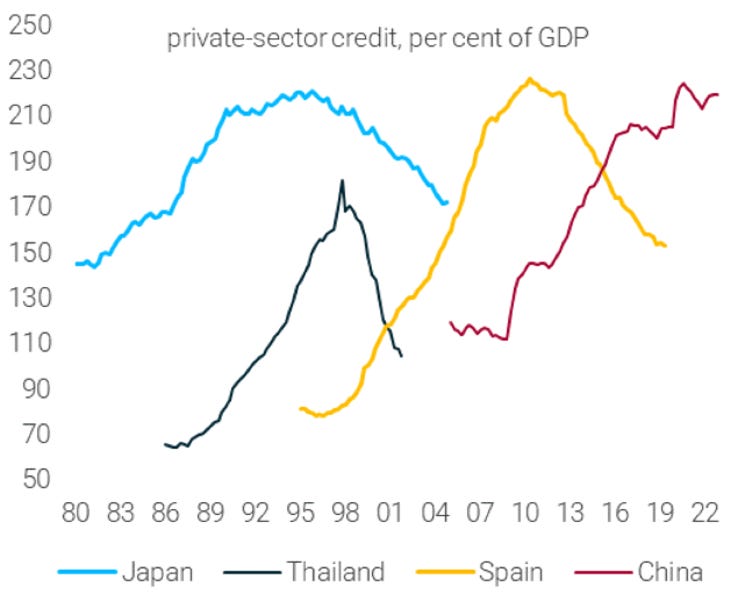

Macro – China

From one of the most astute and successful macro and market observer distilling his wisdom freely on Twitter (is this even legal?).

Some more graphs…

Market - Liquidity

Value agnostic systematic strategies had their first notable selling last week but they remain very long. There are hundreds of billion of potential supply on further decline (domino style).

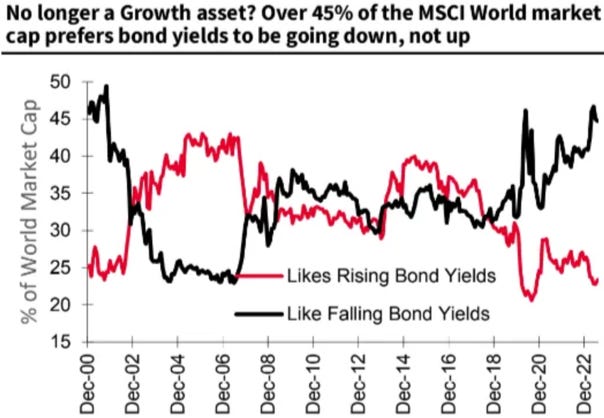

Market - Intermarket

This graph is based on the idea of M. Green. Some see it has the markets discounting fiscal dominance.

This is even more noteworthy now that the majority of the MSCI World market cap prefers declining bond yields (wasn’t the case 5 years ago).

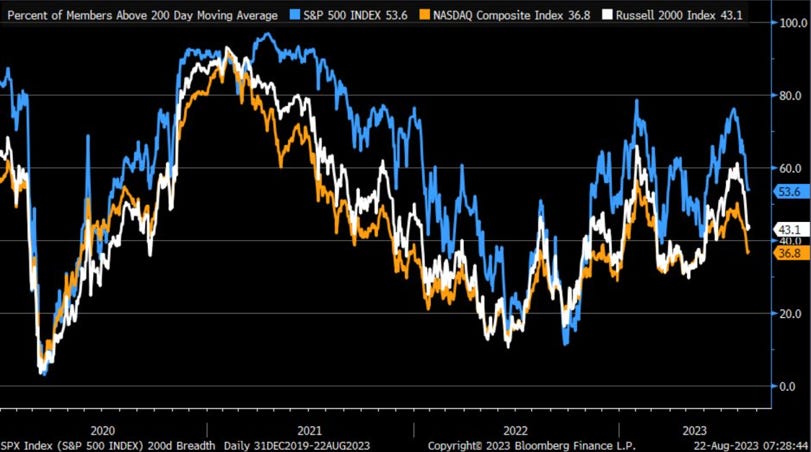

Market - Breadth

Breadth remains unsupportive.

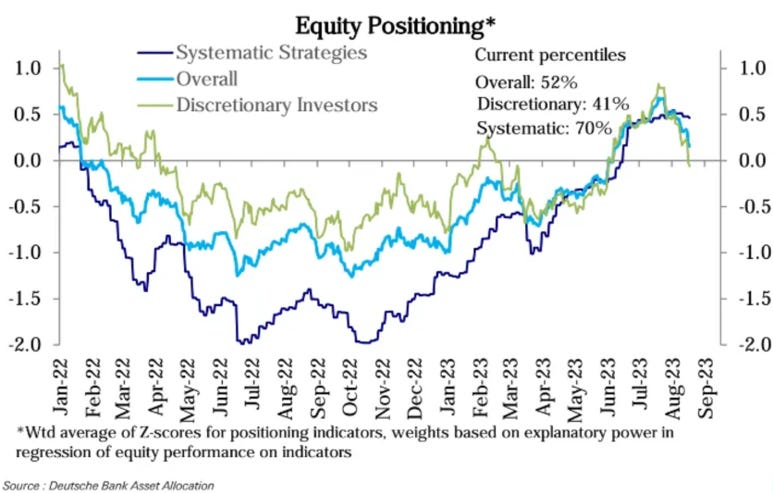

Market - Sentiment

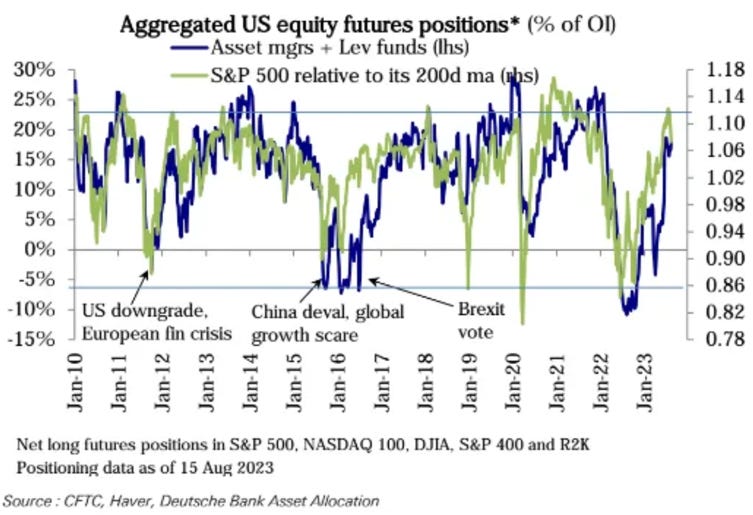

Hedge funds have decreased their net long exposure recently while mutual funds have decreased their cash holdings. The latter is very low given prevailing short-term interest rates and does not leave much cushion were investors rushing to the exit.

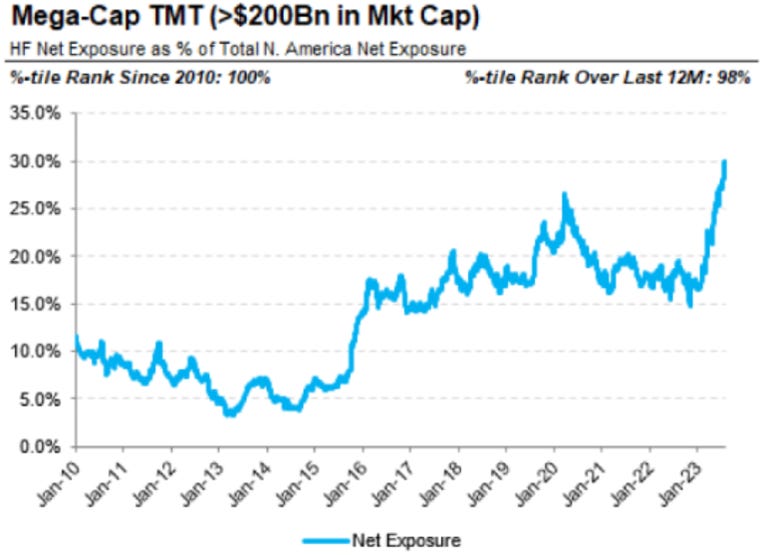

Hedge Funds remain very exposed to mega cap tech names.

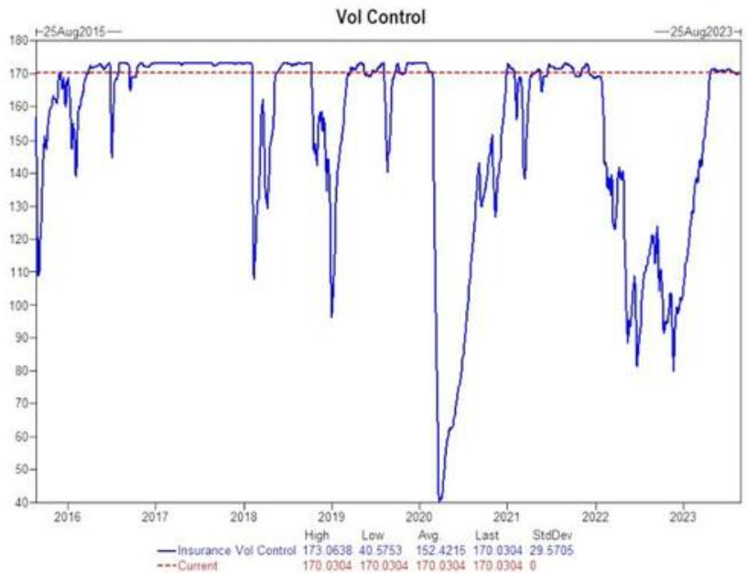

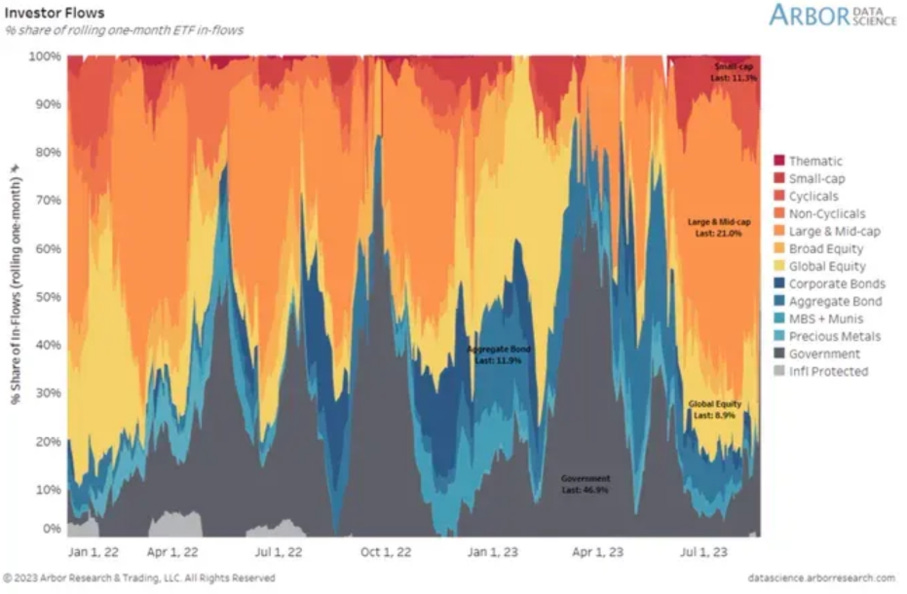

The rolling one month flows into ETFs are giving the same message.

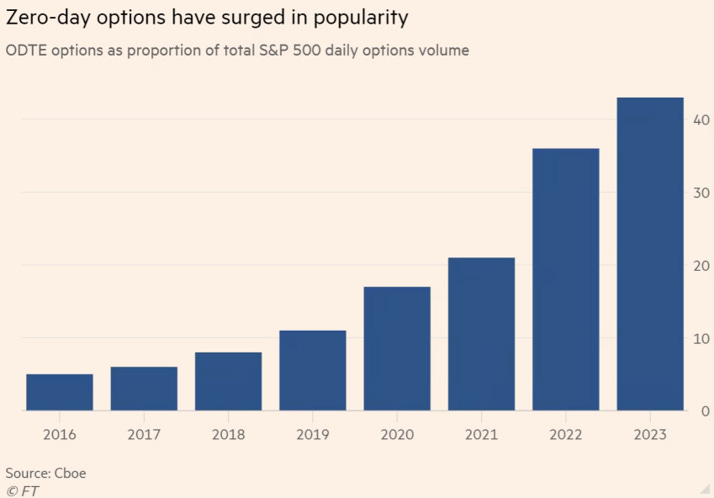

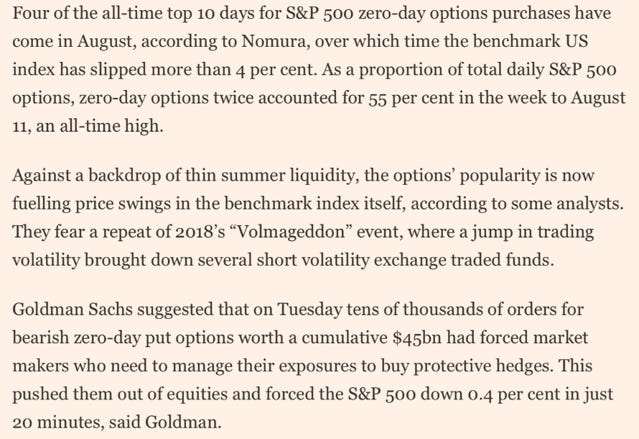

There has been much talk about the rise of 0dte options which are representing an increasing volume (directly or indirectly) of the overall market volume.

Goldman Sachs estimates that it puts woods into the fire of last week decline.

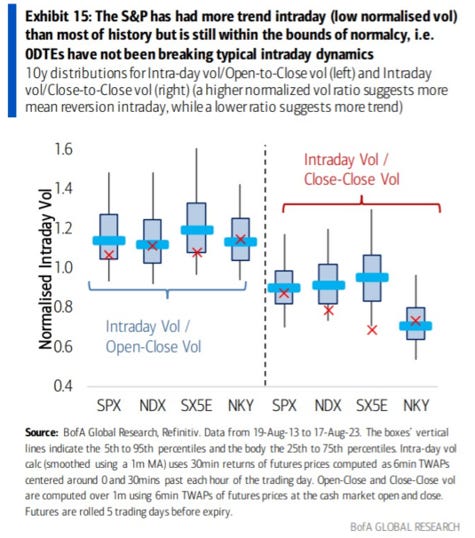

Bank of America analysts do not think they really change the market behavior with regard to day trends.

Yet given the option volume and increasing size of dealers’ gamma exposure, it seems unlikely that they have no effect. It will be interesting to see what happens if the markets experience large gaps to the downside.

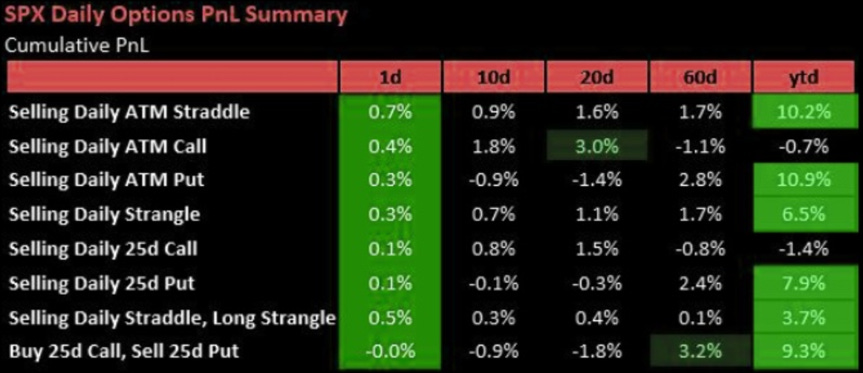

As for now, option sellers are still in party mood!

Market - Valuation

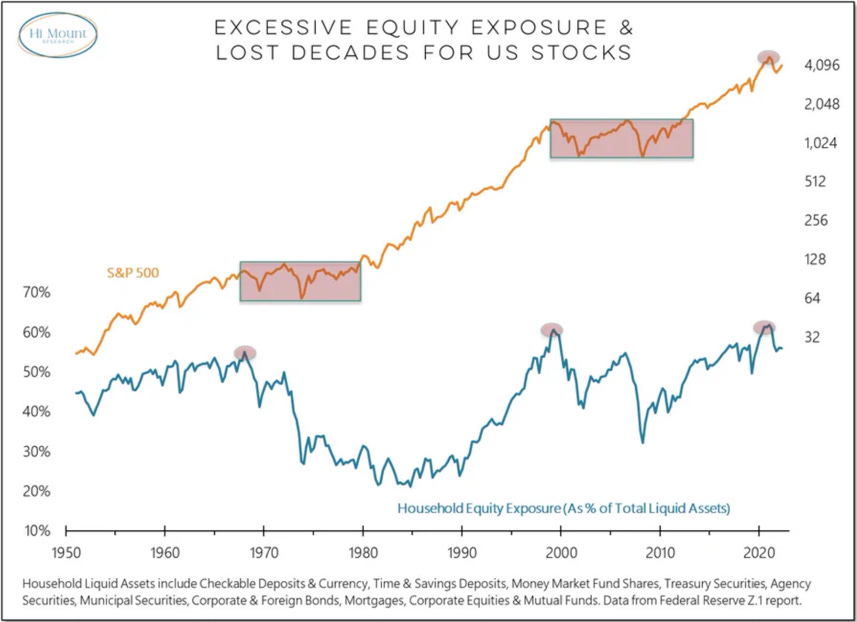

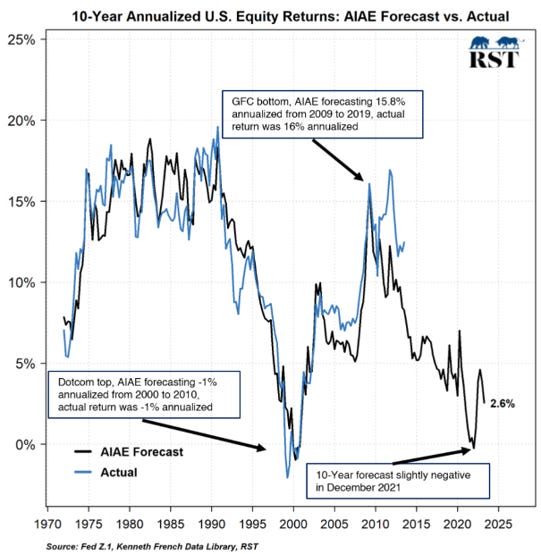

Households equity exposure as a percentage of total liquid assets has been popularized as an alternative to valuations to forecast multi-years forward.

More positive than our valuation-based estimate but…

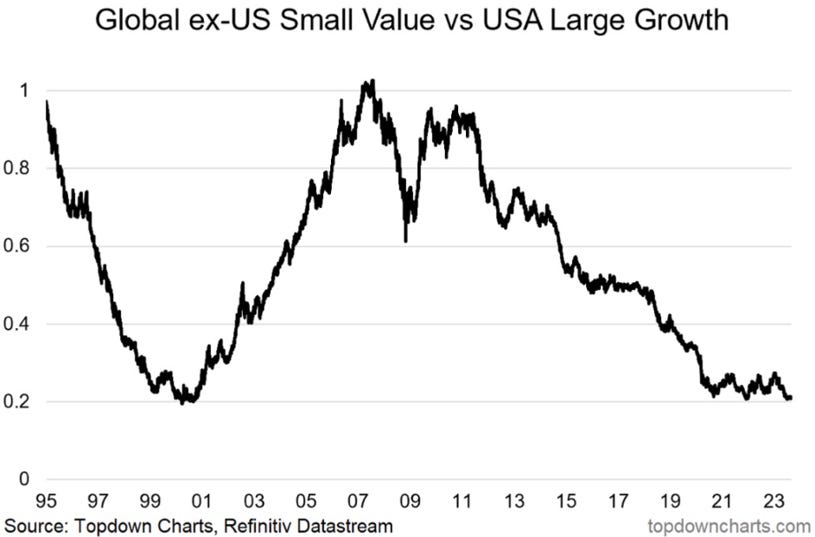

While it is still too early (due to small cap higher sensitivity to the macro cycle), small cap value stocks outside of the US could outperform large cap growth stocks massively in the future.

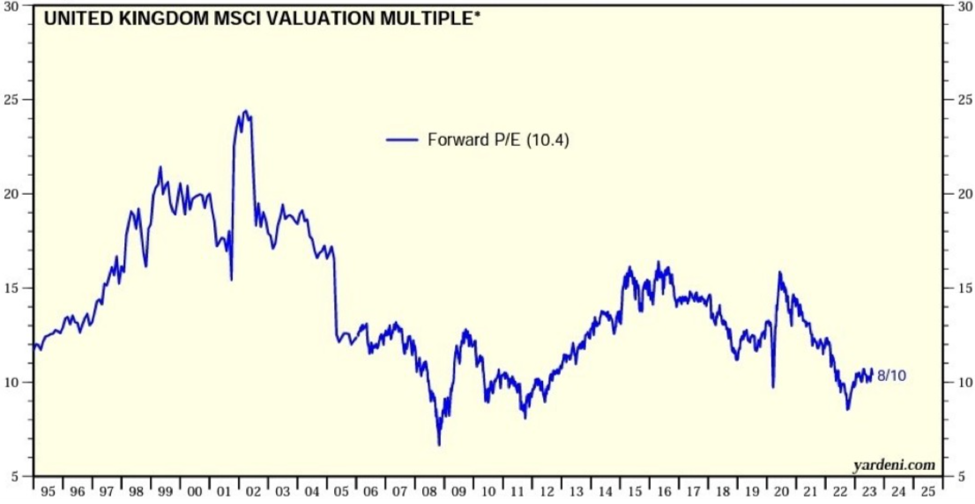

The UK market is universally hated. While the GBP might be a total return headwind for foreign investors going forward, this market must be a fun playing ground for value investors of all kind.

And Nvidia could not not being mentioned this week. Important to say that we have no special insights on Nvidia, so do not take our word for it. We neither have any short positions in the stock but… exploding revenues and profit with declining costs on such a short-period feels like a pure pricing power play. Might continue but with such margins many will try to produce alternatives. Remember Cisco explosive growth in 1998-2000? The stock lost almost 80% into 2011. Once again not a prediction!

Others

Some wisdom from M. Pettis. The balance of payment is often misunderstood.

M. Summers, I have another graph for you!