August 21, 2023

Summary

More of the same

• Yield Curve

• Budget Deficit

• Central Banks

• Inflation

• Households

• Housing

• Liquidity, breadth, sentiment, valuations

- China, China and again China!

Macro – Make Math Great Again

While we have some sympathy for J. Milei resentment towards Central Banks (we recommend everyone to read M. Rothbard “The Case against the Fed” which can be found for free here), we are still wondering what the fourth category is…

Macro – Yield Curve

We always need to keep in mind that correlation is not causation, that’s why one should always accumulate as much loosely related data, build as many structurally different models as possible and look at consensus to get conviction. One should be as agnostic as possible to individual data and model parameters.

Thanks for reading Damien’s Substack! Subscribe for free to receive new posts and support my work.

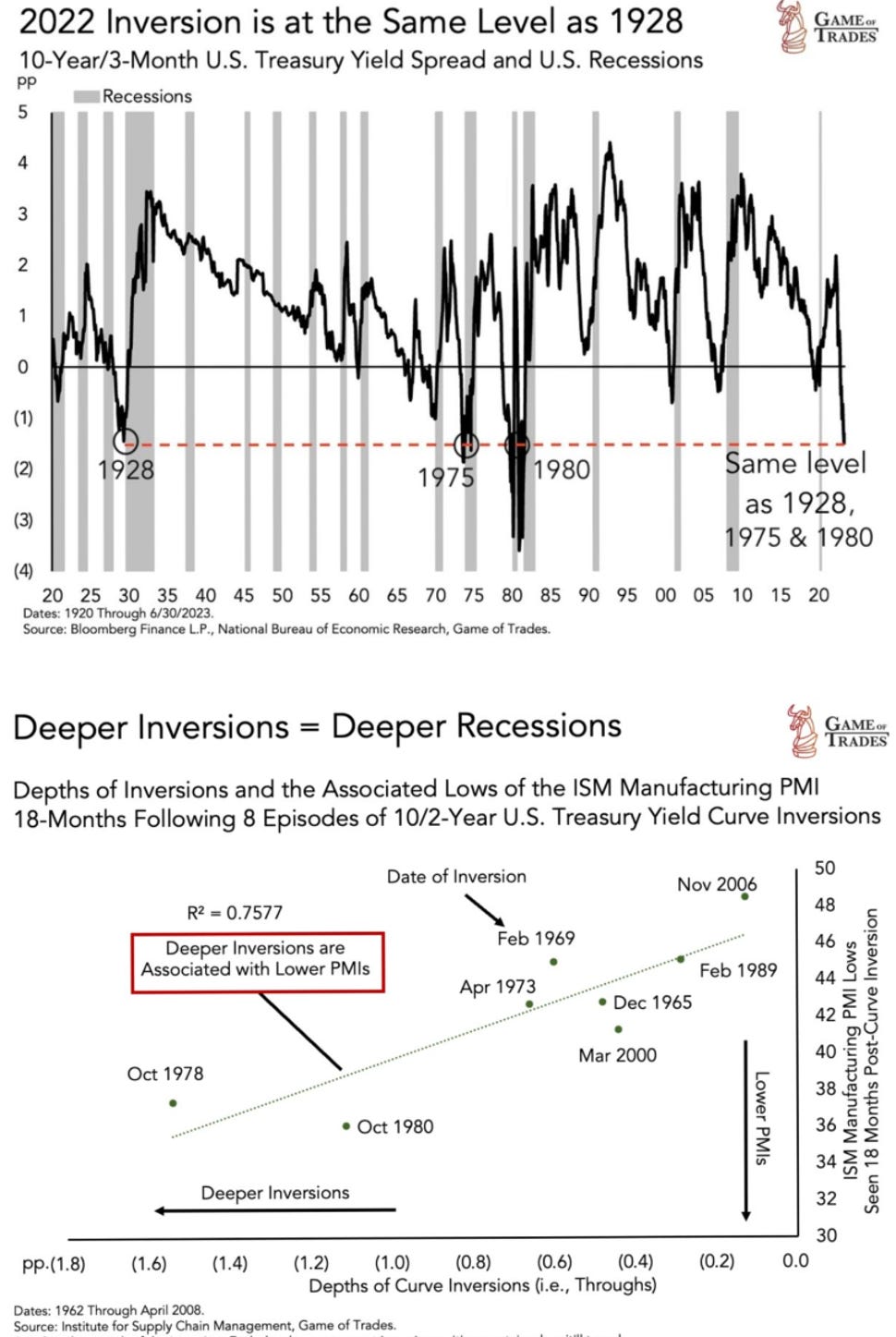

The yield curve is inverted in the US and elsewhere, often deeply so. As we showed in the past, inversions can be a sign of the market anticipating a recession, but it can also be the market expecting inflation to fall sharply.

Macro – Budget Deficit

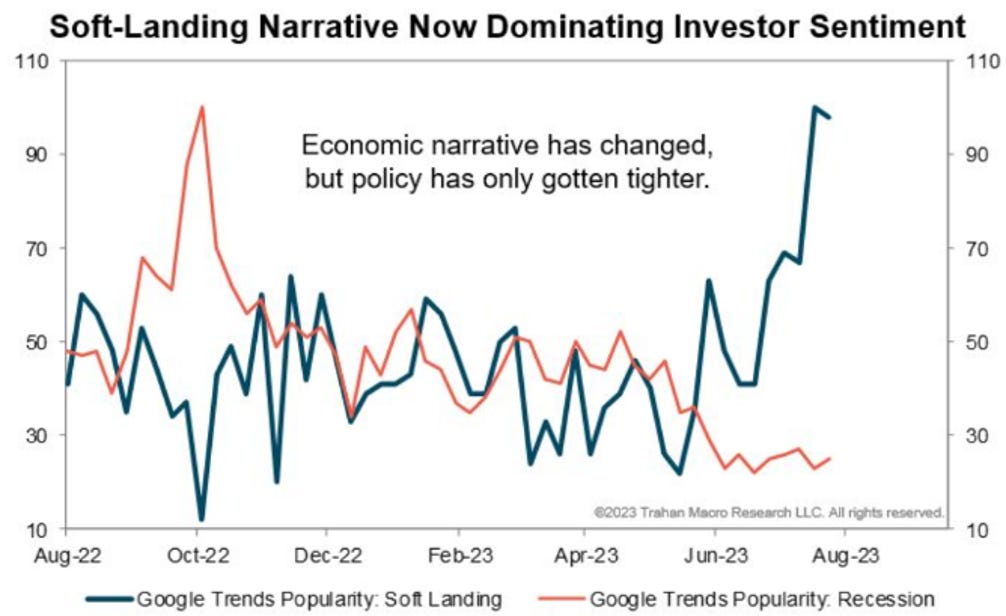

The «Soft Landing» narrative continues to gain momentum. We showed plenty of examples in our previous MashUps why this is exactly what happened before previous recessions.

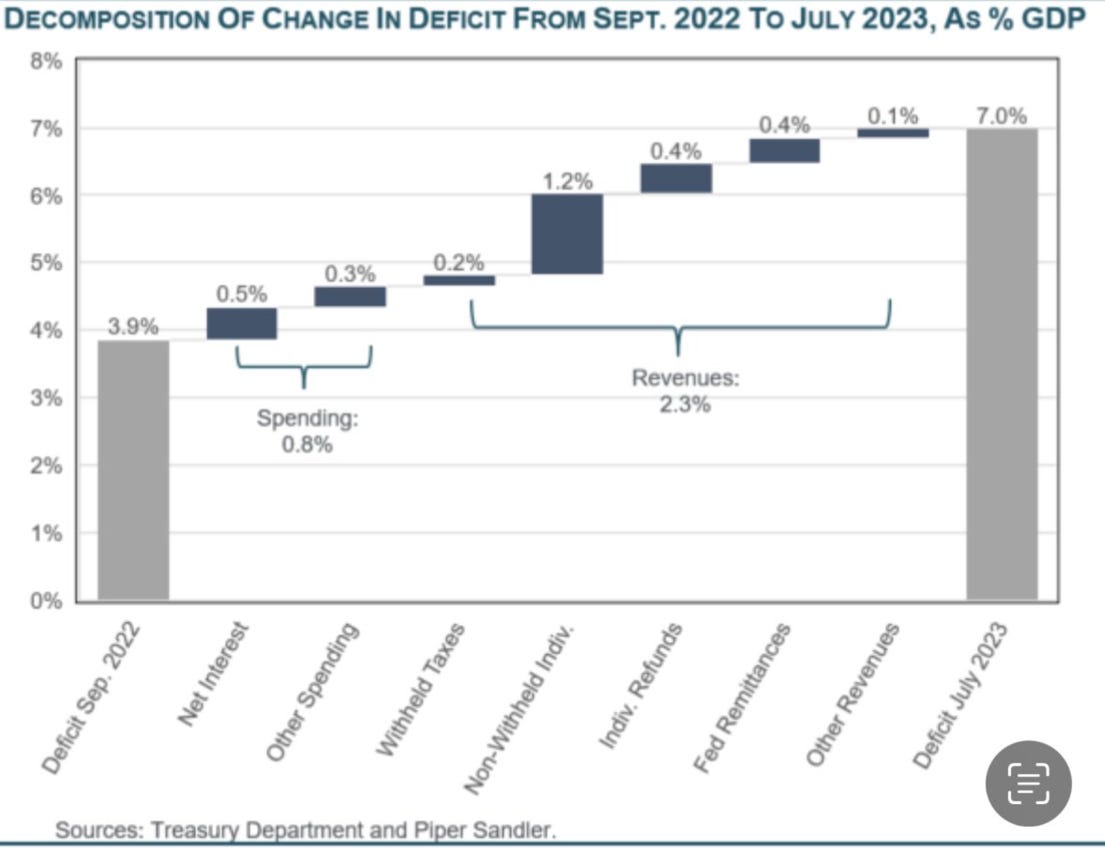

An interesting graph from Piper Sandler showing that the US budget deficit has increased predominantly due to a decrease in revenues and not an increase in spending.

Remember that for Californian the tax declaration deadline has been moved outside of the 2023 fiscal year (ending September). They now have to file in October and it represents circa 15% of total US household taxes!

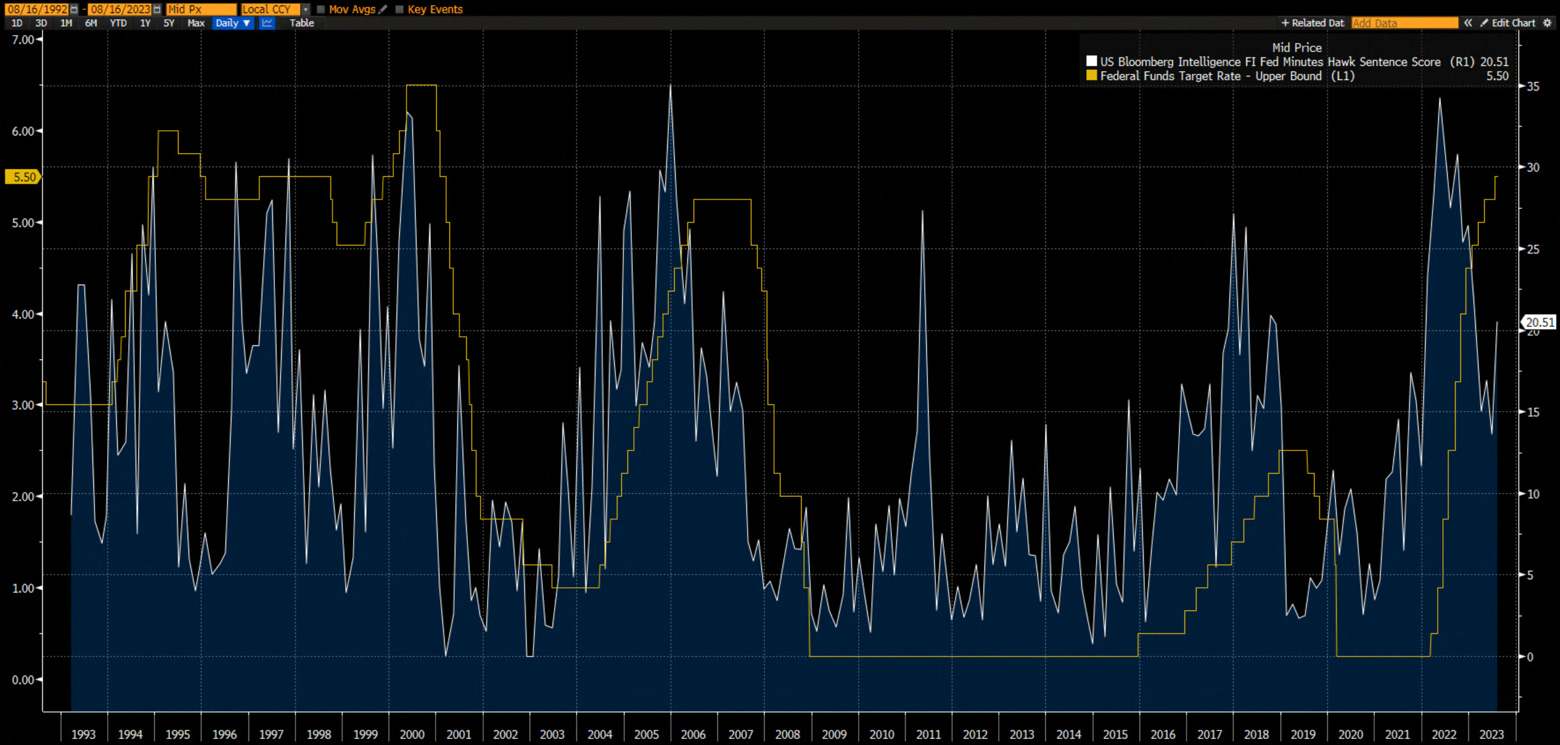

Macro – Central Banks and Inflation

The Bloomberg Intelligence Fed hawkish sentences score has rebounded in the past few weeks.

While fund managers surveyed by Bank of America almost universally expect lower global CPI.

The ECB credibility (if it still had any) is tested by the markets.

Macro – Households

The varying impact of rapidly increasing interest rates on households and corporations, depending on their income /balance sheet quality, has been predominant in our last MashUps. P. Atwater and

H. Greenberg disagree on the impact. We would tend to agree with P. Atwater. On a 10 year horizon, savers buying power will also be severly curtailed given the global debt overhang. There is no escape.

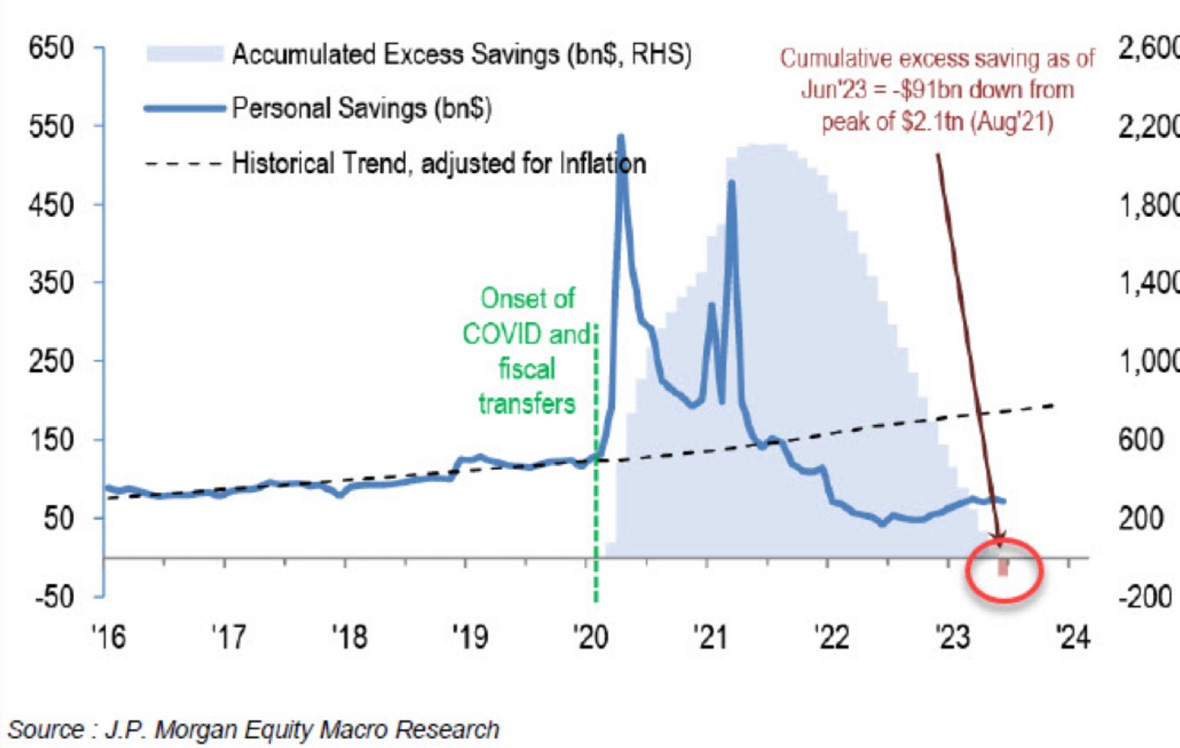

Accumulated excess savings are now on aggregate gone. The lower the households are in the income ladder, the quicker those savings disappeared. Now only the richest, with the lowest propensity to consume households still have some...

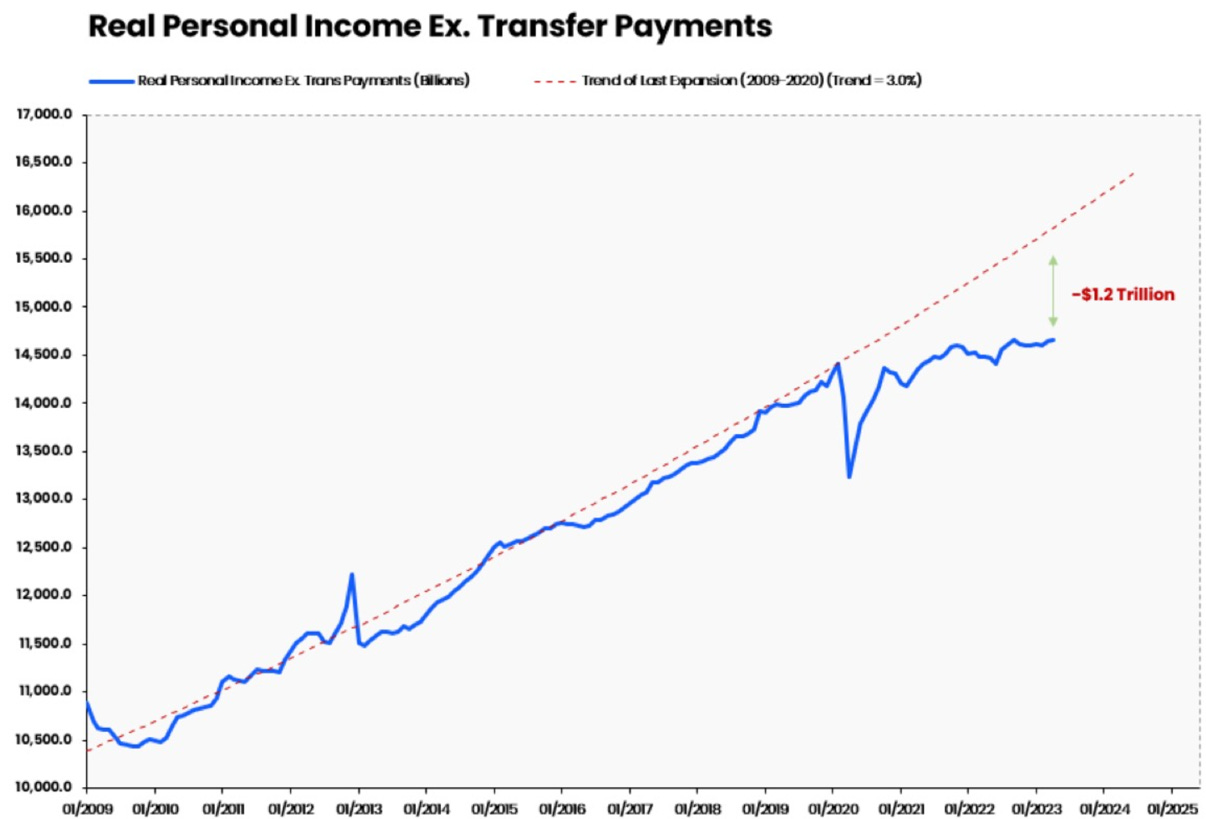

… but households still have > USD 1 tn real personal income shortfall relative to trend. You now know why employment numbers are so important going forward (and you know we think it will disappoint).

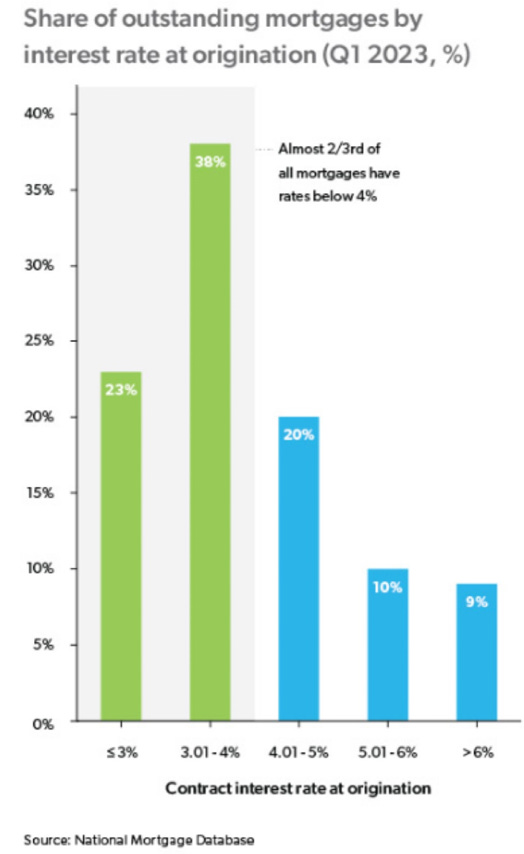

The people who were lucky to have enough money to buy a house or could refinance it per 2022 have low interest rate, 30 years mortgages.

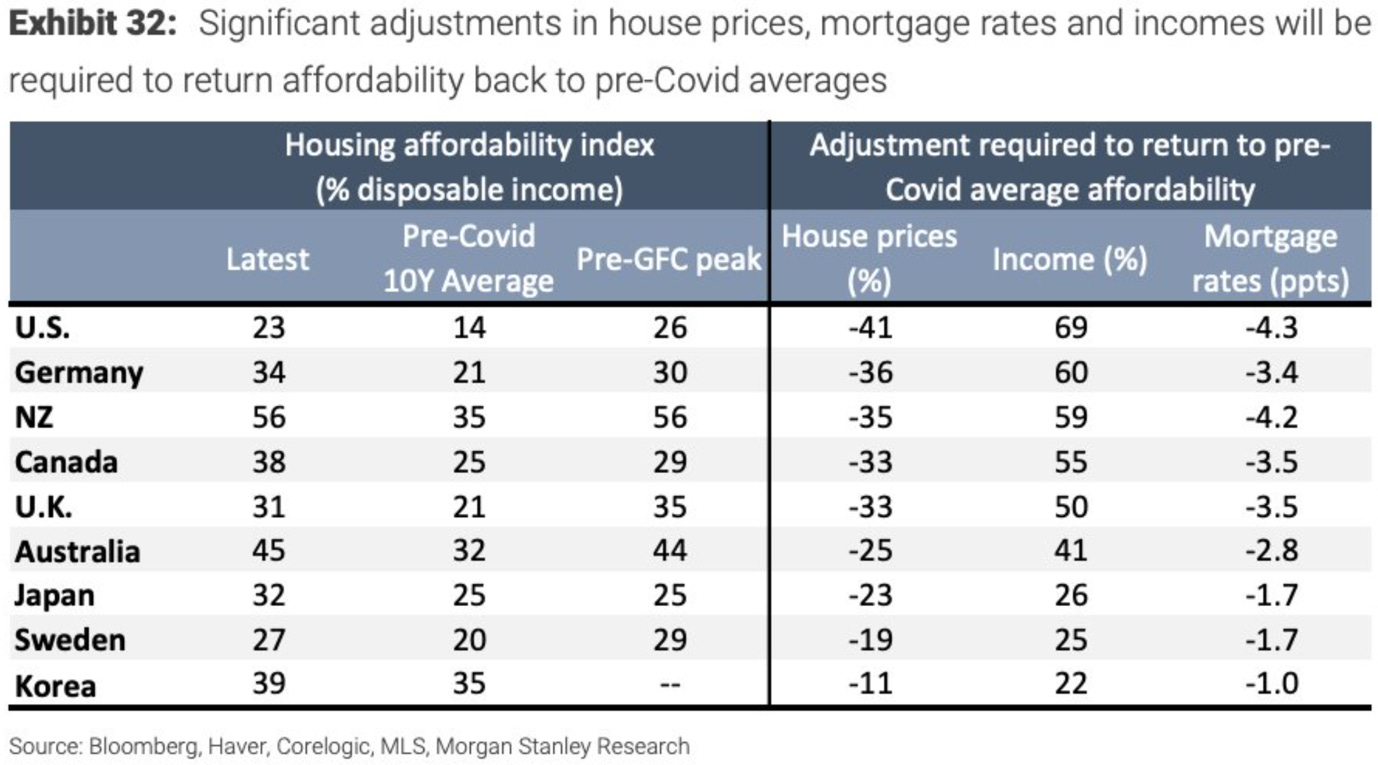

Macro - Housing

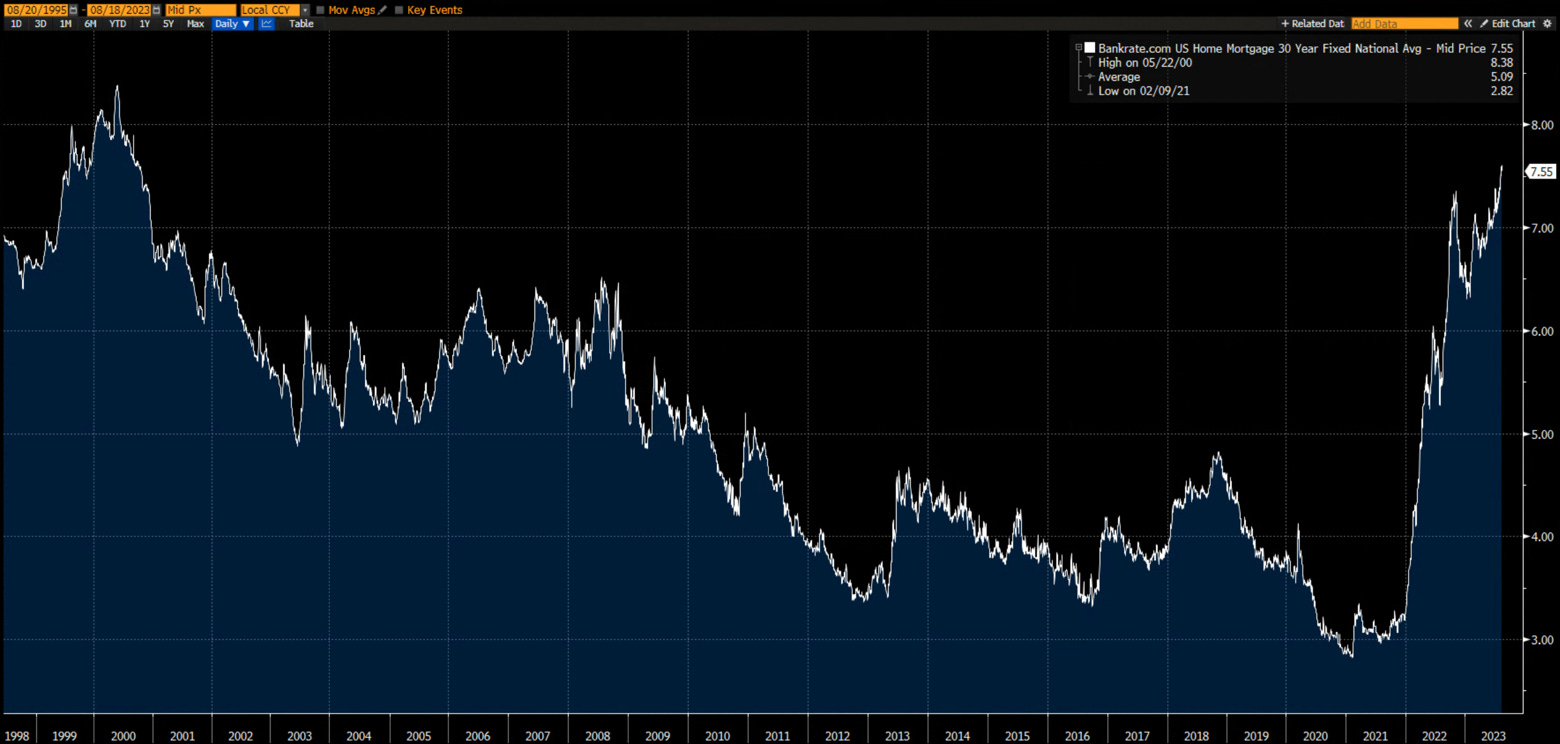

The others are faced with rates not seen in more than 20 years.

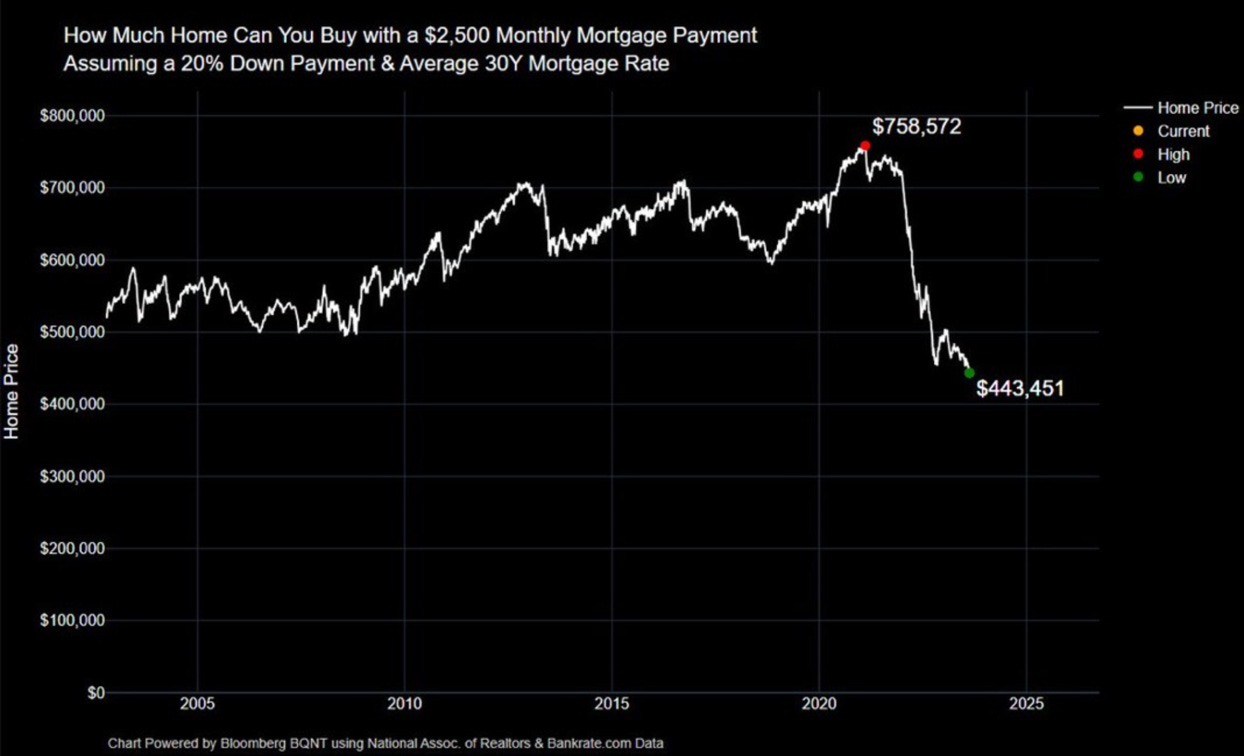

Another way to show how unaffordable housing is to new buyers today…

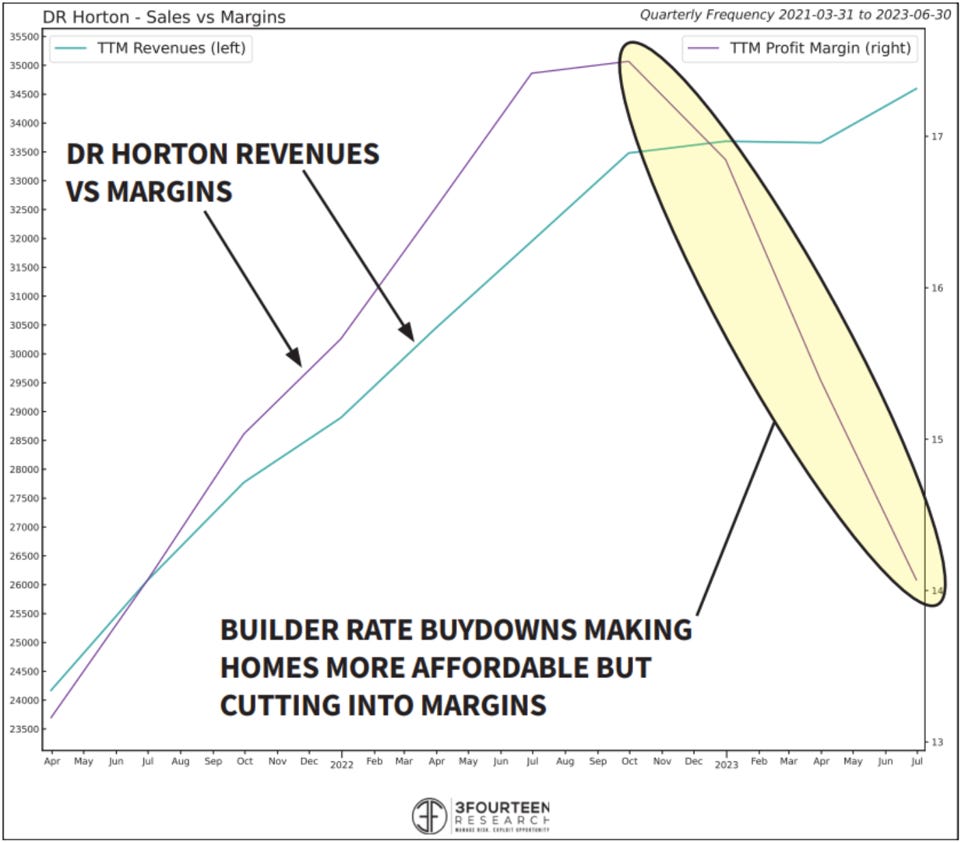

Even now that homebuilders are using their income statement and balance sheets to «help» the households buying new houses.

The situation is similar in many other markets with the main difference being that, contrary to the US, mortgages have on average a much shorter duration.

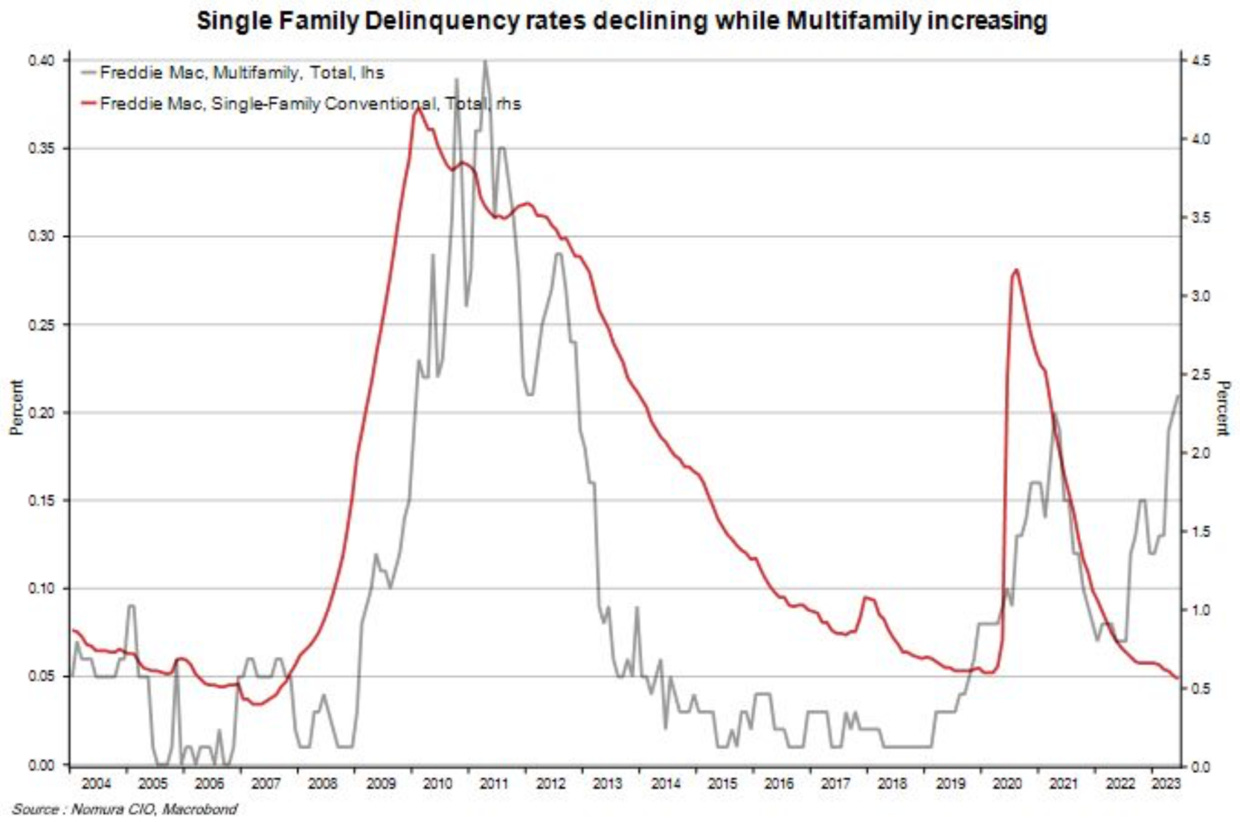

In the US the first real signs of stress are in the multifamily sector. As said before, we believe this will be the epicentre of any potential residential real estate crisis. Financing is short-term by nature and there is too much construction going on (see our latest MashUps for more on this).

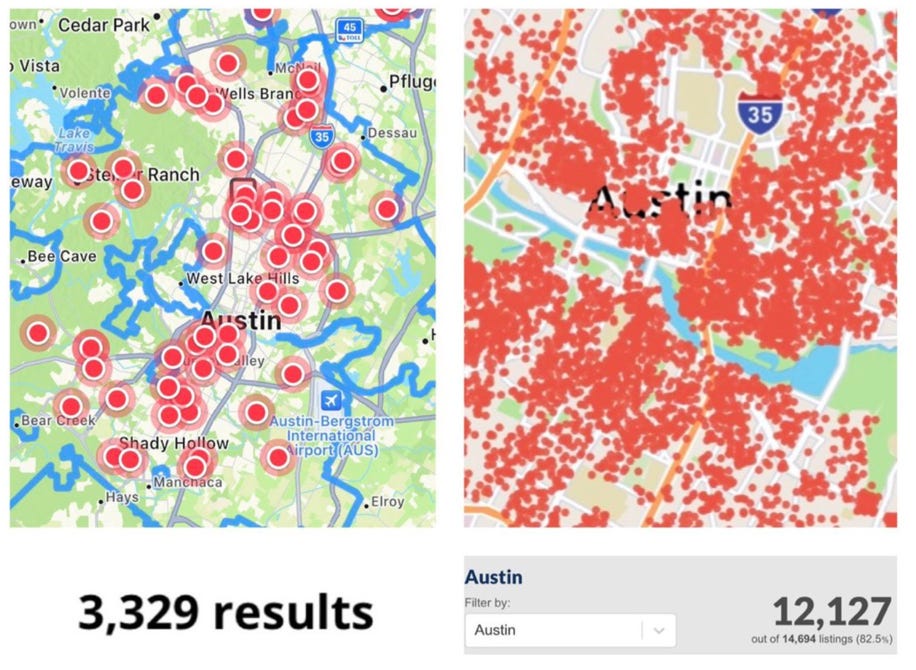

We alluded to the short-term rentals boom in the US before. The sector is more exposed to short-term interest rate moves and experienced a bubbly boom in the past few years. Some signs of stress are slowly emerging. Looking at Austin, for example, there are 12’127 Airbnb rentals and now 3’329 housing units to sell. Leverage goes both ways!

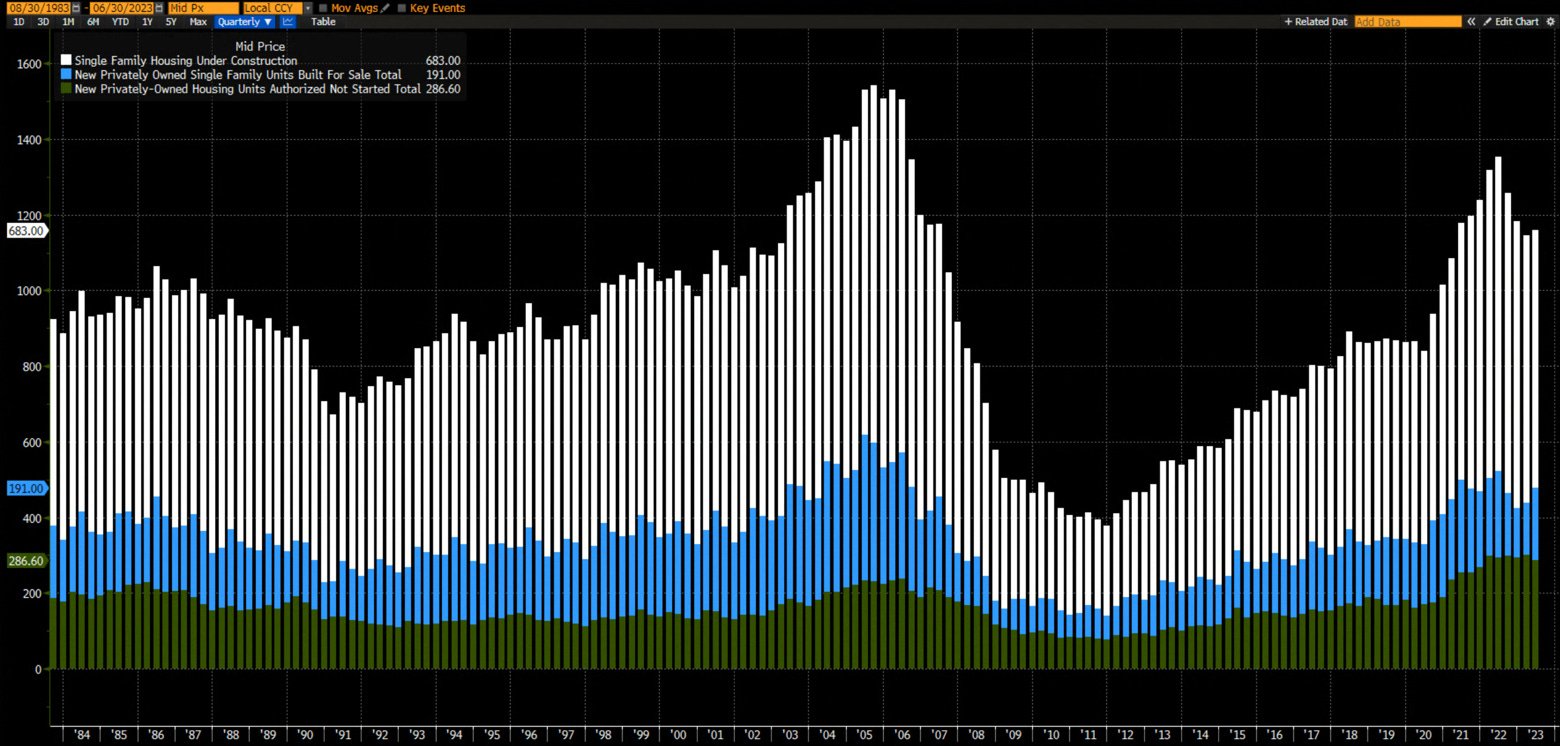

With regard to single family houses, the vacancy rates are still very low. If the employment market deteriorates significantly, the current units under construction, for sale and in planning, could drag prices down and/or create an overhang.

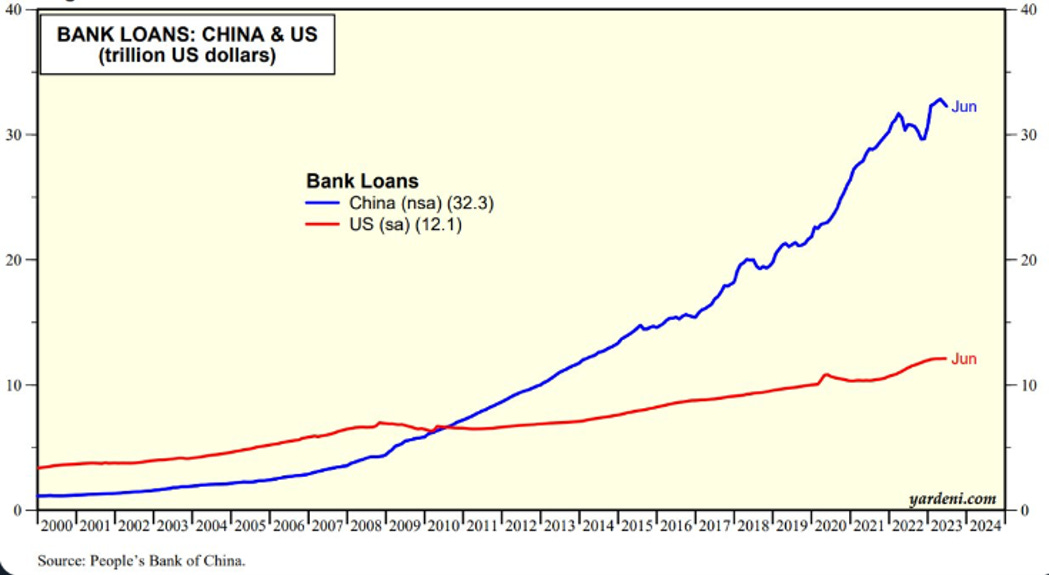

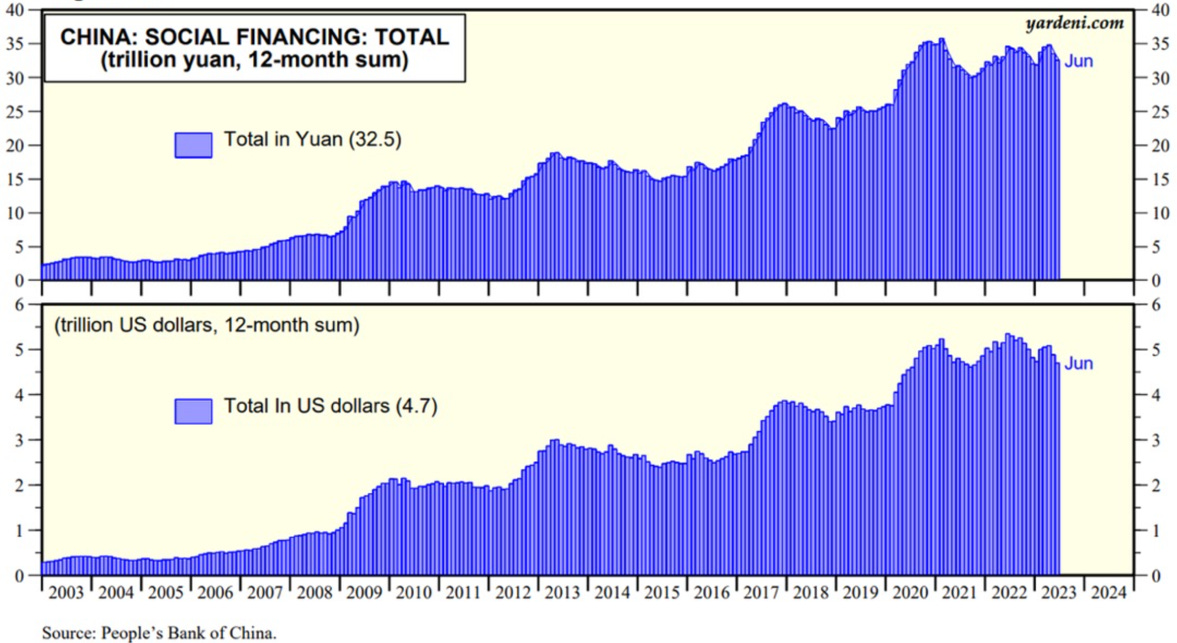

Macro – China

Let’s now move to China which made headlines recently.

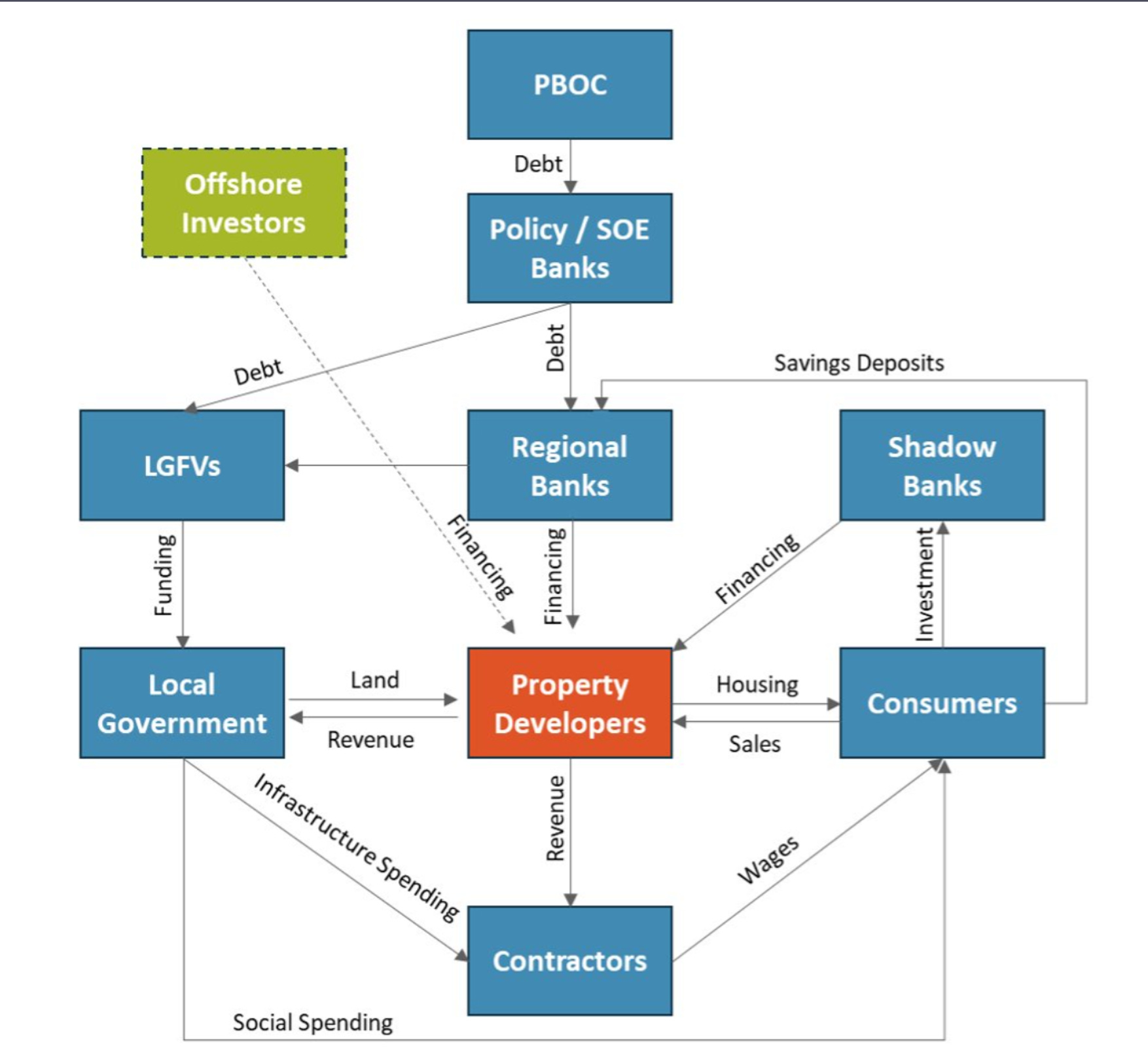

M.Pettis is an astute observer of the Chinese economy so let’s start by one of his threads and a recent article he wrote.

Here is a very good schematic illustration on the Chinese macro machinery.

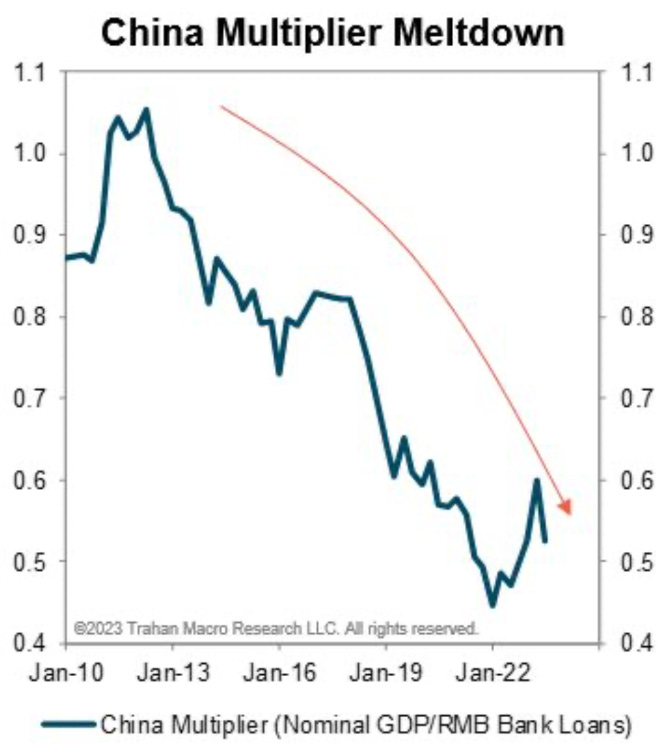

China is becoming less transparent. Macro statistics were known to be ‘massaged’ but now many are discontinued (lastly youth unemployment which was reaching extremely high levels).

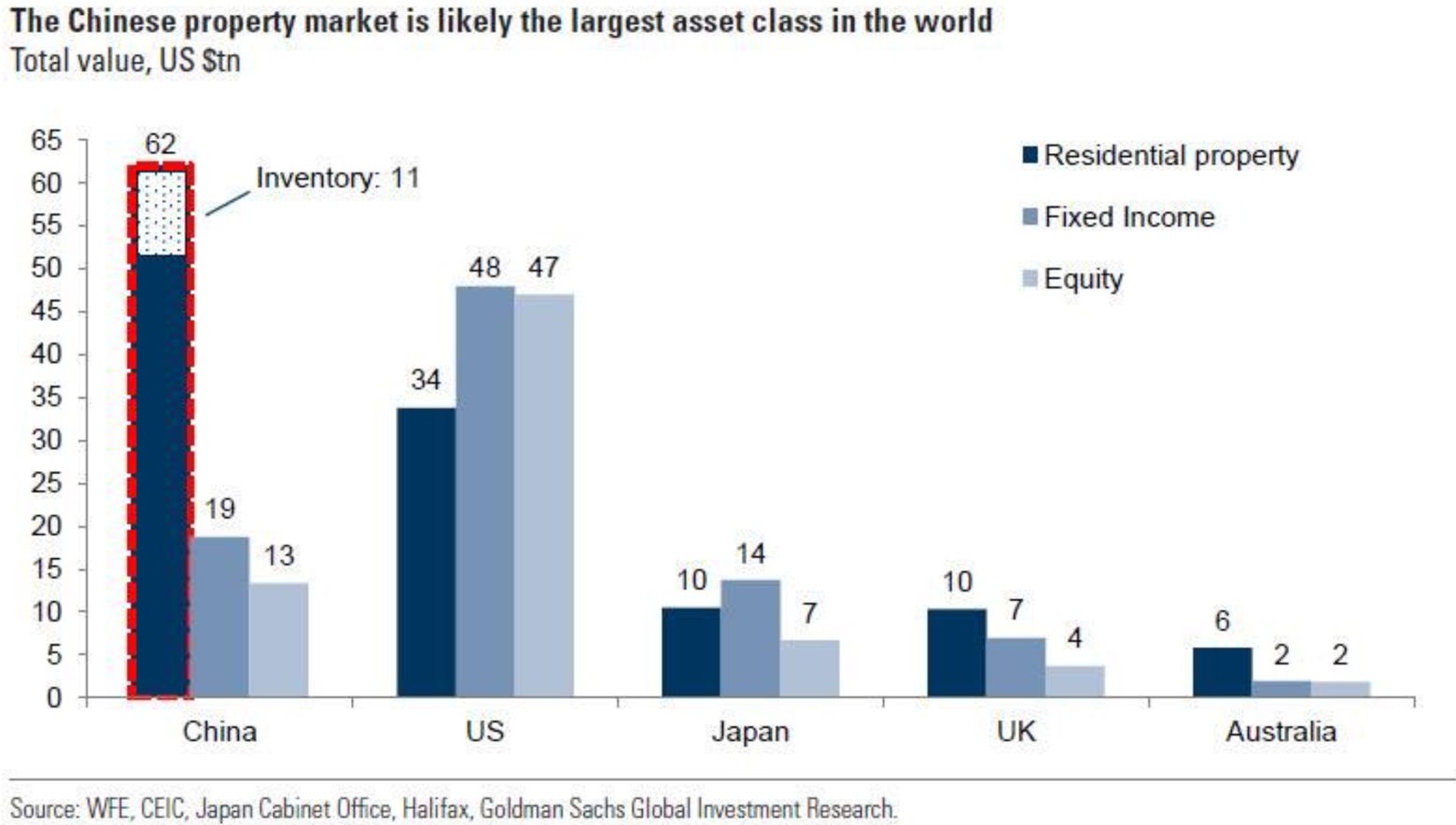

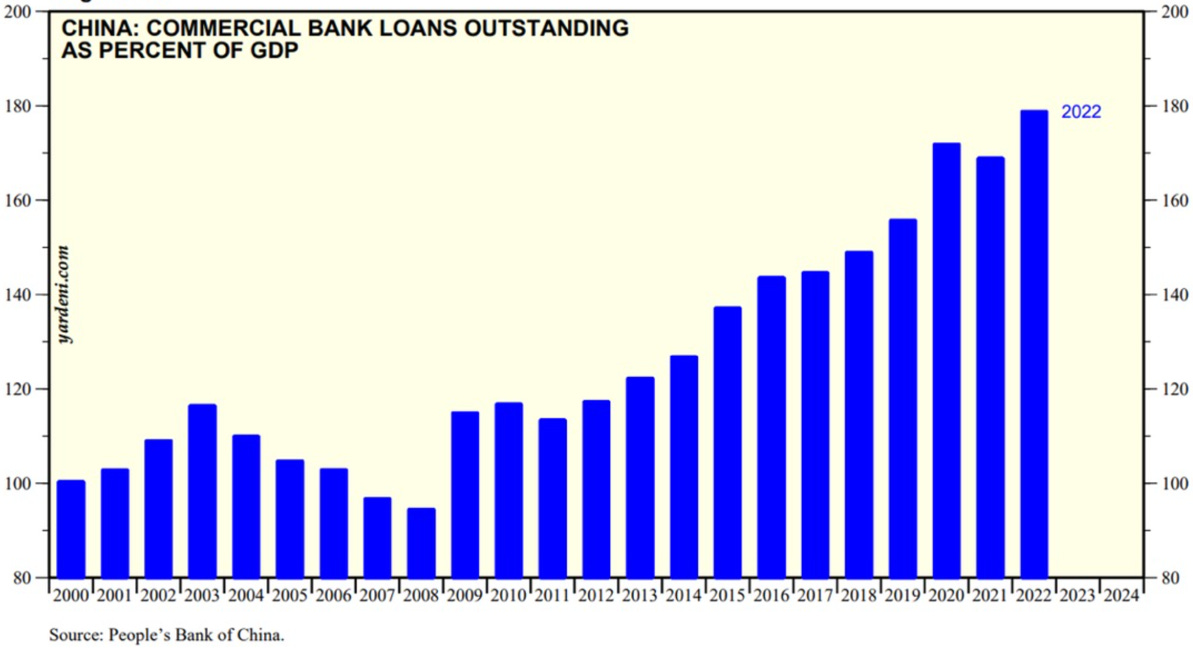

And one should not forget that the Chinese residential property market is the largest asset in the world, by a wide margin and that it has an estimated inventory of more than USD 10 tn!

The sector is also highly levered which, combined with inventories, is not a good combination.

And everything indicates that the quality of the investment made with this leverage has been rapidly declining (nice way to say that we probably witnessed the biggest malinvestment boom in human history).

The real estate sector is suffering with some large bankruptcies.

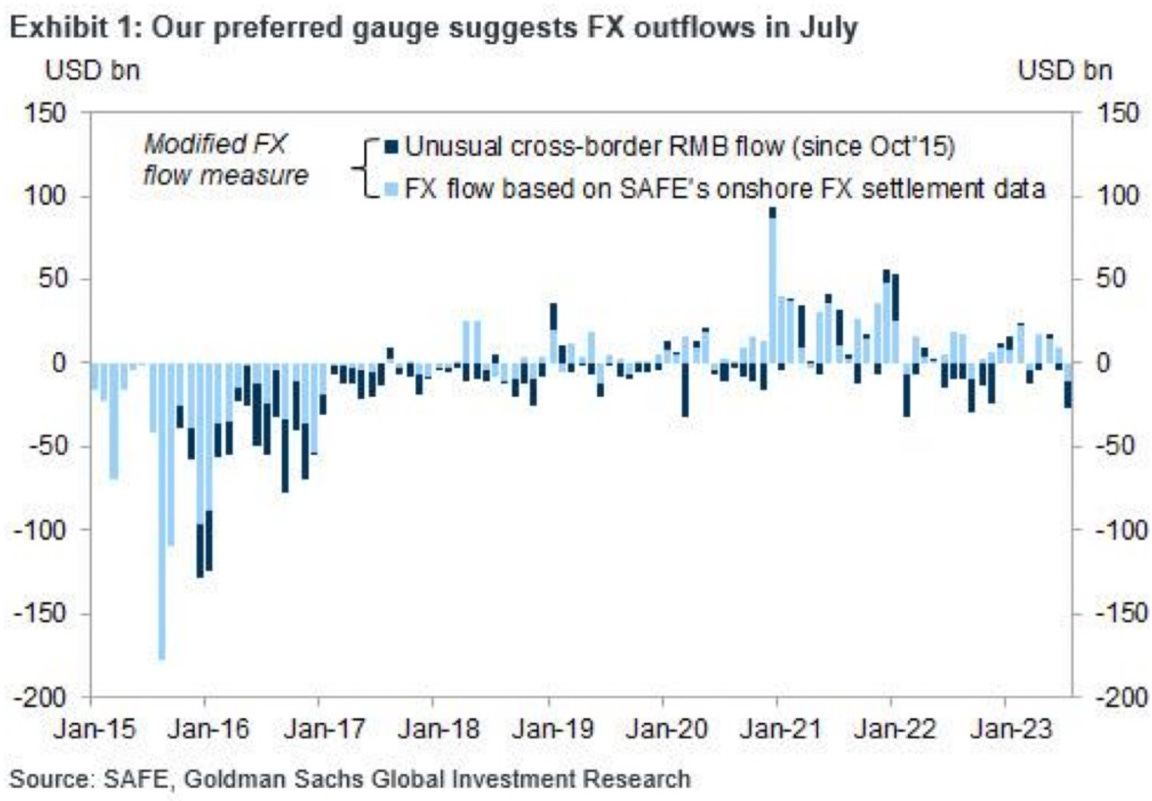

There are some signs of capital outflows, but they remain modest.

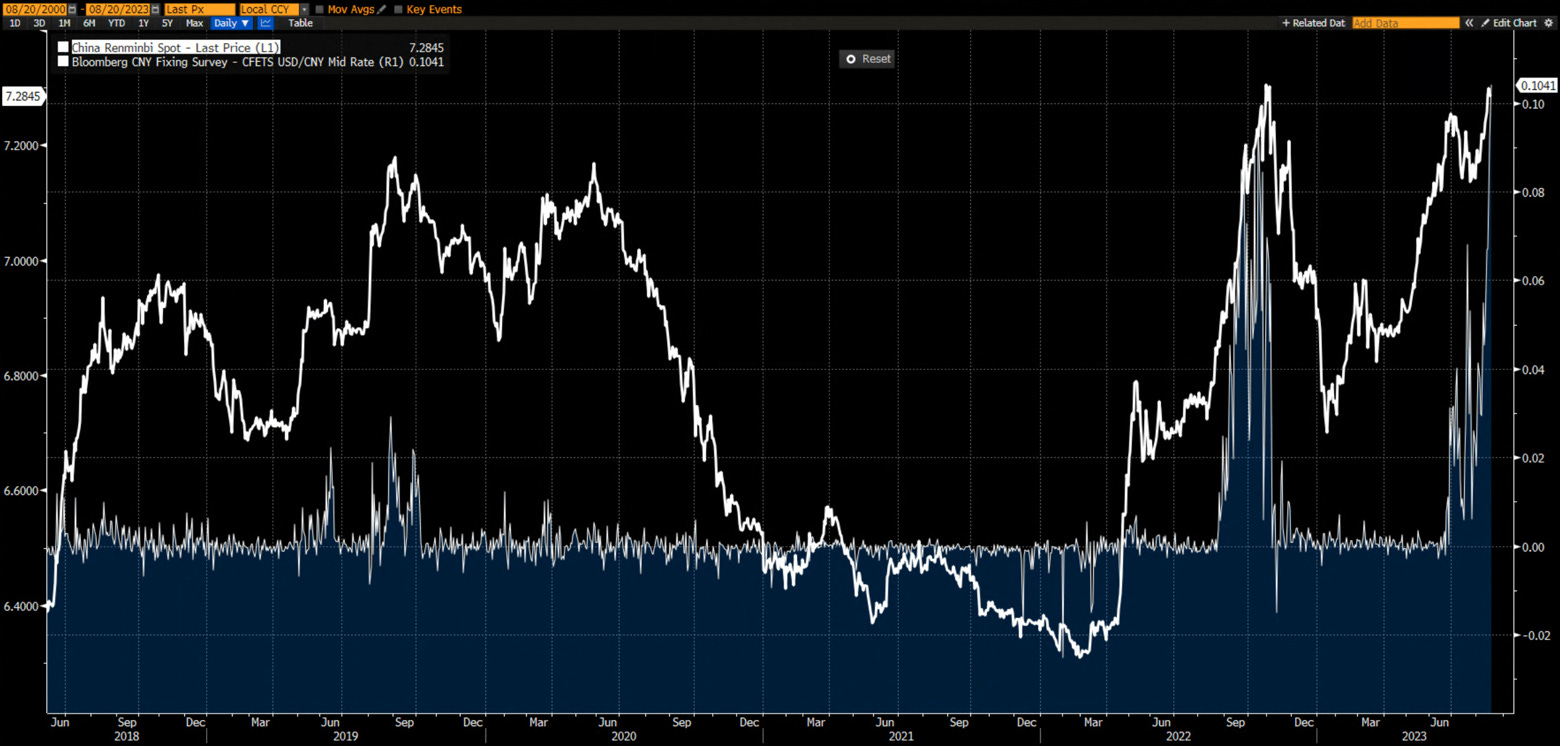

In order to avoid a rapidly falling Yuan, which would exacerbate outflows, the PBOC is, as it did last year when the Yuan fell precipitously, fixing it far from market expectations. Anyhow, given the decline in the JPY and the current Chinese macro backdrop, the CNY could easily break above 7.3 and move much higher.

Rate differentials are also pointing that way…

We will finish this section with some tweets from B. Elliott

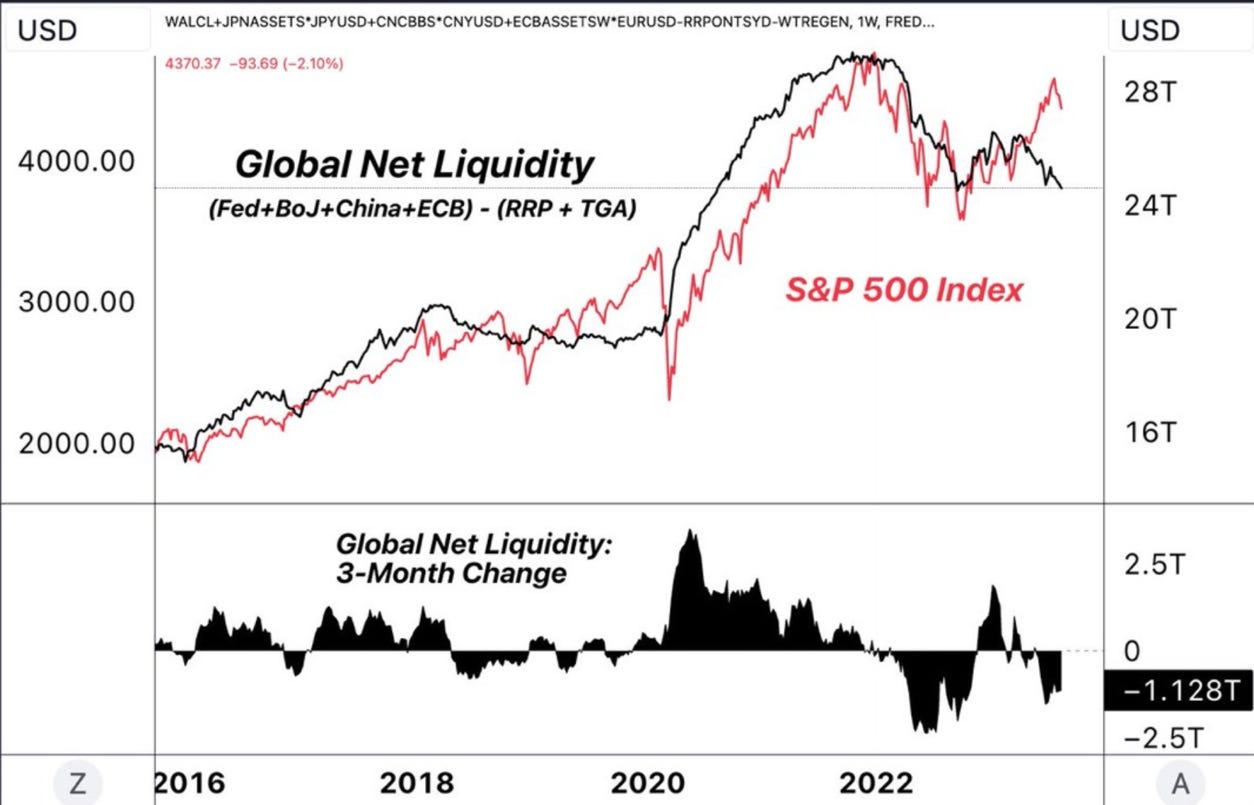

Market - Liquidity

China importance for the world economy is well known. Markets are hoping for a new debt-financed stimulus package. Who cares about tomorrow!

And liquidity momentum is not supportive elsewhere too.

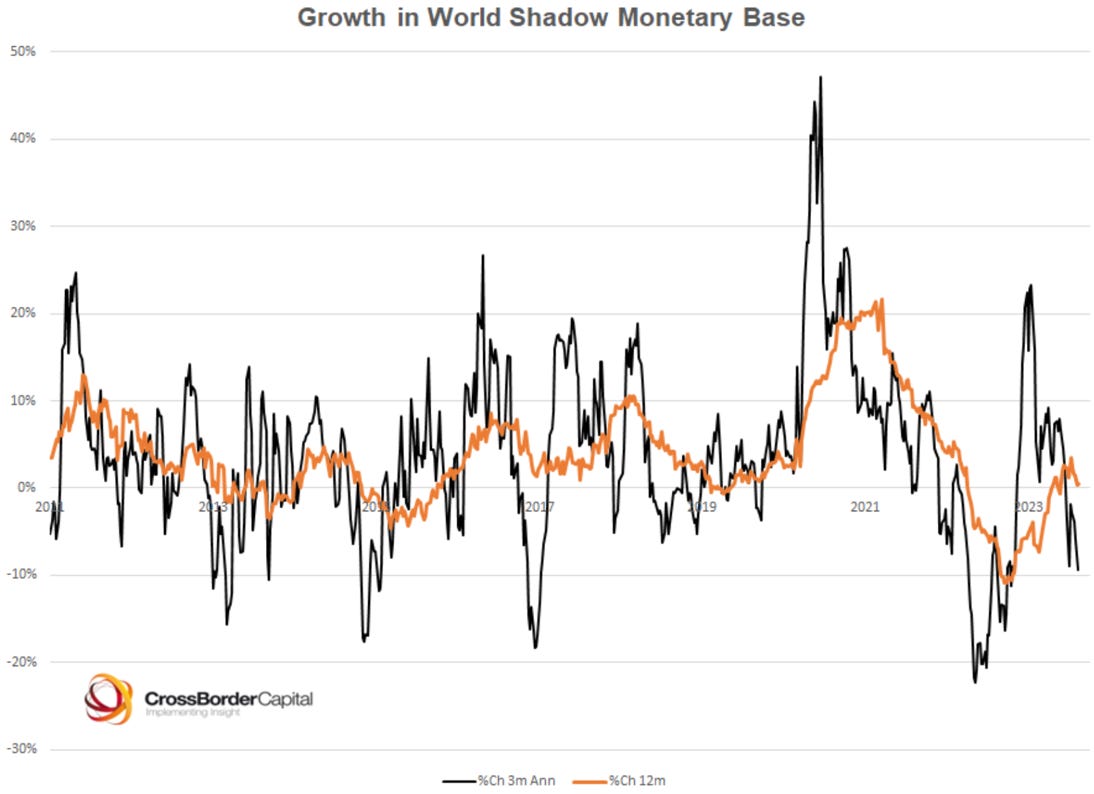

CrossBorder Capital World Shadow Monetary Base is not supportive either.

Systematic strategies (Vol target, risk parity and CTA) have barely started to sell the equity positions they have accumulated since the bottom of October 2022.

Market - Patterns

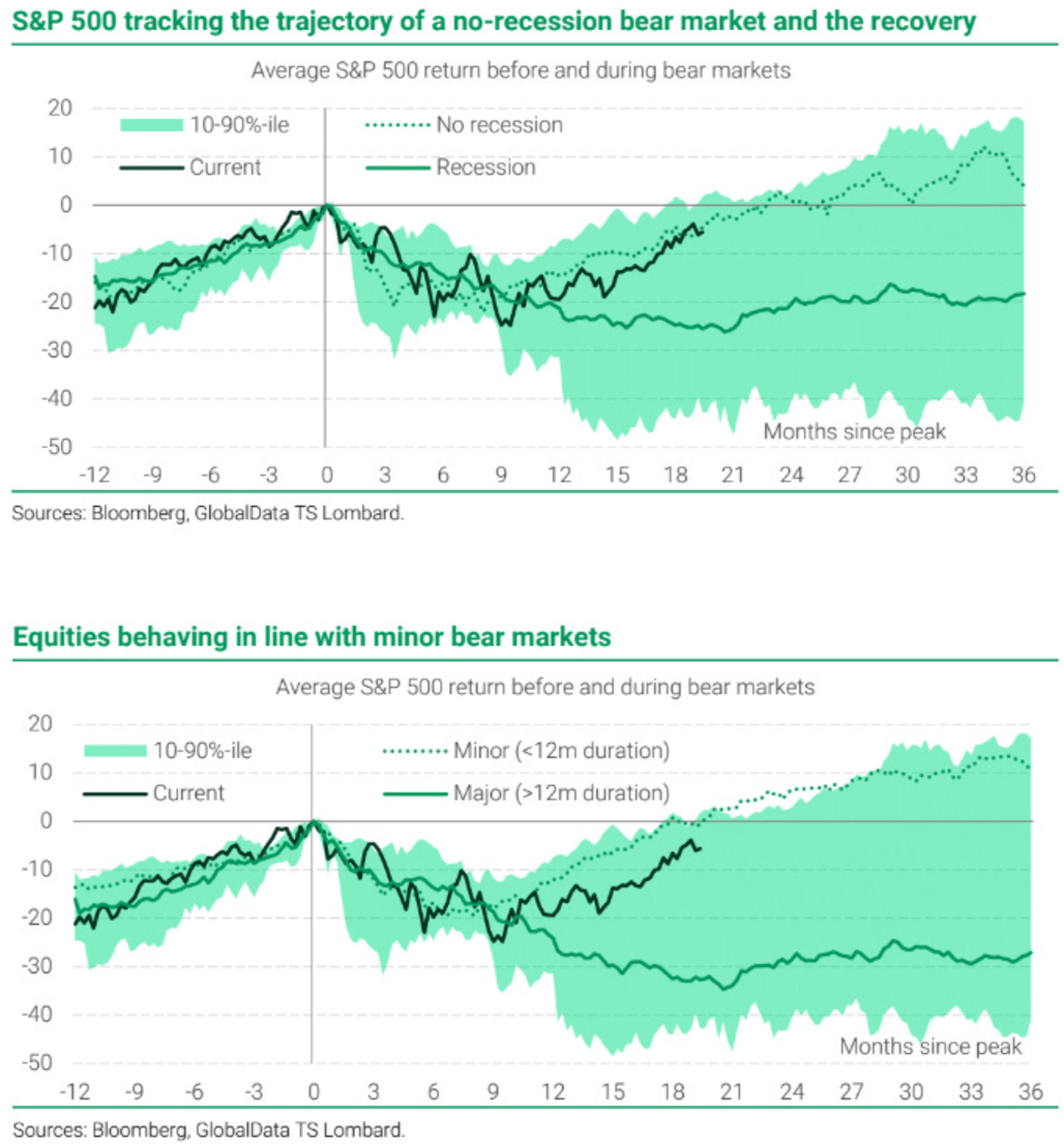

Looking at price only the S&P 500 is not pricing in a recession.

The 2023 Charles H. Dow Award Winner paper is being tested right now. The markets need to fall early this week for a bearish 5% Canary signal to trigger.

Market – Breadth

A quick rebound on strong breadth would, on the contrary, potentially generate a «Zweig Breadth Thrust».

Yet overall breadth remains poor. One example below…

Market – Sentiment

B. Farrell was a very smart investor…

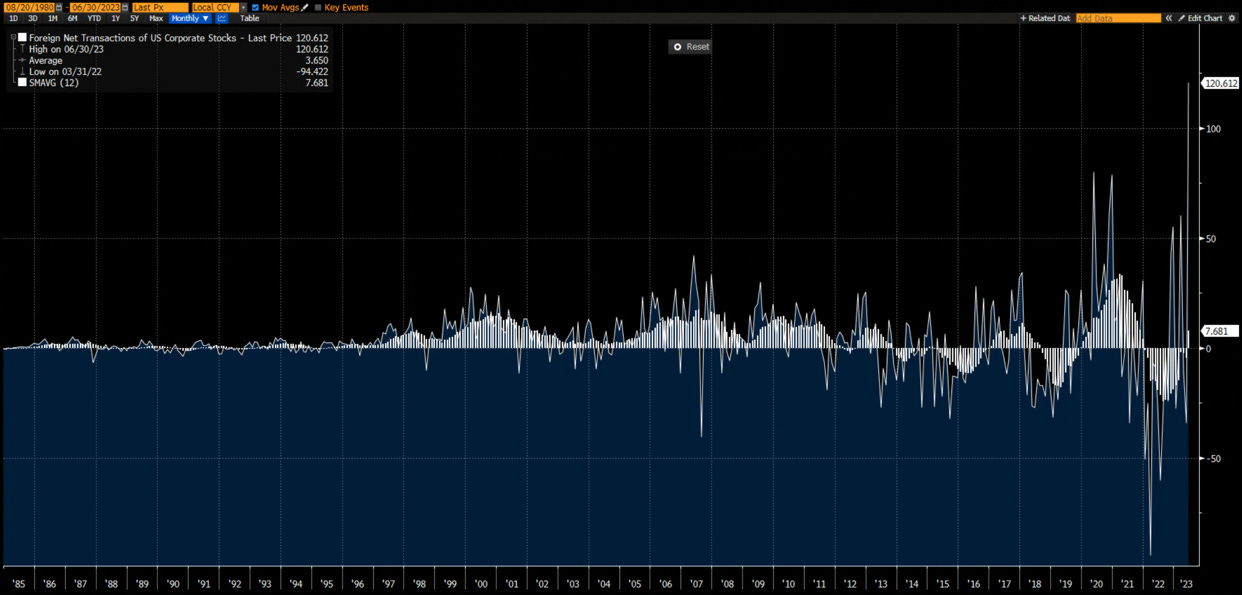

Foreigners have been heavy, very heavy buyers of US stocks recently. This has historically been a good contrarian signal.

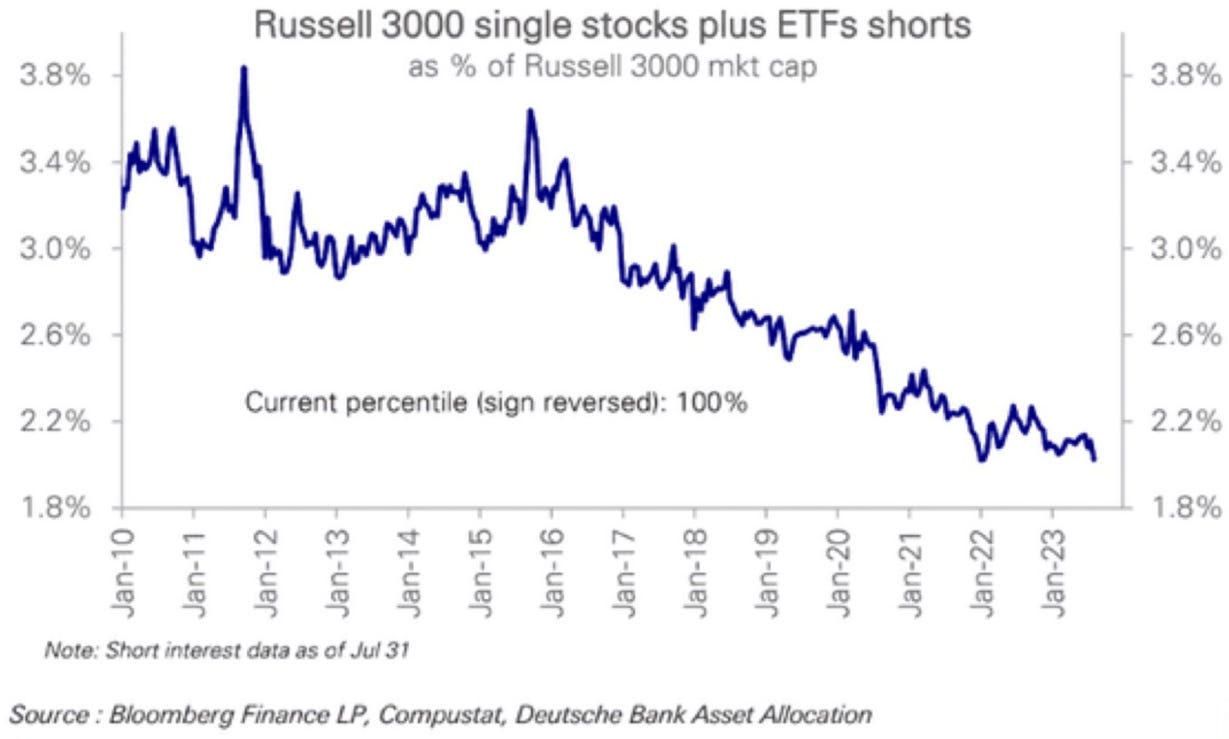

Single stocks and ETF’s short positioning is historically low.

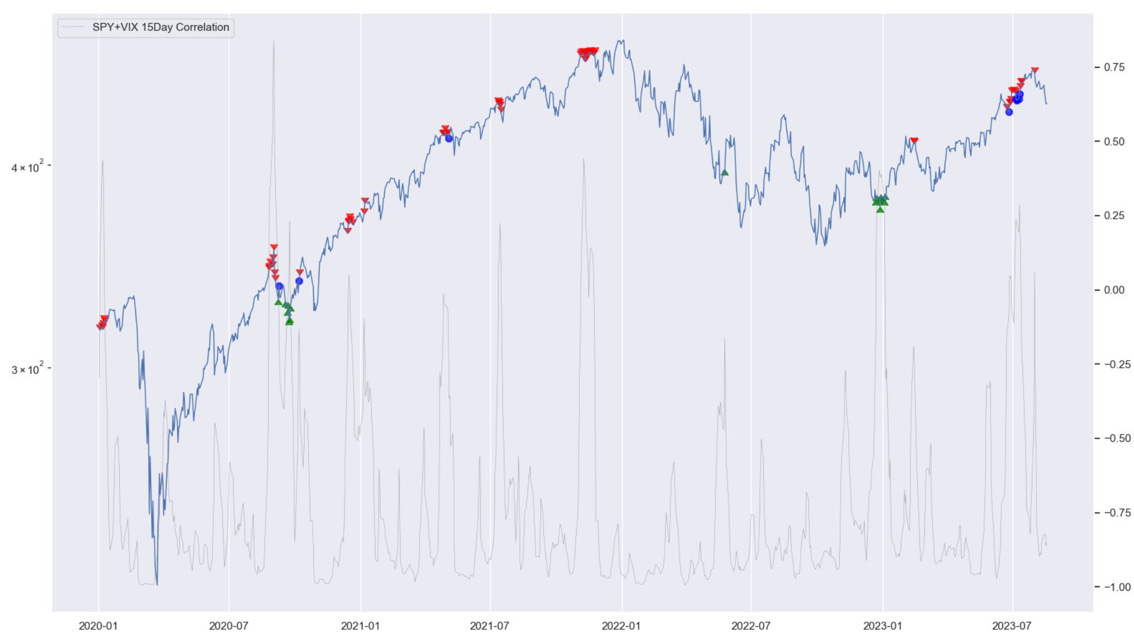

Positive short-term correlation between the S&P 500 and VIX can sometimes pinpoint reversals.

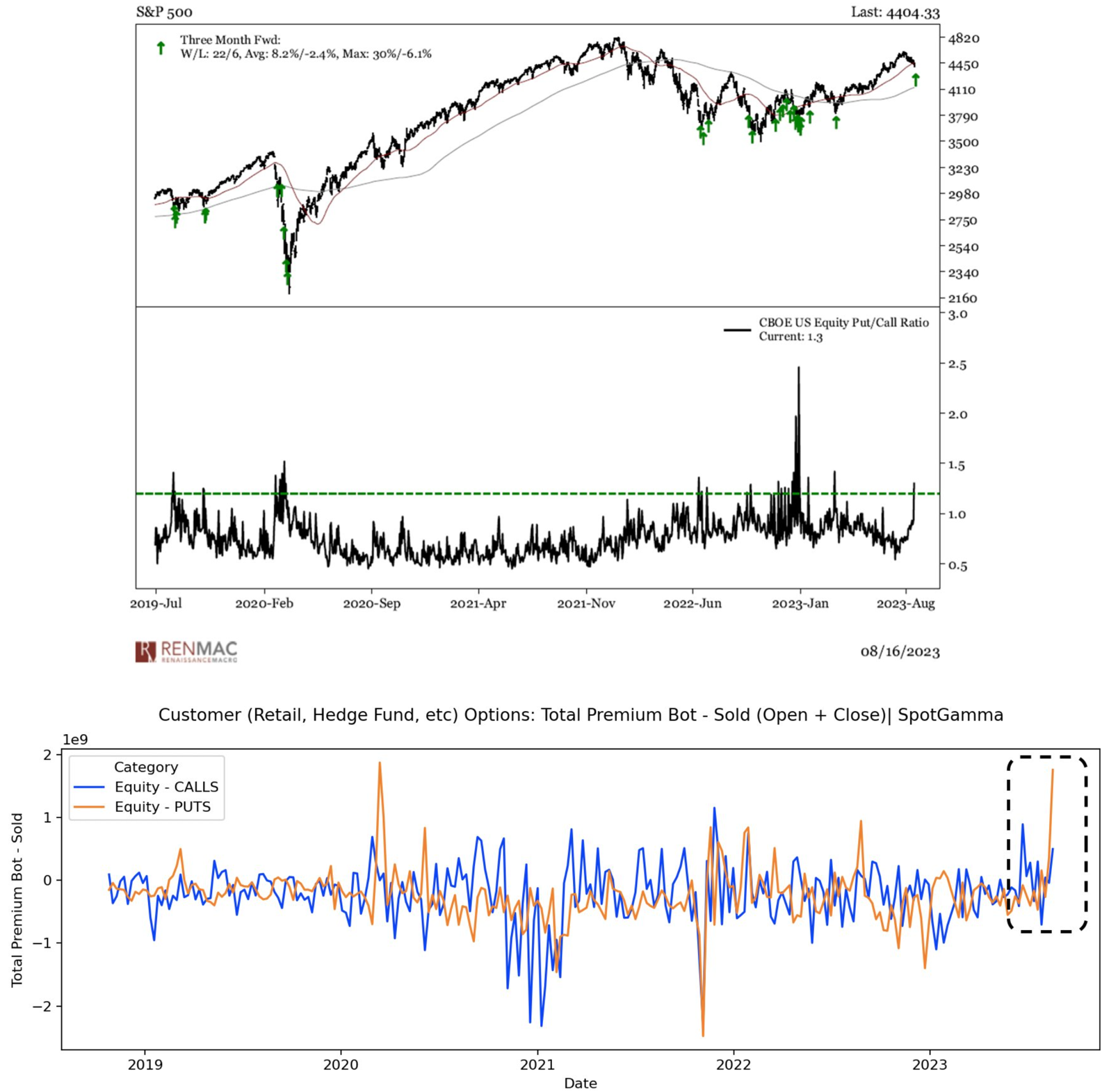

Option markets are showing early sign of stress…

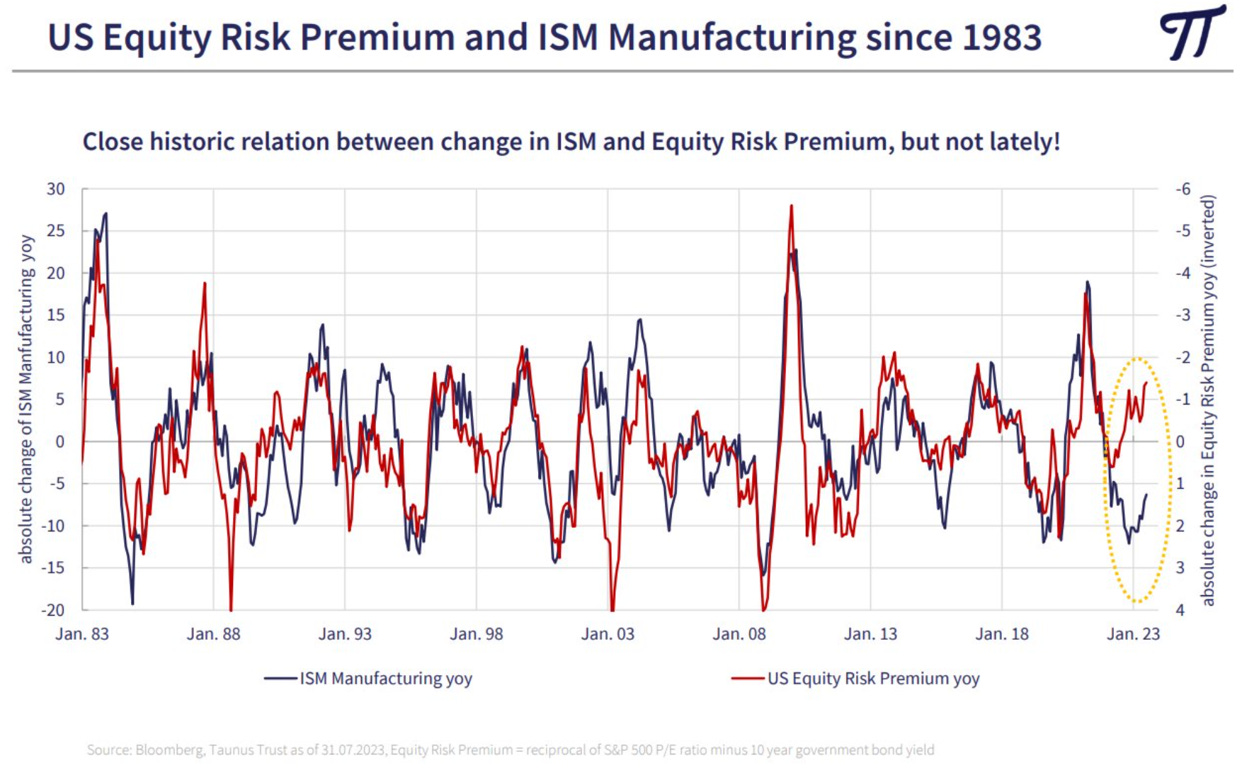

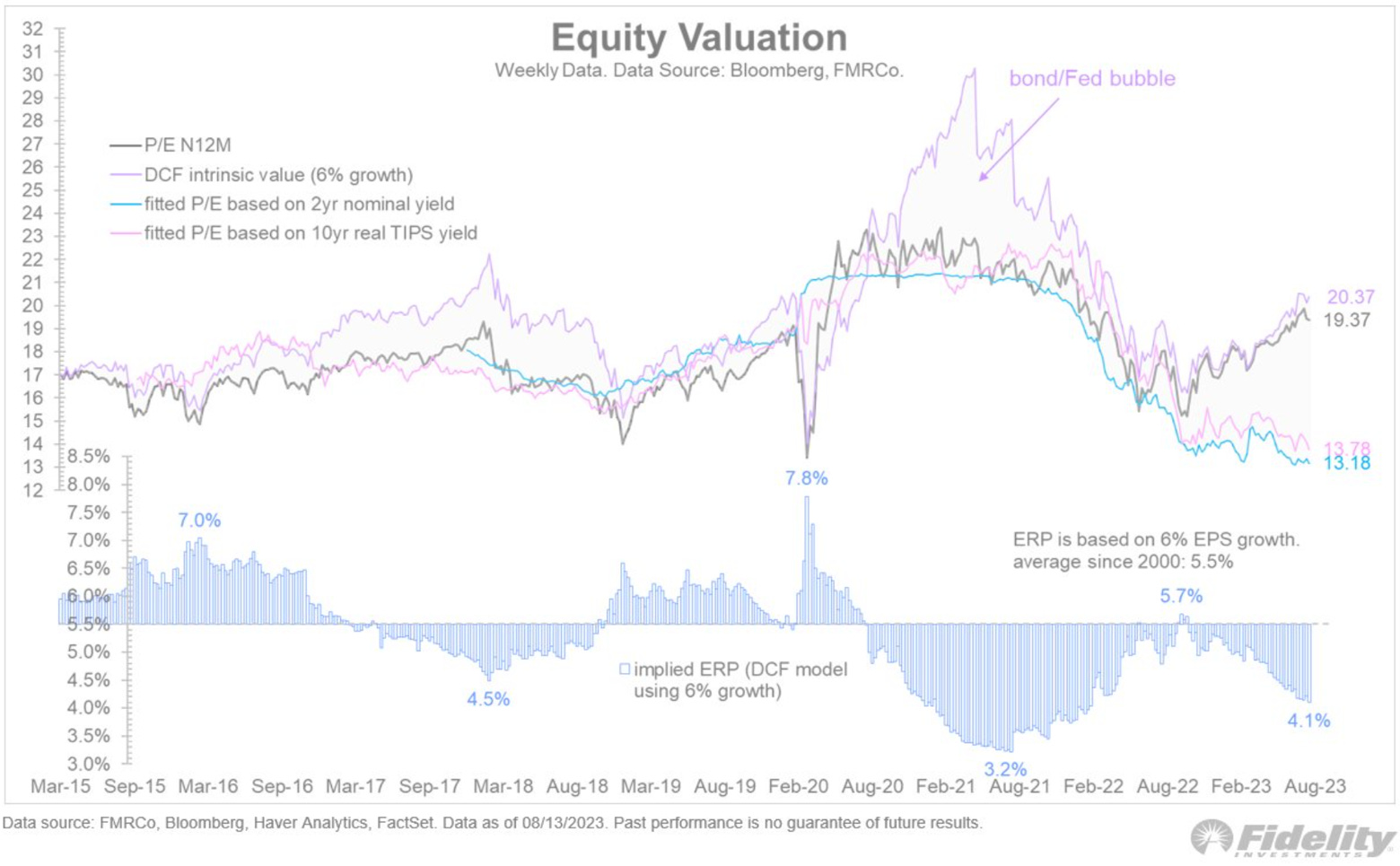

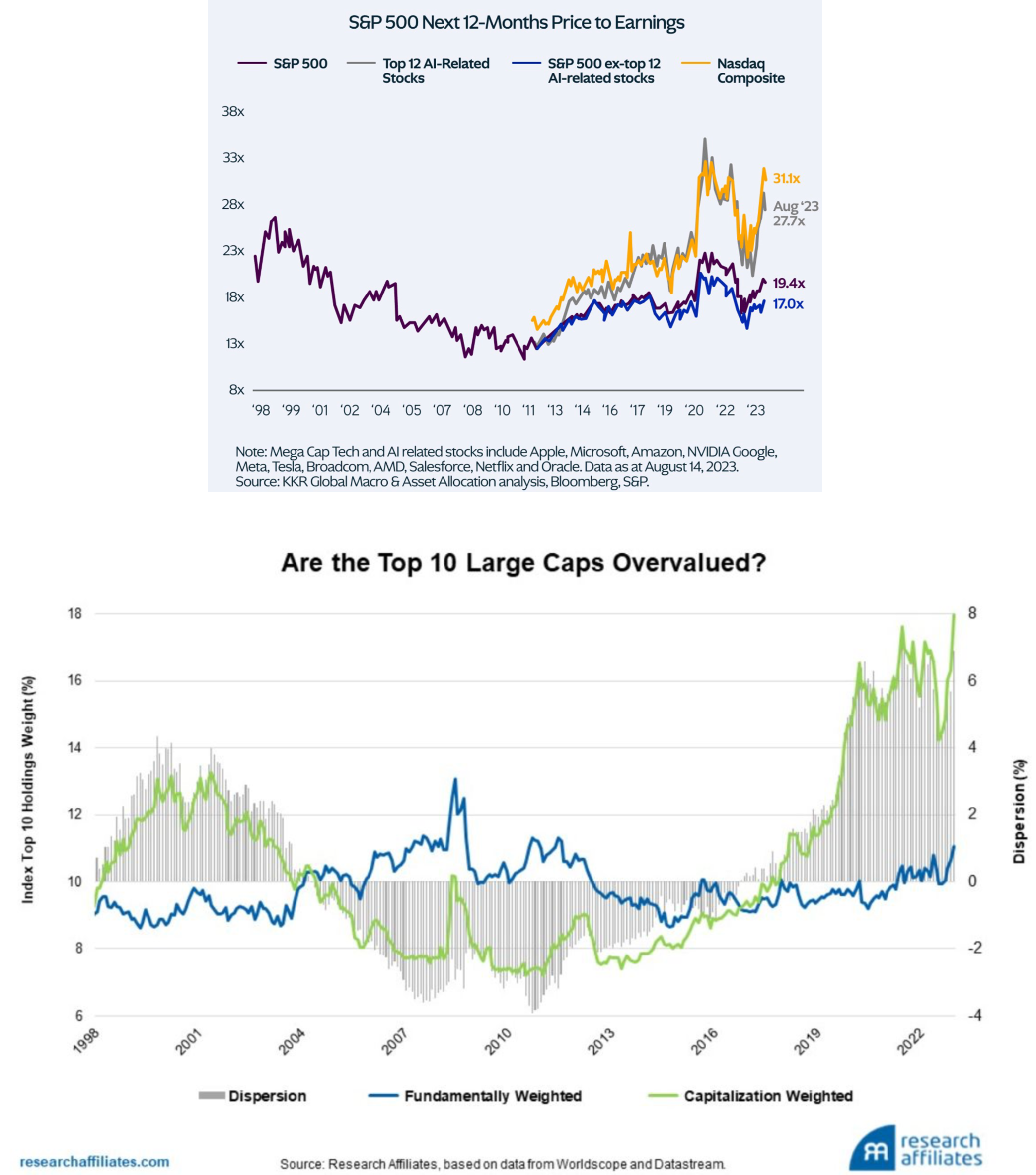

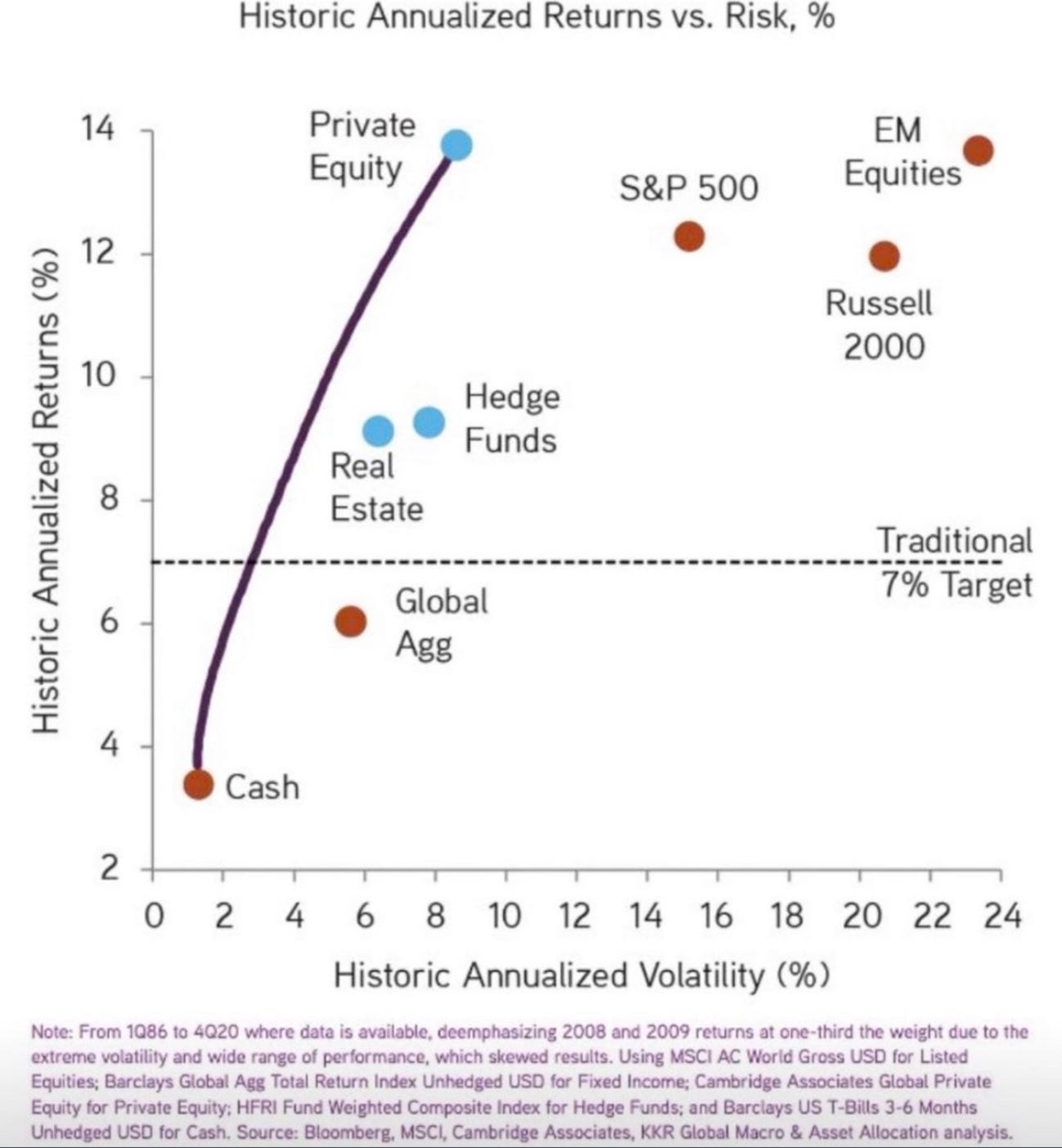

Market - Valuation

US equity risk premium are diverging from the ISM manufacturing.

And the S&P 500 forward PE ratio is 30 to 40% above what short-term Treasuries would imply.

Some parts of the markets are more overvalued than others…

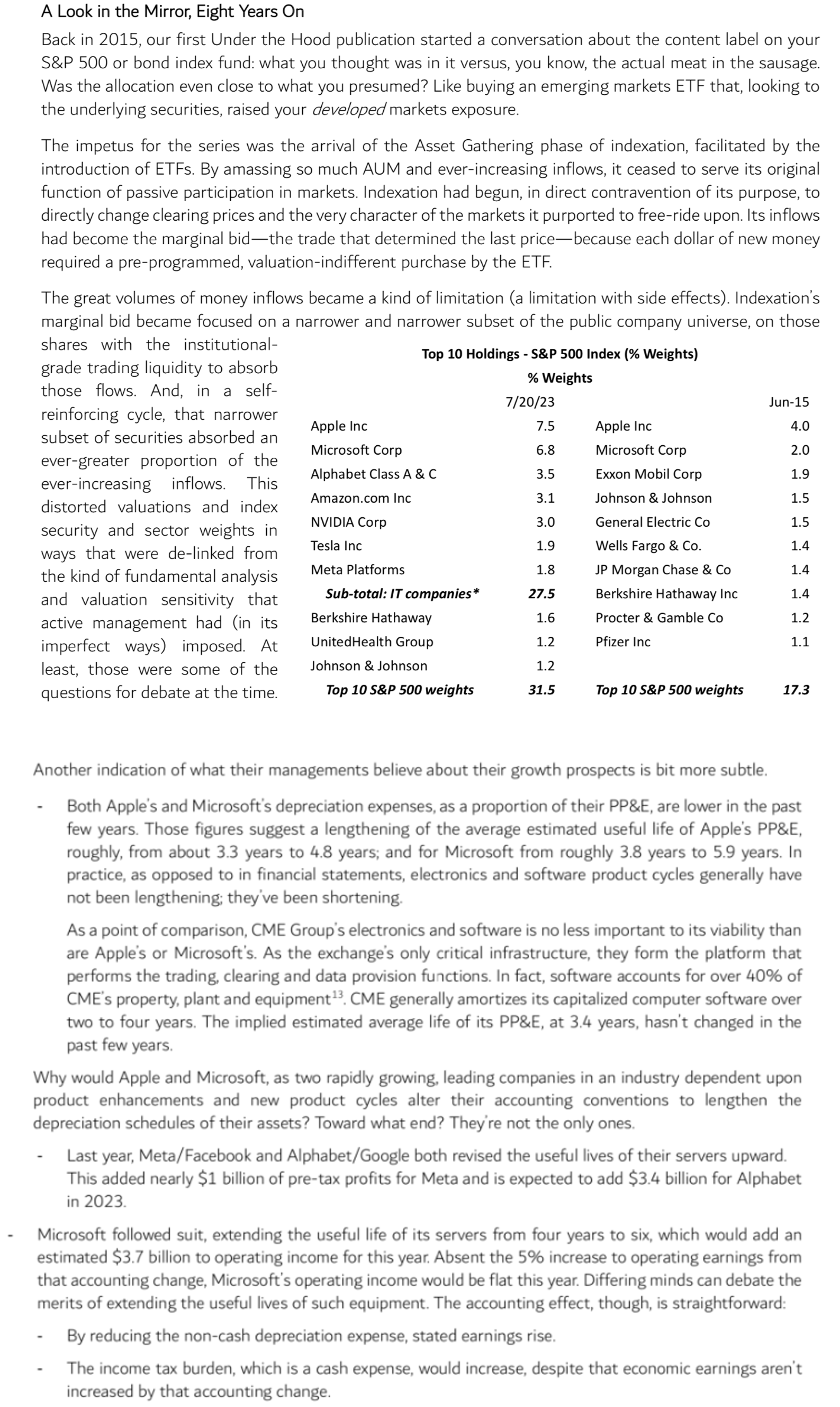

From Horizon Kinetics…

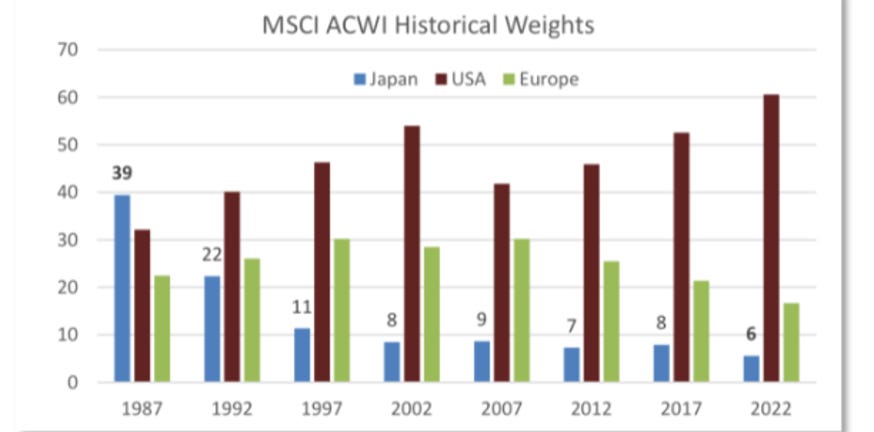

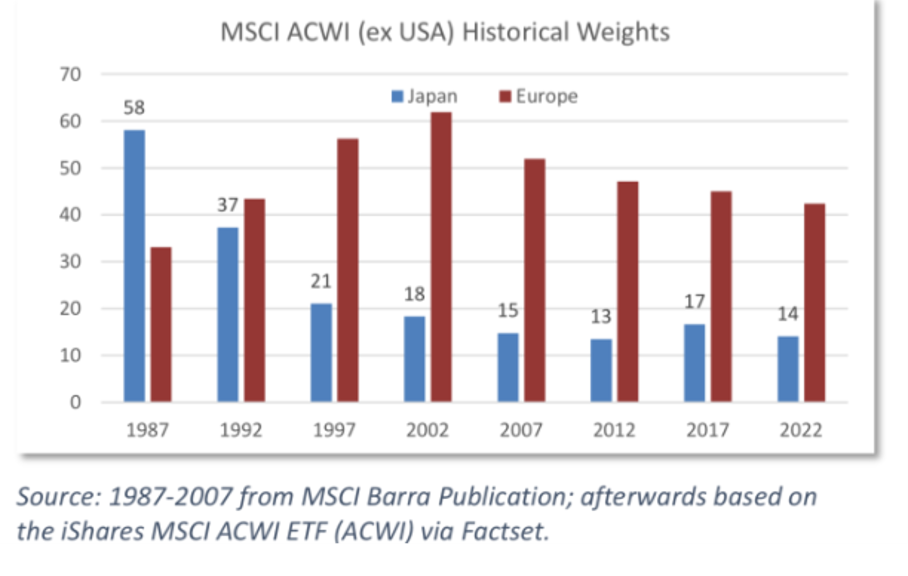

Should the US markets really be 60% of the total world capitalization? Japan almost reached it in 1989…

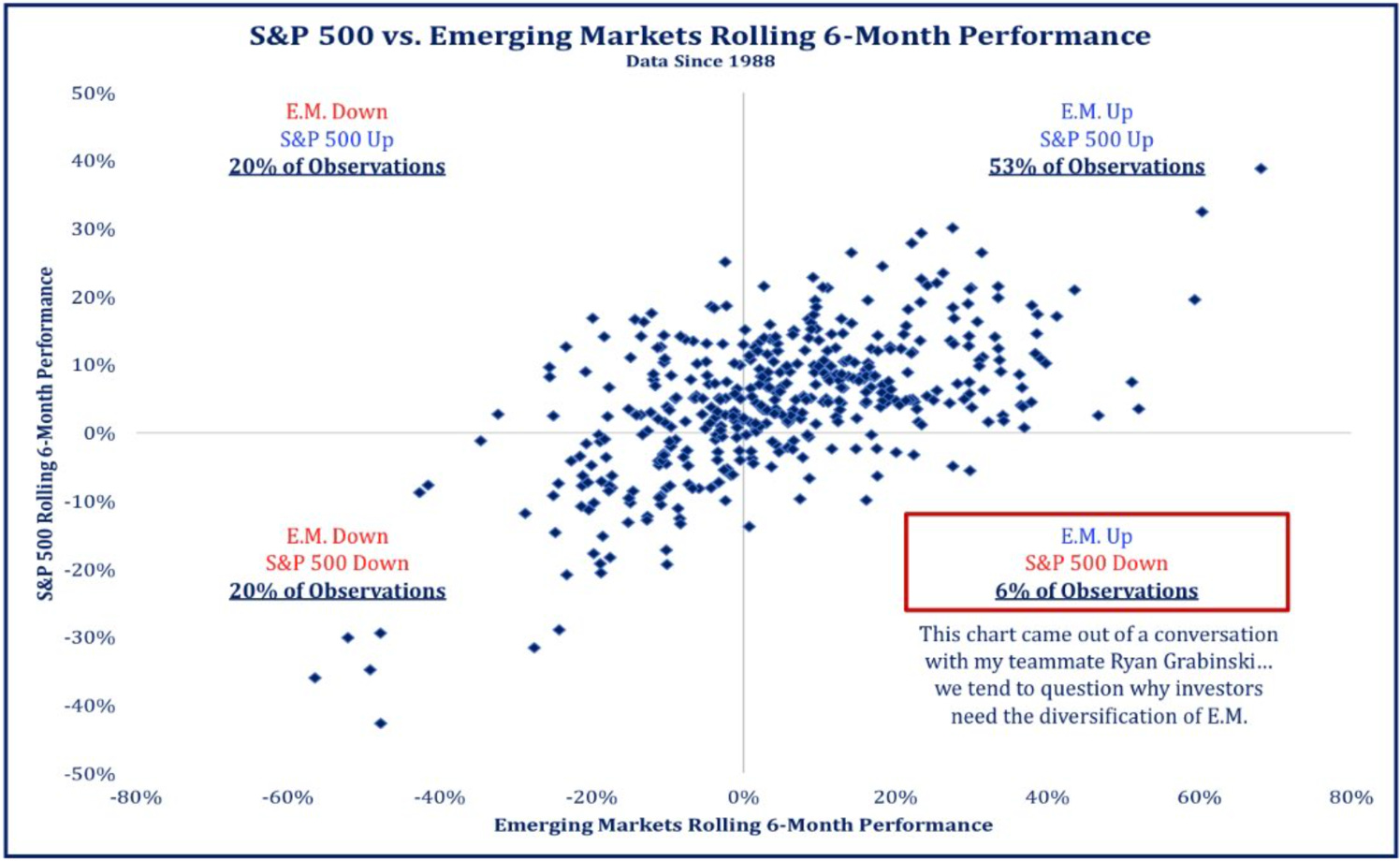

The fact that EM are forecasted to outperform the US by a significant margin in the next 10 years, does not imply that they will be always up when the S&P 500 is down. As you can see EM were only up 6% of the time when the S&P 500 was down since 1988.

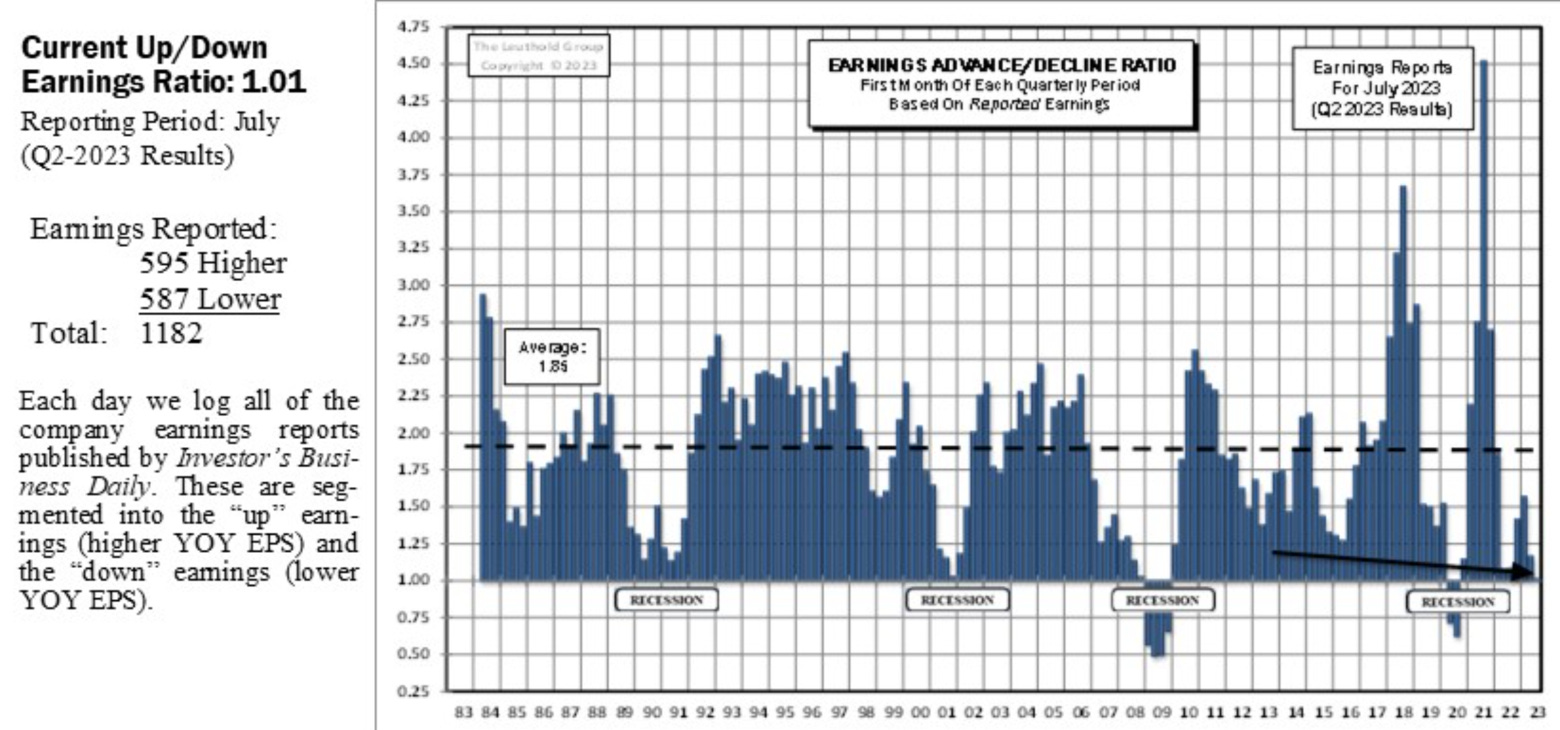

Earnings have not been good this quarter…

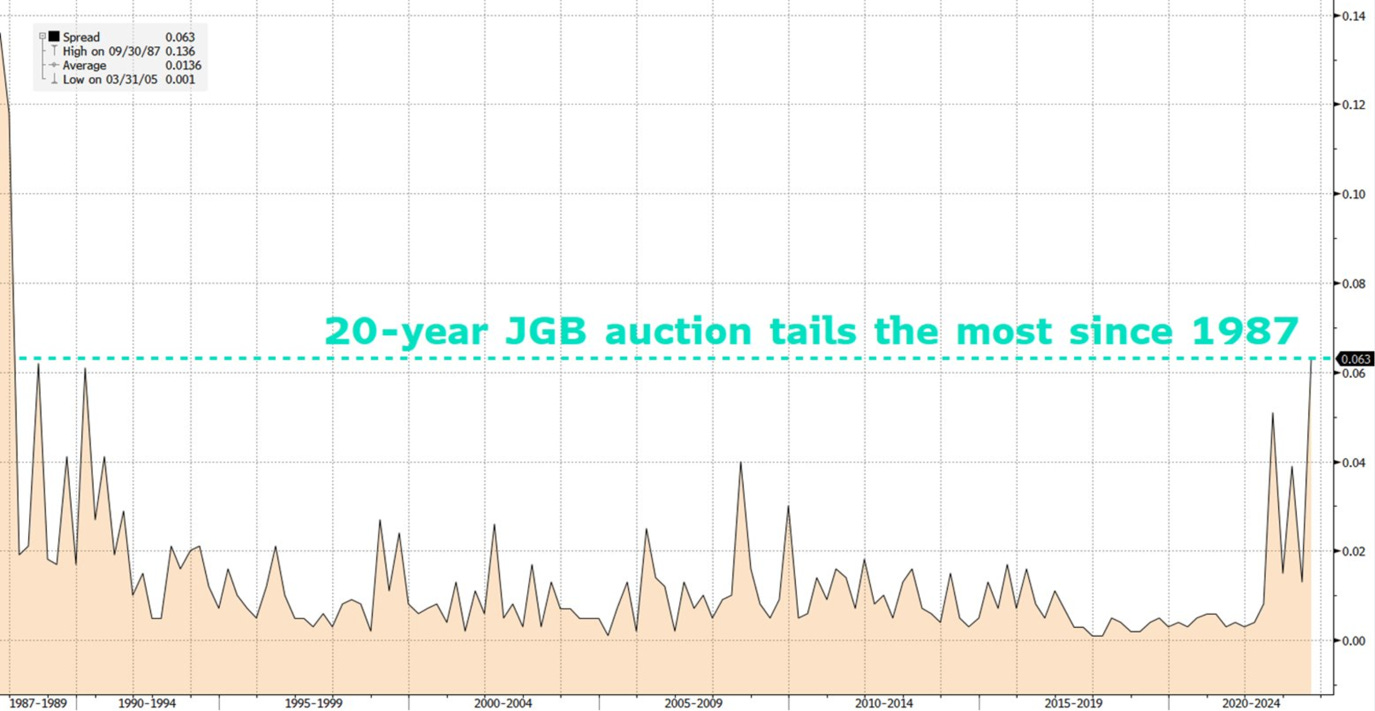

Market – Fixed Income

The JGB markets was characterized as the global anchor for longer-term government bond yields explaining partially (we insist on partially) the rapid recent global up move. JGB auctions tails are increasing quickly…

Others

I also have a bridge to nowhere to sell if you want!

52 years ago

40 years ago

What is a moat?

Thanks for reading Damien’s Substack! Subscribe for free to receive new posts and support my work.